Form 5472 for Foreign-Owned US LLCs: The $25,000 Mistakes Most CPAs Miss

If you own a US LLC as a foreign person, Form 5472 is not optional and getting it wrong costs $25,000 per violation. This guide covers every filing requirement, the disregarded entity trap, related party transactions, and how to fix past errors before the IRS finds them first.

THE NON-US FOUNDER'S COMPLETE GUIDE TO RUNNING A US BUSINESS

3/19/202617 min read

If you own a US LLC as a foreign person, Form 5472 is not optional. It is one of the few IRS information returns that carries an automatic $25,000 penalty for each violation, regardless of whether any tax is owed and regardless of whether you knew the obligation existed. The IRS does not offer grace periods for first-time filers who simply did not know. It assesses the penalty, and the burden falls on you to argue your way out of it.

This guide covers everything a foreign owner of a US LLC needs to understand: who must file, what must be reported, how to file it correctly, what happens when it goes wrong, and how to recover from past errors. It goes significantly deeper than the standard advice available online, because the standard advice frequently misses the structural issues that create the most serious exposure.

Part One: Understanding the Two Very Different Filing Scenarios

The single most important thing to understand about Form 5472 is that it is not one form with one set of rules. It operates in two fundamentally different contexts, and the filing requirements, the correct address, the method of filing, and the parts of the form you complete are different depending on which scenario applies to you. Conflating the two is one of the most common errors made by preparers who understand the form mechanically without understanding the underlying legal structure.

Scenario One: The Foreign-Owned Single-Member LLC (The Disregarded Entity)

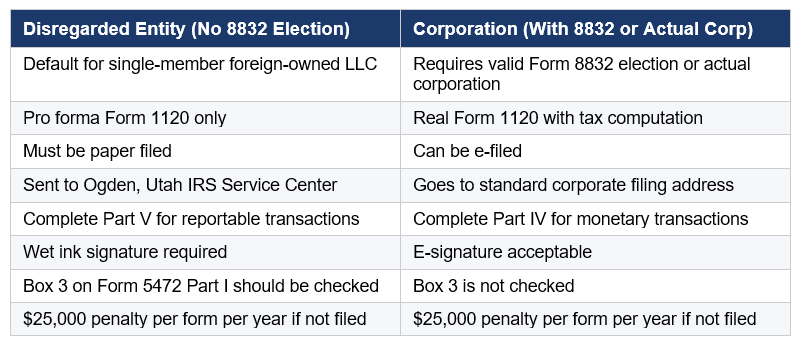

The most common scenario for foreign business owners is a US LLC with a single foreign owner and no Form 8832 entity classification election on file. Under the US check-the-box regulations, this LLC is by default a disregarded entity for US tax purposes. It is treated as if it does not exist separately from its owner.

However, under Treas. Reg. section 1.6038A-1, a disregarded entity owned by a foreign person is treated as a domestic corporation solely for the purpose of the section 6038A reporting requirements. This means it must file Form 5472, but it files it attached to a pro forma Form 1120, not a real corporate return. The Form 1120 is marked as a pro forma return, it carries no tax liability, and its sole purpose is to serve as a cover sheet for the 5472.

This is the scenario where the most procedural errors occur, because the filing rules are genuinely different from a standard corporate return.

ℹ The Form 8832 Question

If no Form 8832 has ever been filed, the LLC is a disregarded entity by default regardless of what it says in its operating agreement or what any accountant has assumed. The existence of a real Form 1120 filing does not mean a valid election was made. If you are unsure whether a Form 8832 was filed for your LLC, this is the first thing to establish before anything else.

Scenario Two: The 25% Foreign-Owned US Corporation

The second scenario applies to an actual US corporation, or to a US LLC that has made a valid Form 8832 election to be treated as a corporation for US tax purposes. If any foreign person owns directly or indirectly at least 25% of the total voting power or total value of the corporation at any point during the tax year, the corporation must attach Form 5472 to its regular Form 1120.

In this scenario, the 5472 travels with the 1120 to whatever IRS service center handles that corporation's return. E-filing is standard and acceptable. The form uses Part IV for monetary transactions rather than Part V. The filing mechanics are substantially simpler.

Part Two: Who Must File and When

The Disregarded Entity Obligation

A foreign-owned single-member LLC must file Form 5472 (attached to a pro forma 1120) for any tax year in which it has any reportable transaction with a foreign or domestic related party. As we explain in detail below, the definition of a reportable transaction is broad enough that almost every foreign-owned LLC has at least one in every year it exists, including the year of formation.

