Part 2: Choosing Your US Entity

The Non-US Founder's Complete Guide to Running a US Business - Part 2 explains how to choose the right U.S. entity as a non-U.S. founder. Compare LLC vs C-Corp, understand ECI and ETBUS, review state selection, compliance costs, BOI reporting, and the tax impact of each structure before you form.

THE NON-US FOUNDER'S COMPLETE GUIDE TO RUNNING A US BUSINESS

2/25/202630 min read

The entity you choose is the foundation on which everything else is built. It determines how you are taxed, how you can pay yourself, whether you can raise investment, what forms you must file, and, critically, how your home country treats what you have created. Getting this decision right from the start is significantly cheaper and less disruptive than fixing it later.

This part covers every meaningful structure available to a non-US founder, the tax concepts that make certain choices better or worse depending on your circumstances, and a practical comparison to help you reach the right decision for your situation. The entity decision has technical consequences, and understanding them is the only way to make an informed choice.

1. Available Structures — The Full Landscape

Non-US founders have more options than most guides acknowledge. In practice, most end up choosing between an LLC and a C-Corp - but understanding the full range of available structures, and why the others are usually unsuitable, is part of making an informed decision.

Limited Liability Company (LLC)

The LLC is the most flexible and most commonly chosen structure for non-US founders without VC ambitions. It is a state-level entity, so created under state law, not federal law, that provides limited liability protection to its members (owners) while offering significant flexibility in how it is taxed and managed. The default tax treatment of an LLC depends on how many members it has: a single-member LLC is treated as a "disregarded entity" for US federal tax purposes, while a multi-member LLC is treated as a partnership.

The LLC is not a corporation. It does not have shareholders, a board of directors, or share capital in the traditional sense. It has members and, typically, an operating agreement that governs how the business is run and how profits are distributed. This flexibility makes it highly adaptable, but it also means that the legal and tax treatment of an LLC is more nuanced than many formation guides suggest.

C-Corporation (C-Corp)

The C-Corp is a separate legal entity that is taxed independently from its owners. It pays US corporate income tax at a flat rate of 21% on its profits. Distributions to shareholders (dividends) are then taxed again in the shareholder's hands, hence the term "double taxation." Despite this, the C-Corp is the standard structure for venture-backed startups and companies that plan to issue equity to employees, raise institutional capital, or eventually pursue a public offering.

Delaware is overwhelmingly the most popular state for C-Corp formation, primarily because Delaware's corporate law is the most mature and well-understood in the US, Delaware's Court of Chancery provides a specialist business court with extensive case law, and investors, lawyers, and fund counsel are all thoroughly familiar with Delaware C-Corp documentation and governance structures.

S-Corporation (S-Corp)

The S-Corp is a special tax election that allows a corporation to be treated as a pass-through entity for US federal tax purposes, meaning profits are taxed at the shareholder level rather than the corporate level. It sounds appealing, but non-US founders are almost entirely excluded from using it.

Non-residents cannot normally hold S-Corp shares. S-Corp status requires that all shareholders be US citizens or permanent residents (like green card holders). A single non-resident alien shareholder disqualifies the entity from S-Corp status entirely. This rules out the S-Corp for virtually every non-US founder. It is mentioned here only so you understand why it does not appear in the rest of this guide.

US Branch of a Foreign Corporation

Rather than forming a new US entity, a foreign company can operate in the US directly through a branch, a US operating presence of the foreign parent. The branch is not a separate legal entity; it is the foreign corporation doing business in the US. This means the foreign company has direct legal exposure in the US, it can be sued in US courts, it holds US contracts and assets, and it has US tax obligations.

Branches are also subject to the Branch Profits Tax, a 30% tax (reducible by treaty) on earnings deemed to have been repatriated to the foreign parent. For these reasons, branches are rarely the right structure for early-stage founders. They are most commonly used by large foreign corporations establishing a US commercial presence where full subsidiary formation is unnecessary.

Representative Office

A representative office is a very limited US presence, it can conduct market research, promote the foreign company's products or services, and liaise with customers, but it cannot conduct revenue-generating activity or sign contracts on the company's behalf. It is not a separate legal entity and provides no liability protection. For most founders, this structure is too limited to be useful. It exists primarily as a light-touch option for foreign companies exploring the US market before committing to full formation.

IRS — Entity Classification (Check-the-Box Rules)

https://www.irs.gov/businesses/small-businesses-self-employed/business-structures

Form 8832 (Entity Classification Election)

https://www.irs.gov/forms-pubs/about-form-8832

Form 2553 (S-Corp Election)

https://www.irs.gov/forms-pubs/about-form-2553

S Corporation Eligibility Requirements (IRS)

https://www.irs.gov/businesses/small-businesses-self-employed/s-corporations

2. The Most Important Question: Will your Business Generate ECI?

Before you choose between an LLC and a C-Corp, you need to answer a more fundamental question: will your US business generate Effectively Connected Income?

The answer to this question shapes everything that follows, your tax obligations, your filing requirements, the efficiency of different entity types, and how much of your US profit ultimately reaches you after tax. It is not a question most formation guides ask, because most formation guides do not think about tax, they just help you file paperwork. This guide is different.

What is Effectively Connected Income (ECI)?

ECI is income that is effectively connected to the conduct of a trade or business within the United States. It is the category of US-source income that is taxed at regular graduated or corporate rates, net of deductions, in the same way that a US resident or corporation would be taxed.

