Part 3: Formation - Step by Step

The Non-US Founder's Complete Guide to Running a US Business - Part 3 is a step-by-step formation guide for non-US founders. Learn how to form an LLC or C-Corp, obtain an EIN without an SSN, handle ITIN requirements, file BOI reports, manage 83(b) elections, and avoid costly formation mistakes.

THE NON-US FOUNDER'S COMPLETE GUIDE TO RUNNING A US BUSINESS

2/26/202625 min read

You have decided on your entity type. You have chosen your state. Now you need to actually form the entity, and as a non-US founder, several parts of that process work differently from what you may have read about in domestic-focused guides.

This part walks you through the complete formation process for both LLCs and C-Corps, step by step. It covers the EIN application in detail, a step that trips up many international founders, along with the ITIN, registered agents, virtual offices, operating agreements, bylaws, BOI reporting, and the most common mistakes made at the formation stage.

1. LLC Formation - Step-by-Step Walkthrough

Forming an LLC involves fewer mandatory documents than a C-Corp, but the process still requires careful attention to sequence and detail. The following walkthrough applies to a single-member LLC formed in Delaware or Wyoming, the two most common choices for non-US founders. State-specific variations are noted where they apply.

Before you start: what you need to have ready

Before you begin any filings, have the following ready:

– Your chosen entity name, checked for availability in your state of formation

– Your chosen state of formation and registered agent service

– A physical address for the registered agent (provided by your agent service)

– Your passport and personal identification documents

– A personal address, even a foreign address is acceptable for formation purposes

– The names and addresses of all members (owners) of the LLC

– If using a formation service: your payment method and account details

The formation steps

STEP 1: Choose and reserve your company name — Search your state's business entity database to confirm the name is available. Delaware's Division of Corporations and Wyoming's Secretary of State both offer free online name searches. Your chosen name must include a designator, "LLC," "L.L.C.," or "Limited Liability Company." Name reservation is optional in most states and costs a small additional fee if you want to hold the name while you prepare your documents.

STEP 2: Appoint your registered agent — Select and engage a registered agent service in your formation state before filing. Your agent provides the official registered office address that appears in your formation documents. You need this address before you can complete the Articles of Organization. Most agents allow you to sign up online within minutes.

STEP 3: Prepare and file your Articles of Organization — The Articles of Organization is the document you file with the state to legally create your LLC. In Delaware, this is filed with the Division of Corporations. In Wyoming, with the Secretary of State. The Articles typically require: your LLC name, your registered agent's name and address, and the name and address of the organizer (the person filing — this can be you, your attorney, or your formation service). Some states require additional information, such as the names of the initial members or the LLC's purpose. In Delaware, the Articles are intentionally minimal, you do not list member names publicly, which provides privacy.

STEP 4: Pay the state filing fee — Filing fees vary by state. Delaware charges approximately $90–$110. Wyoming charges approximately $100. Payment is typically made online by credit card. Some states offer expedited filing for an additional fee, usually $50–$150 for same-day or next-day processing.

STEP 5: Receive your Certificate of Formation — Once the state processes your filing, it issues a Certificate of Formation (or Certificate of Organization in some states) confirming that your LLC exists. In Delaware, standard processing takes approximately 7–10 business days; expedited options can reduce this to same-day or 24 hours. Keep this document, you will need it for banking, contracts, and various registrations.

STEP 6: Draft and execute your Operating Agreement — Your Operating Agreement is a private document, it is not filed with the state in most cases, but it is critical. It governs the internal operation of your LLC: ownership, decision-making authority, profit and loss allocation, and procedures for adding members, handling exits, and dissolving the entity. For a single-member LLC, this document also confirms that you are the sole member and sole manager, and that you have authority to act on behalf of the entity. Execute it with your signature and keep it with your company records. Most banks will request it when you open your business account.

STEP 7: Obtain your EIN from the IRS — Your Employer Identification Number is your LLC's federal tax identification number. It is required to open a US bank account, hire employees, and file US tax returns. The EIN application process for non-US residents without a Social Security Number is covered in detail in Section 3 of this Part.

STEP 8: File your Beneficial Ownership Information (BOI) report — Under the Corporate Transparency Act, most newly formed LLCs are required to file a BOI report with FinCEN within 90 days of formation (30 days for entities formed after January 1, 2025). This report identifies the beneficial owners of the entity. See Section 7 of this Part for the full BOI filing process. Note the ongoing litigation around BOI requirements and confirm current status before filing.

STEP 9: Register in additional states if required — If your LLC will have employees, maintain an office, or regularly conduct business in a state other than your formation state, you are generally required to register as a foreign LLC in that state. This involves filing a Certificate of Authority (or similar) with that state, providing a registered agent in that state, and paying the applicable fees. Do not overlook this as failure to register in an operating state can result in penalties, inability to bring legal claims in that state, and back taxes.

STEP 10: Open your US bank account — With your Certificate of Formation, Operating Agreement, and EIN in hand, you are ready to apply for a US business bank account. Banking for foreign-owned entities is covered in full in Part 4, but the sequencing matters. You need the EIN before the bank will process your application, and many banks also require the executed Operating Agreement.

2. C-Corp Formation — Step-by-Step Walkthrough

C-Corp formation involves more documents and a more formal governance structure than an LLC, but the process is well-standardised for Delaware, particularly for VC-backed startups using specialist formation services or startup attorneys who have done it hundreds of times.