The filing obligation exists regardless of whether the LLC has any revenue. The phrase 'inactive LLC' has no legal meaning in this context. Formation costs, capital contributions, registered agent fees paid by the foreign owner, and cash withdrawals are all reportable transactions. An LLC that was formed, received $500 of initial capital from its foreign owner, paid a registered agent $150, and otherwise did nothing has reportable transactions and must file.

The Corporation Obligation

A US corporation must file Form 5472 if at any time during the tax year a foreign person owned directly or indirectly at least 25% of the total voting power of all classes of stock entitled to vote, or at least 25% of the total value of all classes of stock. The 25% threshold is measured at any point during the year, not just at year end.

There is no minimum transaction threshold. The obligation to file is triggered by the ownership percentage, and then the form reports whatever transactions occurred. If a qualifying corporation had no reportable transactions with its foreign related party during the year, it still files the form but leaves Part IV blank.

What Counts as a Foreign Person

A foreign person for this purpose includes a non-resident alien individual, a foreign corporation, a foreign partnership, a foreign trust, and a foreign estate. It also includes a foreign branch of a US person in some circumstances. Treaty status does not eliminate the filing obligation.

The EIN Requirement

Form 5472 cannot be filed without an Employer Identification Number for the US entity. This sounds obvious but it creates real problems in practice. A foreign person who forms a US LLC from outside the United States often struggles to obtain an EIN without either having a Social Security Number, having an Individual Taxpayer Identification Number, or going through the manual SS-4 process which can take weeks. The 5472 filing deadline cannot be extended simply because an EIN has not arrived. Apply for the EIN as early as possible, ideally at formation, and before the first tax year end approaches.

Part Three: Reportable Transactions

This section is where most guides fall short, and where most foreign-owned LLCs unknowingly accumulate penalty exposure. The definition of a reportable transaction is much broader than most owners and many preparers assume.

a: Monetary Transactions (Corporations and Elected LLCs)

For a corporation or elected LLC using Part IV, reportable monetary transactions include: sales of stock in trade, sales of tangible property, platform contribution payments, cost sharing transaction payments, rents received and paid, royalties received and paid, sales and purchases of intangible property, consideration for technical or managerial services, commissions received and paid, amounts borrowed and lent, interest received and paid, insurance and reinsurance premiums, loan guarantee fees, and any other amounts received or paid.

The catch-all of 'any other amounts received or paid' means that informal transfers, reimbursements, and intercompany payments that owners consider administrative rather than transactional are still reportable. Moving money between your US company and a related foreign entity for any reason is a reportable transaction.

b: Reportable Transactions for Disregarded Entities

For a disregarded entity, Part V applies instead of Part IV. Part V captures transactions as defined under Regulations section 1.482-1(i)(7), which includes any amounts paid or received in connection with the formation, dissolution, acquisition, and disposition of the entity, including contributions to and distributions from the entity.

The practical scope of Part V is extraordinary for year-one filers. Every single one of the following is a reportable transaction that must appear in Part V: the initial capital contribution from the foreign owner, any expenses paid by the foreign owner on behalf of the LLC before it had a bank account, any registered agent or state filing fees reimbursed to the foreign owner, any operating expenses covered by a related party, and any distributions of cash or assets back to the foreign owner.

⚠ The Year-One Trap

Almost every foreign-owned single-member LLC has reportable transactions in its first year of existence, even with zero revenue. The foreign owner contributed capital. Someone paid formation costs. A registered agent was hired. These are all reportable transactions under Part V. Filing nothing because the LLC 'was inactive' or 'had no income' is wrong and creates the same $25,000 penalty exposure as never filing at all.

Transactions with Commonly Controlled Entities

A mistake that catches many owners off guard is the assumption that Form 5472 only covers transactions with the direct foreign shareholder. It does not. A related party for Form 5472 purposes includes any 25% foreign shareholder, any person related to the reporting corporation, and any person related to a 25% foreign shareholder.

This means that if your US LLC sends money to, receives money from, or enters into any arrangement with another company that is commonly owned by the same foreign parent, those transactions are also reportable. If the foreign parent owns both your US LLC and a UK company, and your US LLC regularly transfers funds to that UK company as part of normal operations, every one of those transfers needs to appear on Form 5472. A separate Form 5472 may be required for the UK company as a related party distinct from the direct foreign shareholder.

This is a structural issue rather than an oversight issue. Many foreign-owned US LLCs exist specifically as part of a group structure, collecting US customer payments and remitting them to a related entity elsewhere in the group. The entire remittance flow is reportable, and the balance sheet of the US entity will typically show the accumulated intercompany position if reported correctly. When the 5472 shows zero transactions but the balance sheet shows hundreds of thousands of dollars of intercompany balances, that gap is precisely what IRS matching will detect.