To have ECI, you generally need to be "Engaged in a Trade or Business in the United States", the ETBUS standard. ETBUS is a facts-and-circumstances test. There is no single bright-line rule, but the IRS looks for regular, continuous, and substantial business activity in the US. Activities that typically satisfy ETBUS include:

– Maintaining a US office or fixed place of business that is regularly used

– Having US-based employees who perform services for the business

– Having a US agent with authority to conclude contracts on behalf of the business

– Performing services in the US on a regular and continuous basis

– Holding and managing inventory in the US (depending on facts and treaty position)

The key word throughout is "regular and continuous." Occasional or isolated US activity generally does not create ETBUS. A foreign consultant who attends one US conference per year and has no other US activity is unlikely to be ETBUS. A foreign SaaS company with a US sales team and a US office almost certainly is.

What is FDAP income?

FDAP stands for Fixed, Determinable, Annual, or Periodic income. It is US-source income that is not ECI, typically passive income such as dividends from US companies, interest on US bank accounts or bonds, rental income from US property, and royalties for intellectual property used in the US.

FDAP income is taxed differently from ECI. It is subject to a flat 30% withholding tax on the gross amount, no deductions, no expenses, just 30% off the top. The 30% rate can be reduced or eliminated by a tax treaty between the US and your home country. The payer of FDAP income, a US company paying you a dividend or royalty, for example, is responsible for withholding and remitting the tax to the IRS. You receive the net amount.

ECI vs FDAP in plain terms: ECI is taxed like a business, on net income, at regular rates, with deductions. FDAP is taxed like a passive payment, on gross income, at a flat rate. Which category your income falls into matters enormously for your effective tax rate.

Why ECI vs FDAP changes your entity decision

If your business generates ECI, which it almost certainly will if you have genuine US operations, then you have US tax obligations regardless of your entity structure. The question is how efficiently different entities manage those obligations.

For a single-member LLC generating ECI: the income flows through to you, the foreign owner, and is taxed in your hands at US graduated rates. You file a Form 1040-NR. The LLC itself files a Form 5472 and pro forma Form 1120 but pays no tax at the entity level.

For a C-Corp generating ECI: the income is taxed at the 21% corporate rate at the entity level. If you want to extract that income as a dividend, it is withheld at 30% (less any treaty reduction) before it reaches you. This is the double taxation problem. However, if the C-Corp retains and reinvests its profits, as many growth-stage companies do, the double taxation only materialises when you actually distribute profits.

If your business generates primarily FDAP income, for example, a US holding company that receives royalties from a foreign operating company, then the analysis is different again. The 30% withholding rate on FDAP, potentially reduced by treaty, may be more efficient than having ECI taxed at net rates, depending on your margin structure and treaty position.

IRS — Effectively Connected Income (ECI) Explained

https://www.irs.gov/individuals/international-taxpayers/effectively-connected-income-eci

IRS Publication 519 — U.S. Tax Guide for Aliens

https://www.irs.gov/forms-pubs/about-publication-519

IRC §864(c) — Definition of ECI (Cornell Law, official statute text)

https://www.law.cornell.edu/uscode/text/26/864

3. The ETBUS Test — What triggers it and why it matters

We introduced ETBUS above. This section goes deeper, because the ETBUS determination is one of the most consequential, and most misunderstood, questions in US international tax.

The agent standard

One of the most commonly triggered ETBUS factors is the presence of a dependent agent in the US, someone who regularly acts on your behalf and has authority to conclude contracts for your business. This agent does not need to be a formal employee. A US-based contractor who exclusively or predominantly works for you and has contracting authority may be sufficient to create ETBUS.

By contrast, an independent agent, a broker or distributor who works for multiple clients and acts in their own name, does not generally create ETBUS for a foreign principal. The distinction between dependent and independent agents is important and fact-specific.

The office or fixed place of business standard

If you maintain a US office, even a shared office, coworking space, or virtual office (where employees could sit) with a physical address where your staff or you regularly work, this is strong evidence of ETBUS. A PO box or pure mail forwarding address (like a virtual office which is mosttly used for mail services) is generally not sufficient to create a fixed place of business. But a WeWork desk that a US employee regularly uses almost certainly is.

Services performed in the US

If you or your team regularly perform services in the United States, consulting work, software development, project delivery, and you do so on an ongoing basis, this may create ETBUS. Note that the relevant question is where the services are performed, not where the client is located. A European consultant who performs all their work from Europe for US clients is not performing services in the US, even though their income is US-sourced.

ETBUS and your entity type

Here is where the entity type interacts with ETBUS in an important way. A single-member LLC is treated as a disregarded entity, the IRS looks through it to the foreign owner. So the ETBUS analysis is conducted at the owner level: are you, the non-resident individual, engaged in a trade or business in the US?

A C-Corp, by contrast, is a separate taxpayer. The ETBUS analysis is conducted at the corporate level. A foreign-owned C-Corp that has a US office and US employees is clearly ETBUS. It pays 21% tax on its ECI at the corporate level and faces the additional question of how to efficiently distribute profits to the foreign parent or founder.

Tax treaties and the ETBUS test

Many US tax treaties provide a higher threshold for ETBUS, typically requiring a Permanent Establishment (PE) rather than merely ETBUS, before the other country can tax business profits. If your home country has a treaty with the US, and you do not have a PE in the US (a fixed place of business, dependent agent, etc.), the treaty may protect your US-source business income from US tax even if it would technically be ECI under domestic law.

This is a meaningful protection for many founders, particularly those who sell into the US market from abroad without maintaining a US office or US staff. However, treaty benefits are not automatic so you must claim them on the relevant forms, and the IRS can challenge treaty positions.

IRS — Trade or Business in the United States (Pub 519)

https://www.irs.gov/publications/p519#en_US_2023_publink1000222187

Treasury Regulations §1.864-2

https://www.law.cornell.edu/cfr/text/26/1.864-2

4. LLC Deep Dive

The LLC is the right choice for the majority of non-US founders who are not raising institutional VC capital. Here is what you need to understand in detail.

Single-Member LLC (SMLLC)

A single-member LLC owned by a non-US person is treated as a disregarded entity for US federal income tax purposes. "Disregarded" means the IRS ignores the entity's existence for tax purposes and looks straight through it to the owner. The owner reports the LLC's income and expenses on your own tax return, not on a separate business return.

For a non-resident alien owner, this means normally your LLC's income is reported on Form 1040-NR if it constitutes ECI. The LLC itself files a Form 5472 (Information Return of a 25% Foreign-Owned US Corporation or a Foreign Corporation Engaged in a US Trade or Business) and a pro forma Form 1120 (effectively a shell corporate return). These are information returns, not tax returns, the tax is paid at the individual level. But the penalties for missing the Form 5472 filing are severe, and they apply regardless of whether you owe any tax.

Multi-Member LLC

A multi-member LLC, one owned by two or more members, is treated as a partnership for US federal tax purposes by default. This is a fundamentally different tax treatment from a single-member LLC, and it has significant implications.

A partnership files a Form 1065 (US Return of Partnership Income) every year. Each member receives a Schedule K-1 showing their allocable share of the partnership's income, deductions, and credits. Each member then reports their K-1 income on their own tax return, Form 1040-NR for non-resident alien members.

The withholding rules for partnerships with foreign partners are particularly important. Under Section 1446, the partnership is required to withhold US tax on the foreign partner's allocable share of ECI, currently at the highest applicable rate, and remit it to the IRS, even if no cash is actually distributed to the partner. This means a foreign partner in a profitable US partnership may owe US tax on profits they have not yet received, and the partnership must withhold on their behalf.

Partnership withholding trap: If you are a non-resident member of a profitable US multi-member LLC and no one has set up Section 1446 withholding, the partnership is non-compliant and you may have a personal US tax liability on income you have not been paid. Get this right from the start.

LLC tax elections — the choices available

By default, an LLC is treated as a disregarded entity (if single-member) or a partnership (if multi-member) for US tax purposes. But an LLC can elect to be treated as a corporation by filing Form 8832 (Entity Classification Election). And if it elects corporate treatment, it can then elect S-Corp status — subject to the S-Corp eligibility restrictions that disqualify non-resident owners.

For non-US founders, the most relevant elections are:

– Default disregarded entity (single-member) — the simplest, most common choice for non-VC-backed businesses

– Default partnership (multi-member) — requires Form 1065 and K-1 filings; triggers Section 1446 withholding obligations

– Check-the-box election to be taxed as a C-Corp (Form 8832) — gives you LLC legal structure with corporate tax treatment; rarely optimal

The check-the-box election is sometimes suggested as a way to get corporate tax treatment without the governance formalities of a C-Corp. In practice, for non-US founders, this rarely makes sense — if you want corporate tax treatment, you are usually better served by actually forming a C-Corp.

Permanent Establishment risk for LLC owners

Because a single-member LLC is disregarded, the IRS looks through it to the foreign owner, your home country may also look through it and treat the LLC's activities as your personal business activities. If those activities are conducted substantially from your home country, your home country may argue that you have a Permanent Establishment there, and that the income is taxable domestically.

This is particularly relevant for UK, German, and Australian founders, all of whom operate in jurisdictions with active PE enforcement. It is less relevant if you have genuine US economic substance, real employees, real US operations, decisions being made in the US, because substance is the primary defence against PE attribution.

5. C-Corp Deep Dive

The C-Corp is the correct choice if you are raising US institutional capital, issuing equity to US employees, or building toward a US exit. Here is what you need to understand.

The 21% flat corporate rate

Since the Tax Cuts and Jobs Act of 2017, the US federal corporate income tax rate has been a flat 21%. This replaced a graduated rate structure that topped out at 35%. The flat 21% applies to all C-Corp taxable income, regardless of the amount. State corporate income taxes are levied on top of this, though Delaware, where most C-Corps are formed, does not tax income earned outside Delaware, which for a startup with no Delaware operations, often means minimal state corporate tax.Note that Delaware generally does not impose corporate income tax on a corporation with no Delaware-source income, but many startups will owe Delaware franchise tax regardless. Also, the real state income tax exposure is usually in the operating states (nexus/apportionment).

Double taxation

The C-Corp double taxation problem is real but frequently overstated. Here is the actual mechanics: the C-Corp pays 21% tax on its profits. If it distributes those profits as dividends to a non-resident foreign founder, the dividend is subject to US withholding tax - 30% at the default rate, reduced by treaty (often to 15% or lower for founders in treaty countries). So on $100 of profit, the C-Corp pays $21 in corporate tax, leaving $79. If that $79 is distributed as a dividend, 30% ($23.70) is withheld, leaving you $55.30. Effective combined rate: approximately 45%.

However, most growth-stage founders do not distribute all their profits. The C-Corp retains earnings and reinvests them. In that scenario, only the 21% corporate rate applies, no dividend withholding until you actually distribute. And a founder who eventually exits via a sale of shares may find that the capital gains treatment on exit is more efficient than dividend extraction along the way.

For founders in strong treaty countries, UK, Germany, Canada, France, Australia, dividend withholding rates are typically reduced to 5% or 15% depending on ownership percentage. This materially changes the double taxation calculation.