The Transfer Pricing Dimension

Beneath the Form 5472 reporting obligation sits a more complex question that many small foreign-owned US companies have never considered: if the US entity is performing a function within a group structure, is it being compensated at arm's length for that function?

A US LLC that collects customer payments, maintains a bank account, employs staff, pays rent, and bears operating costs is providing a service to the group. Under US transfer pricing rules, it should be compensated for that service at a price that an unrelated party would charge. If the US entity consistently shows losses while the related foreign entity accumulates the economic benefit of the US customer relationships, there is a transfer pricing risk sitting underneath the 5472 compliance question. These two issues are connected and should be addressed together.

Part Four: Filing Mechanics

The Address Question

For a disregarded entity filing a pro forma 1120 with attached 5472, the designated IRS service center is Ogden, Utah. This is not the same address as a standard Form 1120 corporate filing, and sending a pro forma return to the wrong service center is treated as non-filing. Always verify the current Ogden address directly from the IRS Form 5472 instructions before filing, because addresses have changed before and the instructions are updated annually.

For a corporation filing a real Form 1120 with 5472 attached, the 5472 goes wherever the 1120 goes for that corporation. The address is not a separate consideration.

Wet Ink Signatures

The pro forma 1120 attached to a 5472 for a disregarded entity must normally be signed with a wet ink signature. Print the return, sign it physically, and mail it. The IRS does not accept electronic signatures on this filing. If you submit an electronically signed pro forma return, the IRS can treat it as unsigned and therefore as never filed, triggering the $25,000 penalty. This is not a technicality that gets forgiven on first request.

For a corporation filing a real 1120 with the 5472 as an attachment, e-filing is standard and acceptable. The wet ink requirement applies specifically to the disregarded entity pro forma route.

Certified Mail and Filing Evidence

Because the disregarded entity return must be paper filed, filing evidence becomes critical. Use certified mail with return receipt requested. The postmark date on the certified mail receipt is your evidence of timely filing if the IRS later claims the return was never received. Regular mail with no tracking provides no protection at all.

If you file by fax, which is an option for some 5472 submissions, retain the fax confirmation page. Print it, screenshot it, save it permanently. If the IRS says they never received the fax, the confirmation page is your only proof. Without it you have nothing to counter a penalty notice.

For international filers using courier services such as FedEx or DHL, retain the delivery confirmation showing the Ogden address and the delivery date. The same principle applies: your proof of timely filing is only as good as your documentation.

Country Codes and the Reference ID Number

Two administrative details on Form 5472 cause recurring problems.

Country codes must be the correct IRS-recognized two-letter codes. These follow ISO 3166-1 alpha-2 standards in most cases but there are exceptions for certain territories. South Africa is ZA, not SF. Guernsey is GG. Using the wrong country code for the foreign shareholder is a factual error on a disclosure return and should be corrected. If you are uncertain about the correct code for a given jurisdiction, verify it directly against the IRS country code list in the instructions.

The Reference ID number is a unique identifier that ties the foreign related party across all your annual filings. You choose it, but once chosen it must remain consistent. If you change it from year to year, even by accident or by using a different format, it creates a mismatch in IRS records that can flag your return for review. Choose a logical identifier at the start, document it, and use the same one every year.

Part Five: Deadlines

The Standard Annual Deadline

For a disregarded entity using the calendar year, the pro forma 1120 with attached 5472 is due by April 15 of the following year, with a six-month extension available on Form 7004 that pushes the deadline to October 15. The extension must be filed by the original April 15 deadline. An extension of time to file is not an extension of time to pay, but because the pro forma return has no tax liability, the payment dimension is irrelevant here.

For a fiscal year entity, the due date is the 15th day of the fourth month following the close of the fiscal year.

For a corporation filing a real Form 1120, the same due dates apply and the 5472 follows the 1120 deadline.

The Initial Year Complication

When an LLC is formed partway through a calendar year, its first tax year is a short year running from the date of formation to December 31. The first Form 5472 due date is April 15 of the following calendar year, covering that short first year. The short year does not eliminate the filing obligation, and formation-year transactions are subject to Part V reporting as described above.

The Dissolution Deadline

This is the deadline that catches the most people completely off guard. When a foreign-owned LLC is dissolved or otherwise terminates, a final Form 5472 attached to a final pro forma 1120 is required. The deadline for this final filing is the 15th day of the fourth month after the date of dissolution. If the LLC dissolves in July, the final return is due by November 15. This deadline is entirely separate from the standard April 15 annual cycle and operates independently of any tax year.