Why investors require Delaware C-Corps

The commercial standard for US VC-backed companies is the Delaware C-Corporation. This is not arbitrary. Delaware's General Corporation Law is the most extensively litigated and interpreted corporate statute in the US. The Court of Chancery provides specialist, efficient resolution of corporate disputes. Standard form investment documents, Series Seed, Series A term sheets, SAFEs, convertible notes, are all drafted for Delaware C-Corps. Deviating from this standard creates legal work and cost that investors do not want to absorb.

Additionally, many VC fund structures create tax complications when investing in pass-through entities. An LP in a VC fund who is a tax-exempt institution, a university endowment, a pension fund, does not want to receive Unrelated Business Taxable Income (UBTI), which can arise when a pass-through entity (like an LLC) distributes income. A C-Corp distributing dividends does not create UBTI. This is a structural reason, not just convention, for the C-Corp preference.

Equity and stock options

One of the most important practical advantages of the C-Corp for companies that plan to hire or compensate people with equity is the clean, well-understood framework for stock and options. A Delaware C-Corp can issue Incentive Stock Options (ISOs) to US employees under Section 422 of the Internal Revenue Code, a tax-advantaged form of equity compensation that allows employees to defer tax and potentially qualify for long-term capital gains rates on exit.

An LLC can issue equity-equivalent instruments, units, profits interests, but the tax treatment is more complex, the documentation is less standardised, and the employee experience is less familiar. Most US employees with equity experience expect stock and options, not LLC units. If building a US team with meaningful equity compensation is part of your plan, the C-Corp structure is significantly more practical.

Section 83(b) elections: Founders receiving equity in exchange for services, or receiving restricted stock that vests over time, should be aware of the Section 83(b) election, which allows you to elect to be taxed on the value of the equity at grant rather than at vesting. This can be extremely valuable if the equity is low-value at grant and high-value at vesting. The election must be filed within 30 days of the grant. Missing the window cannot be corrected. We cover this in detail in Part 5.

Delaware vs other states for C-Corps

For C-Corps, Delaware is the default for good reason, so investor expectations, legal infrastructure, and the Court of Chancery. There are very few situations where a non-US founder should form a C-Corp outside Delaware. If your investors, lawyers, and advisors all expect Delaware, that expectation should govern.

One exception worth noting: if you are forming a C-Corp purely as a domestic operating company with no VC plans and no investor expectations, for example, a service business that simply wants corporate tax treatment, then your operating state (where your employees and customers are) may be more practical than Delaware, as it avoids the need to register as a foreign corporation in your operating state while also maintaining Delaware.

Section 83(b) Election

IRC §83

https://www.law.cornell.edu/uscode/text/26/83

Treasury Reg. §1.83-2 (83(b) rules)

https://www.law.cornell.edu/cfr/text/26/1.83-2

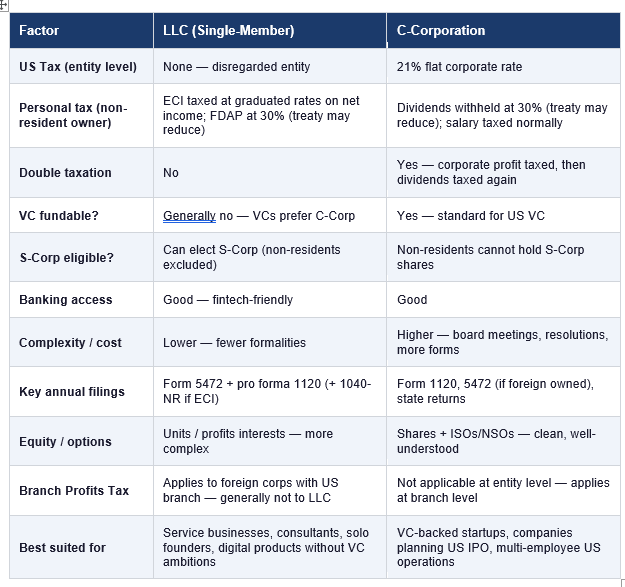

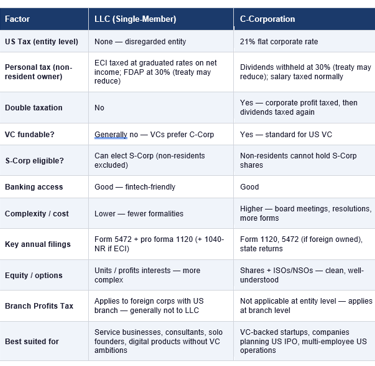

6. LLC vs C-Corp: Comparison Matrix

The table below summarises the key differences between an LLC (single-member, foreign-owned) and a Delaware C-Corp for a non-US founder. This is intended as a quick-reference tool — each row is discussed in more detail in the relevant sections of this guide.

How to read this table: This comparison reflects the most common scenario, a foreign-owned single-member LLC versus a Delaware C-Corp with a foreign founder. Multi-member LLCs, LLC-to-Corp conversions, and treaty-modified outcomes will vary. Use this as a starting framework, not a substitute for advice on your specific structure.

7. The Branch Profits Tax - What it is and when it catches you

The Branch Profits Tax (BPT) is a second layer of US tax that applies specifically to foreign corporations operating in the US through a branch, rather than a separately incorporated US subsidiary. It is designed to mirror the withholding tax that would apply if a US subsidiary distributed dividends to its foreign parent, and to prevent foreign corporations from avoiding dividend withholding simply by operating directly rather than through a US subsidiary.

The BPT applies at a rate of 30% (reducible by treaty) on what the IRS calls "dividend equivalent amount", essentially the portion of the branch's US earnings that are deemed to have been repatriated to the foreign parent. It is levied in addition to the regular corporate income tax on the branch's ECI.

When does the BPT apply to non-US founders?

For most non-US founders forming a US LLC or C-Corp, the Branch Profits Tax is not directly relevant, it applies to foreign corporations operating through US branches, not to separately incorporated US entities. However, there are two scenarios where founders need to be aware of it:

– If a foreign corporation (your home country company) operates directly in the US as a branch, without forming a separate US entity, it will face the BPT on top of regular ECI taxation.

– If your structure involves a foreign parent company with a US LLC or C-Corp subsidiary, certain repatriation transactions may be characterised in ways that the BPT reaches, depending on how they are structured and the applicable treaty.

For most founders using a clean US LLC or C-Corp structure, the BPT will not be a primary concern. But it is worth understanding, particularly if your structure involves a foreign parent entity actively doing business in the US without a separately incorporated US subsidiary.

IRC §884 — Branch Profits Tax

https://www.law.cornell.edu/uscode/text/26/884

IRS — Branch Profits Tax Overview (Pub 519 reference)

https://www.irs.gov/publications/p519

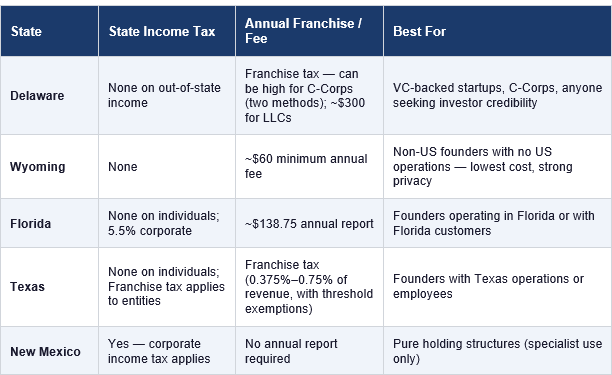

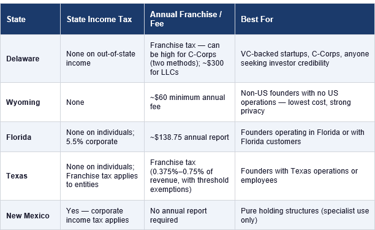

8. Choosing your State: Delaware, Wyoming, Florida, Texas - and Others

Every US LLC and corporation is formed in a specific state. The state of formation affects your formation cost, annual maintenance cost, tax obligations, privacy protections, and, for LLCs particularly, the legal framework governing your entity. For most founders, the choice narrows to four or five states, each with distinct advantages.

Delaware - the institutional standard

Delaware is the default state for C-Corps, and for good reason: it has the most developed corporate law in the US, the most experienced business court (the Court of Chancery), the most extensive case law interpreting corporate documents, and is expected by US institutional investors without exception.

For LLCs, Delaware is also commonly used, though the advantages are less overwhelming compared to states like Wyoming. Delaware's LLC law is flexible and well-understood, but Delaware's franchise tax, a fixed annual fee for LLCs, and its corporate franchise tax for C-Corps deserve attention. For C-Corps, Delaware's franchise tax is calculated using one of two methods: the Authorized Shares Method and the Assumed Par Value Capital Method. Many early-stage founders are surprised to find that their Delaware C-Corp owes thousands of dollars in franchise tax calculated on their total authorised shares, when switching to the Assumed Par Value Capital Method would reduce this to the minimum ($400 annually). Always calculate using both methods and pay the lower one.

Delaware franchise tax trap: If you receive a Delaware franchise tax bill calculated using the Authorized Shares Method and you have a large number of authorised shares (common in VC-backed startups), the bill can appear shockingly high, sometimes tens of thousands of dollars. Always request recalculation using the Assumed Par Value Capital Method before paying.

Wyoming - the founder-friendly alternative

Wyoming has emerged as a popular alternative for non-US founders forming LLCs, particularly those who do not need the VC credibility of Delaware and want to minimise annual costs and administrative burden. Wyoming's advantages include:

– No state corporate or individual income tax

– Very low annual fees — typically around $60 minimum

– Strong privacy protections — Wyoming does not require member names to be listed in public filings

– No publication requirements (unlike some other states)

– A well-developed LLC statute that has been updated to reflect modern practice

Wyoming is well-suited to non-US founders who are forming a US LLC primarily to access US banking and payment infrastructure, who have no US employees, no US office, and no near-term VC ambitions, and who want to minimise their annual compliance burden and cost. It is less suitable if you expect to raise US institutional capital, hire US employees, or operate substantially within a specific US state, because in those cases you will likely need to register as a foreign entity in that state regardless of where you formed.

Florida and Texas - operating state formations

If you have real US operations, so employees, customers, or a physical presence, in a specific state, it is often practical to form your entity in that state rather than in Delaware or Wyoming and then register as a foreign entity in your operating state. Florida and Texas are both no-income-tax states with significant business activity, making them popular choices for founders who are genuinely operating there.

Florida has no personal income tax and no corporate income tax on partnerships or LLCs taxed as pass-throughs. Its corporate income tax (5.5%) applies to C-Corps. Florida's annual report fee is modest. Texas has no personal income tax but applies a franchise tax to most business entities above a revenue threshold, the rate is 0.375% for wholesale/retail businesses and 0.75% for others, with exemptions for small businesses below a certain revenue level. Both states are reasonable choices if your business genuinely operates there.