Many owners dissolve their LLC, assume their tax obligations are complete, and discover months or years later that a final 5472 was required. The same $25,000 penalty applies to the missing final return.

Part Six: The $25,000 Penalty

The penalty under IRC section 6038A(d) is $25,000 for each Form 5472 that is not filed, is filed late, or is filed with incorrect or incomplete information. There is no minimum transaction amount. There is no de minimis exception. A $100 capital contribution that was not reported carries the same potential penalty as a $5 million intercompany transaction.

Per Form, Per Year

The penalty is assessed per form per year. If a reporting corporation was required to file two Forms 5472 in a given year because it had reportable transactions with two separate related parties, and it filed neither, the penalty exposure is $50,000. If it failed to file for three years, the exposure is $150,000. The penalties stack across both forms and years.

The Continuing Failure Penalty

If the IRS notifies the taxpayer of a failure and the failure continues for 90 days after notification, an additional penalty of $25,000 applies for each 30-day period or fraction thereof during which the failure continues. A failure that was not corrected after IRS notification can multiply quickly.

What Triggers a Penalty Notice

The IRS has multiple routes to identifying Form 5472 failures. The most direct is the failure to file a return that was expected based on prior year filings or other information the IRS holds. The more subtle route is information matching: if the IRS has data from FBAR filings, bank Suspicious Activity Reports, FinCEN records, or foreign tax authority information exchange under FATCA, it can identify intercompany flows that should have been reported on Form 5472 but were not. A balance sheet that shows large intercompany balances while the 5472 reports zero transactions is a particularly clear indicator.

Part Seven: When You Are Already in Trouble

Amended Returns and Late Filing

If Form 5472 was filed incorrectly, the fix is an amended pro forma 1120 with a corrected 5472 attached, clearly marked as amended. If Form 5472 was never filed at all, the approach is to file the missing return as soon as possible, ideally before receiving any IRS notice.

Filing late or filing an amended return does not automatically trigger a penalty. The IRS will often accept a delinquent filing, particularly if accompanied by a reasonable cause statement, before a formal penalty is assessed. The moment you receive a penalty notice is not the moment to start the process. The process should start as soon as you know there is a problem.

When filing an amended return to correct structural errors, such as having filed the wrong form type entirely, the amended filing should address the root cause, not just the surface symptom. If a disregarded entity filed a real Form 1120 when it should have filed a pro forma, the amended return needs to reflect the correct form type, the correct filing address, and the correct parts of the 5472.

First-Time Penalty Abatement

The IRS offers first-time penalty abatement administrative relief to taxpayers who have a clean compliance history for the three preceding years. If the taxpayer has no history of penalties in the prior three years and is requesting abatement for the first time, the IRS will generally grant it without requiring a detailed reasonable cause argument. First-time abatement is procedurally straightforward and should be the first approach considered when a 5472 penalty is assessed against a taxpayer with a clean prior history.

Note that first-time abatement is a one-time relief. Using it for a 5472 penalty means it is no longer available for future periods.

Reasonable Cause Arguments

For taxpayers who are not eligible for first-time abatement, or where the penalty amount is large enough to warrant a more detailed argument, a reasonable cause and good faith statement can be submitted with a penalty abatement request. Reasonable cause exists when the taxpayer exercised ordinary business care and prudence but was nevertheless unable to comply.

The strength of a reasonable cause argument depends heavily on the specific facts. Reliance on a qualified tax professional is a recognized basis for reasonable cause, but it requires demonstrating that the reliance was genuine, that the professional was qualified, and that the taxpayer provided complete and accurate information to the professional. A structural error by a preparer who was given all the relevant facts is a more difficult case than a taxpayer who was unaware of the filing obligation entirely.

When the underlying error is a wrong form type or wrong filing address resulting from a preparer's misunderstanding of the entity's classification, the reasonable cause narrative needs to address both the taxpayer's good faith and the preparer's qualifications. This is where working with a tax attorney, rather than the original preparer, on the abatement request makes a material difference.

Preparer Liability

A paid preparer who signs a return containing an unreasonable position, or who demonstrates reckless disregard for IRS rules, is subject to penalties under IRC section 6694. Filing a real Form 1120 for an entity with no Form 8832 election on file, e-filing a return that required paper filing, or reporting zero related party transactions when the balance sheet shows hundreds of thousands of dollars of intercompany balances are not judgment calls. They are errors that fall within the scope of preparer liability.