The foreign qualification problem

Here is a point that many formation guides omit: if you form your LLC in Delaware or Wyoming but then hire employees, maintain an office, or conduct business in another state, say, California or New York, you are typically required to register your entity as a foreign LLC (or foreign corporation) in that state. This costs money, requires a registered agent in that state, and creates state tax filing obligations there.

This means that a Wyoming LLC with a Texas-based employee and a California customer may need to be registered in both Texas and California, paying annual fees and filing tax returns in both states, plus maintaining Wyoming registration. The "cheap" Wyoming formation can become significantly more expensive once you factor in multi-state registration requirements.

The practical implication: if you have clear geographic concentration of your US operations, form in that state (or Delaware if VC-relevant). If you have no US operations and are forming purely for banking/payment access, Wyoming or a comparable low-cost state is a sensible choice.

State comparison at a glance

9. Registered Agent - What it is, what it Costs, and how to Choose

Every US LLC and corporation is required to maintain a registered agent in its state of formation. The registered agent is a person or entity with a physical address in that state who is available during business hours to receive service of process, legal documents, lawsuits, government correspondence, on behalf of the company.

For a non-US founder who is not physically based in the US, the registered agent is particularly important because it is your US legal address of record. If someone sues your company, the lawsuit is served on your registered agent. If the state government sends a compliance notice, it goes to your registered agent. If you miss correspondence here, because your registered agent is not working or because you have not updated your details, you may miss deadlines or legal proceedings without knowing about them.

What registered agents actually do

A registered agent receives and scans mail and legal documents, forwards them to you promptly, maintains a record of documents received, and maintains a physical address in the state of formation. Many registered agent services also provide additional services: annual report reminders, compliance alerts, document storage, and forwarding of general business correspondence.

Cost and options

Registered agent services are widely available and relatively inexpensive. The major national providers, like Northwest Registered Agent, Registered Agents Inc, InCorp, CT Corporation, and National Registered Agents (NRAI), charge between $50 and $300 per year per state. Formation services like Stripe Atlas, Firstbase, and Doola typically include registered agent service for the first year as part of their formation package.

For non-US founders, the choice of registered agent is primarily about reliability and responsiveness. You are not physically present to monitor for compliance correspondence, so you need a service that scans and forwards promptly and provides clear digital records. National providers with established track records are generally preferable to bargain-tier options for this reason.

10. Operating Agreements, Bylaws, and Formation Documents

Formation documents are the legal foundation of your entity. Getting them right matters and not just at formation, but for banking, investor due diligence, and any future dispute between founders or with third parties.

LLC Operating Agreement

An operating agreement is the governing document of an LLC. It sets out the ownership structure, how decisions are made, how profits and losses are allocated, what happens if a member wants to exit or transfer their interest, and how the LLC can be dissolved. Many states do not legally require a written operating agreement, but not having one is a mistake that can create serious problems.

For a single-member LLC, the operating agreement is important because it reinforces the separation between the LLC and the individual owner, a distinction that matters for both liability protection and tax purposes. It also governs the relationship between you and the entity, including how you as the manager are authorised to act on the entity's behalf. Banks frequently request it as part of account opening. Clients may request it as part of contract due diligence.

For a multi-member LLC, the operating agreement is critical, it is the primary document governing the relationship between members. It should cover: ownership percentages, voting rights, decision-making thresholds (simple majority vs supermajority vs unanimity), profit and loss allocation, member contribution obligations, restrictions on transfer of membership interests, buy-sell provisions, and dissolution procedures. Without a well-drafted operating agreement, disputes between members are resolved by state default rules, which may not reflect what the members actually intended.

C-Corp formation documents

A C-Corp is governed by a more extensive set of documents than an LLC. The key formation documents are:

– Certificate of Incorporation (or Articles of Incorporation): the document filed with the state that creates the corporation. It sets out the company's name, registered agent, authorised shares, and any special provisions.

– Bylaws: the internal governance document that sets out how the corporation is managed - board composition, officer roles, meeting procedures, voting requirements, amendment procedures.

– Initial Resolutions: corporate actions taken by the initial board of directors authorising the issuance of stock, appointing officers, opening bank accounts, and approving the form of bylaws.

– Stock Purchase Agreements: the documents through which founders receive their initial shares, typically accompanied by a Restricted Stock Purchase Agreement if shares vest over time.

– Shareholder Agreements: where there are multiple founders, a shareholder agreement may cover right of first refusal on share transfers, co-sale rights, voting agreements, and founder vesting acceleration provisions.

For VC-backed companies, investors will conduct legal due diligence on all of these documents before closing a round. Clean, properly executed formation documents make that process faster and cheaper. Formation documents that have not been properly executed, that contain errors, or that are missing entirely create delay and additional legal cost.

11. Beneficial Ownership Information (BOI) Reporting

The Corporate Transparency Act (CTA), which came into effect on January 1, 2024, introduced a new federal reporting requirement for most US LLCs and corporations: Beneficial Ownership Information reporting, filed with the Financial Crimes Enforcement Network (FinCEN), a bureau of the US Treasury Department. Following a major interim final rule issued by FinCEN in March 2025, the scope has been dramatically narrowed.

What BOI reporting requires (for foreigners owning US companies)

All entities formed in the United States, so including the typical single-member LLC owned by a foreign founder, are now fully exempt from BOI reporting requirements. This means there is generally no obligation to report the foreign beneficial owner’s details (full legal name, date of birth, current address, or a copy of a government-issued ID such as a passport, national ID, or driver’s licence) to FinCEN.

The information (when required) is filed online through FinCEN’s BOI filing portal. It is not publicly accessible so it is available only to authorised law enforcement and certain financial institutions. Although US-formed companies are now exempt, the penalties for non-compliance under the prior rules remain on the books: civil penalties of up to $591 per day (subject to annual adjustment) and criminal penalties of up to $10,000 and two years in prison for wilful violations.

Filing deadlines

US-formed entities (domestic LLCs and corporations) have no current BOI filing obligation and no update requirements, regardless of formation date or changes in ownership or control. (The original deadlines that applied until early 2025 - January 1, 2025 for pre-2024 entities, 90/30 days for newer ones, no longer apply to them.)

BOI litigation notice: The BOI reporting requirements have been subject to ongoing legal challenges since their introduction, with various court orders temporarily blocking enforcement at different points. The status of these requirements shifted multiple times, culminating in FinCEN’s March 2025 interim final rule that exempts all domestically formed entities and their beneficial owners (including foreign ones). Before relying on any guidance about current BOI obligations, confirm the current status with a qualified US advisor as this is an area where the rules have been in active flux.

12. Common Formation Mistakes Non-US Founders Make

The formation process is relatively straightforward. The mistakes most non-US founders make are not in the paperwork but they are in the decisions made before and after the paperwork.

Choosing the wrong entity without understanding why

The most common mistake is forming an LLC because someone else said to, or forming a C-Corp because that is what appeared first in a search, without understanding the tax implications of the choice. The entity decision should be driven by your specific circumstances so your home country, your income type, your hiring plans, your funding plans, and your extraction strategy. Defaulting to either option without working through those factors is how founders end up with structures that are inefficient or actively wrong for their situation.

Forming in the wrong state

Forming in Delaware or Wyoming because those are the popular choices and without considering where your business actually operates, can create a need to register as a foreign entity in your operating state anyway, doubling your annual compliance obligations and cost for no real benefit.

Not getting an operating agreement

Skipping the operating agreement for a single-member LLC because it seems unnecessary is a mistake that creates problems at the bank, with clients, and in any future dispute. A simple, well-drafted operating agreement is not expensive and takes little time. Not having one is a false economy.

Treating the EIN as proof of compliance

Getting an EIN from the IRS is a straightforward process, and many founders treat it as the end of the formation process. It is not. The EIN is simply a tax identification number. It does not mean you have filed the right forms, set up the right compliance processes, or understood your ongoing obligations. Founders who stop at EIN and then do nothing for 12 months typically discover the Form 5472 problem at exactly the wrong moment.

Not telling their home country accountant

Forming a US entity without informing your home country accountant is one of the most reliably expensive mistakes a founder can make. Your home country obligations do not disappear because you have a US entity. In many cases, forming a US entity creates new home country obligations so CFC reporting, foreign asset disclosure, changes to your personal tax position, that your home country accountant needs to know about in order to advise you correctly.

13. Formation Costs — A Realistic Breakdown

Formation costs vary by state, entity type, and whether you use a professional service or attorney. The following figures are indicative based on typical 2025 costs and should be verified against current state fees before relying on them.

LLC formation

Delaware LLC: State filing fee approximately $90–$110. Registered agent approximately $50–$300 per year. Annual LLC tax: $300 flat. Total first-year cost excluding professional fees: $450–$700.

Wyoming LLC: State filing fee approximately $100. Registered agent approximately $50–$150 per year. Annual report fee: approximately $60 minimum. Total first-year cost excluding professional fees: $210–$400.

Florida LLC: State filing fee approximately $125. Annual report fee: approximately $139. Registered agent: approximately $50–$150. Total first-year cost excluding professional fees: $315–$415.

C-Corp formation

Delaware C-Corp: State filing fee approximately $89–$200 depending on authorised shares. Registered agent approximately $50–$300 per year. Annual franchise tax: minimum $400 using Assumed Par Value Capital Method, potentially higher on Authorized Shares Method. Total first-year cost excluding professional fees: $540–$900+.

Professional fees

If you use a formation service — Stripe Atlas, Firstbase, Doola, Clerky, or similar, expect to pay $400–$1,500 for assisted formation, typically including registered agent for the first year. If you use an attorney for formation, expect $1,500–$5,000 for a basic LLC and $3,000–$10,000 for a C-Corp with full documentation (operating agreement or bylaws, shareholder agreements, founder equity, initial resolutions).

Ongoing annual compliance costs, excluding US tax preparation, typically run $500–$2,000 per year for an LLC (registered agent, state annual report, bookkeeping) and $1,500–$5,000 per year for a C-Corp (same plus more extensive governance and state filings). US tax preparation for foreign-owned entities adds $1,000–$5,000 per year depending on complexity. These are not optional costs and they are the price of maintaining a US entity correctly.

Before You Move to Part 3

Part 3 covers the step-by-step formation process, so exactly what you file, in what order, and what the EIN application looks like for a non-US resident without a Social Security Number. It also covers the ITIN, virtual office requirements, and the BOI filing process in practical detail.

Before you proceed, you should have a clear answer to the following from this part:

– LLC or C-Corp — and why, based on your specific situation

– Which state — and whether you will need to register in additional operating states

– Whether your business will generate ECI, FDAP income, or both — and what that means for your tax position

– Whether you have discussed the entity decision with both a US-qualified advisor and someone who understands your home country position

If those answers are clear, you are ready to form. If they are not, the time to resolve them is before you file anythin.

Antravia Advisory: We help non-US founders work through exactly these decisions, entity type, state, structure, and home country implications, before committing to a formation. If you would like to discuss your specific situation, get in touch.