Preparer penalties are separate from taxpayer penalties. The IRS assesses the $25,000 against the entity first. If the entity wants to recover those costs from the preparer, that requires a civil claim for professional negligence or a claim against the preparer's errors and omissions insurance. This is a separate process from the IRS penalty, and it is the entity's burden to pursue.

Part Eight: What Form 5472 Does Not Cover

Knowing where Form 5472 ends is as useful as knowing where it begins.

Form 5472 does not apply to multi-member LLCs without a Form 8832 election. A multi-member LLC is by default treated as a partnership for US tax purposes. The reporting and filing requirements for a foreign-owned partnership are different, involving Form 1065, Schedule K-1, and potentially Forms 8804 and 8805 for withholding on effectively connected income.

Form 5472 does not replace other international reporting obligations. A foreign-owned US corporation with foreign subsidiaries may also have Form 5471 obligations. A US person with signature authority over foreign financial accounts has FBAR obligations. FATCA reporting under Form 8938 applies separately. Form 5472 is one piece of a potentially larger international compliance picture.

Form 5472 does not report the foreign owner's personal tax obligations. The foreign owner's own US filing requirements, such as Form 1040-NR for effectively connected income, are separate from the entity-level Form 5472 obligation.

Part Nine: A Practical Checklist

Before filing Form 5472, work through the following:

• Confirm whether the LLC has a valid Form 8832 election on file. If not, it is a disregarded entity and the pro forma 1120 route applies.

• Confirm the LLC has an EIN. Do not attempt to file without one.

• Identify all related parties, not just the direct foreign shareholder. Include any entity under common ownership that had any transaction with the US LLC during the year.

• Determine whether one or more Forms 5472 are required based on the number of related parties with reportable transactions.

• For disregarded entities, complete Part V, not Part IV. Document all formation-year transactions including capital contributions and expenses paid by the owner on behalf of the entity.

• Verify the country codes for all foreign related parties against the IRS country code list. Do not assume.

• Assign or confirm the Reference ID number for each foreign related party and ensure it matches prior years.

• For disregarded entities: print the return, sign in wet ink, send by certified mail to Ogden, Utah. Retain the certified mail receipt permanently.

• Note the deadline. For calendar year entities, April 15 with a six-month extension available.

• If the LLC dissolved during the year, note the separate final return deadline: 15th day of the fourth month after dissolution.

• Retain all filing evidence, including certified mail receipts, fax confirmations, and delivery confirmations, indefinitely.

How Antravia Advisory Can Help

Form 5472 compliance sits at the intersection of entity classification, international tax, and transfer pricing. Getting it right requires understanding not just the form itself but the underlying structure of the business and the relationships between related parties across jurisdictions.

Antravia Advisory works with foreign-owned US businesses across a range of international tax compliance needs, including Form 5472 preparation for both disregarded entities and corporations, related party transaction documentation, transfer pricing considerations for small and mid-size international groups, penalty abatement requests, and amended return filings for prior-year errors.

If you are unsure whether your LLC has been filing correctly, or if you have received an IRS penalty notice, contact us for an initial consultation. The sooner a compliance gap is identified, the more options are available to resolve it.

Disclaimer

This article is published by Antravia Advisory for general informational purposes only. It does not constitute tax advice and does not create a client relationship. US tax law is complex and fact-specific. The information in this article reflects the law as understood at the time of publication and may not reflect subsequent changes. Every taxpayer's situation is different. You should consult a qualified US tax professional before making any decisions based on the content of this article.

The Non-US Founder’s Complete Guide to Running a US Business

The Non-US Founder's Complete Guide to Running a US Business - Everything a non-US founder needs to know about setting up, operating, and scaling a US business, from choosing the right entity and opening a bank account, to tax compliance, paying yourself, hiring staff, and managing your home country obligations. Built for international entrepreneurs who want to get it right. Link

Disclaimer:

Content published by Antravia is provided for informational purposes only and reflects research, industry analysis, and our professional perspective. It does not constitute legal, tax, or accounting advice. Regulations vary by jurisdiction, and individual circumstances differ. Readers should seek advice from a qualified professional before making decisions that could affect their business.

See also our Disclaimer page

Antravia Advisory

Accounting built for complexity

Not legal advice, always verify with your Accountant

Email:

Contact us:

© 2025. All rights reserved. | Disclaimer | Privacy Policy | Terms of Use |

contact@antravia.com

Antravia LLC

941 W Morse Blvd suite 100

Winter Park

Florida

32789