Continue to Part 3: Formation — Step by Step →

References

1. Entity Classification (LLC vs Corporation)

IRS — Entity Classification (Check-the-Box Rules)

https://www.irs.gov/businesses/small-businesses-self-employed/business-structures

Form 8832 (Entity Classification Election)

https://www.irs.gov/forms-pubs/about-form-8832

Form 2553 (S-Corp Election)

https://www.irs.gov/forms-pubs/about-form-2553

S Corporation Eligibility Requirements (IRS)

https://www.irs.gov/businesses/small-businesses-self-employed/s-corporations

2. Effectively Connected Income (ECI)

IRS — Effectively Connected Income (ECI) Explained

https://www.irs.gov/individuals/international-taxpayers/effectively-connected-income-eci

IRS Publication 519 — U.S. Tax Guide for Aliens

https://www.irs.gov/forms-pubs/about-publication-519

IRC §864(c) — Definition of ECI (Cornell Law, official statute text)

https://www.law.cornell.edu/uscode/text/26/864

3. Engaged in a Trade or Business in the U.S. (ETBUS)

IRS — Trade or Business in the United States (Pub 519)

https://www.irs.gov/publications/p519#en_US_2023_publink1000222187

Treasury Regulations §1.864-2

https://www.law.cornell.edu/cfr/text/26/1.864-2

4. FDAP Income & Withholding

IRS — Withholding on Nonresident Aliens (FDAP)

https://www.irs.gov/individuals/international-taxpayers/withholding-of-tax-on-nonresident-aliens

IRC §871(a) — 30% withholding rule

https://www.law.cornell.edu/uscode/text/26/871

Form W-8BEN & W-8BEN-E Instructions (Treaty claims)

https://www.irs.gov/forms-pubs/about-form-w-8-ben

https://www.irs.gov/forms-pubs/about-form-w-8-ben-e

5. Section 1446 Partnership Withholding

IRS — Withholding on Foreign Partners (Section 1446)

https://www.irs.gov/businesses/partnership-withholding

Form 8804 / 8805 Instructions

https://www.irs.gov/forms-pubs/about-form-8804

https://www.irs.gov/forms-pubs/about-form-8805

6. Branch Profits Tax

IRC §884 — Branch Profits Tax

https://www.law.cornell.edu/uscode/text/26/884

IRS — Branch Profits Tax Overview (Pub 519 reference)

https://www.irs.gov/publications/p519

7. Corporate Income Tax (21% Rate)

IRS — Corporate Tax Information

https://www.irs.gov/businesses/corporations

IRC §11 — Corporate Tax Rate (21%)

https://www.law.cornell.edu/uscode/text/26/11

8. Delaware Corporate & LLC Law

Delaware Division of Corporations

https://corp.delaware.gov

Delaware General Corporation Law (DGCL)

https://delcode.delaware.gov/title8/

Delaware LLC Act

https://delcode.delaware.gov/title6/c018/

Delaware Franchise Tax Information

https://corp.delaware.gov/frtaxcalc/

9. BOI Reporting (Corporate Transparency Act)

FinCEN — Beneficial Ownership Information Reporting

https://www.fincen.gov/boi

Corporate Transparency Act (31 U.S.C. §5336)

https://www.law.cornell.edu/uscode/text/31/5336

10. Section 83(b) Election

IRC §83

https://www.law.cornell.edu/uscode/text/26/83

Treasury Reg. §1.83-2 (83(b) rules)

https://www.law.cornell.edu/cfr/text/26/1.83-2

11. Tax Treaties & Permanent Establishment

IRS — U.S. Tax Treaties

https://www.irs.gov/businesses/international-businesses/united-states-income-tax-treaties-a-to-z

U.S. Model Income Tax Convention (Treasury)

https://home.treasury.gov/policy-issues/tax-policy/treaties

12. EIN Application

IRS — Apply for an EIN

https://www.irs.gov/businesses/small-businesses-self-employed/apply-for-an-employer-identification-number-ein-online

About Antravia Advisory

Antravia Advisory is a US-based tax and accounting advisory firm headquartered in Winter Park, Florida, operating nationally and internationally.

We advise international businesses entering the United States and complex US companies operating across multiple states, entities, and revenue structures. Our work spans advanced tax strategy, multi-state sales tax oversight, cross-border structuring, and high-level accounting architecture for e-commerce brands, subscription and SaaS businesses, platform-based models, and multi-entity groups.

We work with founders and leadership teams who require technical precision, structural clarity, and financial frameworks built for scale, capital events, and long-term resilience.

The Non-US Founder’s Complete Guide to Running a US Business

Part 1 — Before You Start

Part 2 — Choosing Your US Entity

Part 3 — Formation

Part 4 — US Banking

Part 5 — US Federal Tax

Part 6 — US State Tax

Part 7 — Paying Yourself

Part 8 — Accounting and Bookkeeping

Part 9 — Annual Compliance Calendar

Part 10 — Hiring in the US

Part 11 — Intellectual Property and Contracts

Part 12 — Your Home Country Obligations

Part 13 — Applied Business Types

Part 14 — Exiting, Winding Down, or Restructuring

Disclaimer:

Content published by Antravia is provided for informational purposes only and reflects research, industry analysis, and our professional perspective. It does not constitute legal, tax, or accounting advice. Regulations vary by jurisdiction, and individual circumstances differ. Readers should seek advice from a qualified professional before making decisions that could affect their business.

See also our Disclaimer page

Antravia Advisory

Accounting built for complexity

Not legal advice, always verify with your Accountant

Email:

Contact us:

© 2025. All rights reserved. | Disclaimer | Privacy Policy | Terms of Use |

contact@antravia.com

Antravia LLC

941 W Morse Blvd suite 100

Winter Park

Florida

32789