Before you start: what you need to have ready

– Your chosen company name, checked for availability in Delaware

– Your registered agent service in Delaware

– The names and addresses of all initial directors (can be the founder(s))

– Your planned capital structure, number of authorised shares and par value

– The names and addresses of all initial shareholders (founders) and their proposed equity allocation

– Your passport and personal identification documents

– If you have multiple founders: agreement in principle on equity split, vesting schedule, and governance rights

Capital structure decisions before you file

Before filing your Certificate of Incorporation, you need to decide on your authorised share structure. This matters for two reasons: Delaware's franchise tax is partially calculated based on authorised shares, and your authorised share count affects how much equity flexibility you have as you grow.

The most common approach for early-stage startups is to authorise 10,000,000 shares of common stock at a par value of $0.0001 per share. This gives you significant flexibility to issue founder shares, create an option pool, and issue preferred stock to investors, all without amending the certificate, which requires board and shareholder approval. Some founders authorise blank check preferred stock, giving the board flexibility to issue preferred stock with terms defined at the time of issuance, this is standard for VC-funded companies.

Par value and franchise tax: Delaware calculates franchise tax under the Authorized Shares Method based on your total authorised shares. With 10,000,000 authorised shares, this can produce a very large franchise tax bill. Always request recalculation under the Assumed Par Value Capital Method and for early-stage companies with low paid-in capital, this typically produces a minimum tax of $400. Never pay a Delaware franchise tax bill without verifying which calculation method was used.

The formation steps

STEP 1: Choose and reserve your company name — Search Delaware's Division of Corporations name database. Corporate names must include a designator: "Corporation," "Corp.," "Incorporated," "Inc.," or "Company" (though "Company" alone is not sufficient). Name reservation is available for 120 days at a cost of approximately $75.

STEP 2: Appoint your Delaware registered agent — As with an LLC, you need a registered agent with a physical Delaware address. Select your agent before filing, their address appears in your Certificate of Incorporation.

STEP 3: Draft and file your Certificate of Incorporation — The Certificate of Incorporation (sometimes called the Charter) is filed with the Delaware Division of Corporations. It sets out: your corporate name, the registered agent's name and Delaware address, the total number of authorised shares and par value, and any special provisions (blank check preferred, protective provisions, etc.). Delaware filing fees are based on authorised shares, for a standard 10,000,000-share structure at $0.0001 par value, the base fee is typically $89–$200. Expedited filing (24 hours) costs approximately $100 additional; same-day is approximately $200–$500 additional.

STEP 4: Receive your Certificate of Incorporation — Delaware issues a stamped Certificate of Incorporation once the filing is processed. This is your proof of existence. Keep it permanently, you will need it for banking, investor due diligence, and various regulatory filings.

STEP 5: Hold the organisational meeting and adopt bylaws — The initial directors (or incorporator, if no directors are named) hold an organisational meeting, which for a single founder is typically documented by written consent rather than a formal meeting. At this meeting, the directors: adopt the bylaws, appoint the initial officers (CEO, CFO, Secretary), authorise the issuance of founder shares, approve the opening of bank accounts, and authorise other initial corporate actions. All of this should be documented in writing, as board resolutions or written consent in lieu of meeting, and kept in your corporate records book.

STEP 6: Issue founder shares and execute stock purchase agreements — Founder shares are issued pursuant to a Restricted Stock Purchase Agreement (RSPA), which sets out the vesting schedule, repurchase rights, and other conditions. For a non-US founder receiving shares in a US C-Corp, the tax treatment of those shares, and the Section 83(b) election, requires immediate attention. See the Section 83(b) discussion below and in Part 5.

STEP 7: File Section 83(b) election if applicable — If your founder shares are subject to vesting (the company has the right to repurchase unvested shares if you leave), you must file a Section 83(b) election with the IRS within 30 days of the share grant. This is a critical step that cannot be corrected if missed. See Section 6 of this Part for the full process.

STEP 8: Obtain your EIN from the IRS — Same process as for an LLC, see Section 3 of this Part. The C-Corp needs an EIN before it can open a bank account, run payroll, or file tax returns.

STEP 9: File your BOI report with FinCEN — Same obligation as for an LLC, see Section 7 of this Part. File within 90 days of formation (or 30 days if formed after January 1, 2025), subject to current litigation status.

STEP 10: Register in operating states — If your C-Corp will have employees, maintain an office, or regularly conduct business in states other than Delaware, you must register as a foreign corporation in those states and appoint a registered agent there. This is mandatory and not optional, and failure to do so can result in penalties and loss of the right to bring legal claims in that state.

STEP 11: Open your US bank account — With your Certificate of Incorporation, bylaws, EIN, and board resolutions in hand, apply for your US business bank account. C-Corps typically face slightly more documentation requirements than LLCs, as banks want to see the governance documents as well as the formation certificate.

3. Getting Your EIN as a Non-US Resident

The Employer Identification Number (EIN) is the single most important number your US entity will have. It is your entity's federal tax identification number, used on every US tax return, every bank account application, every payroll filing, and most business contracts. Getting it is not complicated, but there are specific rules for non-US residents that differ significantly from the domestic process.

The core issue: you have no Social Security Number

The standard EIN application process for US residents involves an online application at IRS.gov that takes approximately five minutes and produces an EIN immediately. This process requires the applicant to have a US Social Security Number (SSN) or Individual Taxpayer Identification Number (ITIN). Non-US residents who have neither, which is most international founders before they have done any US tax filings, cannot use the online application.

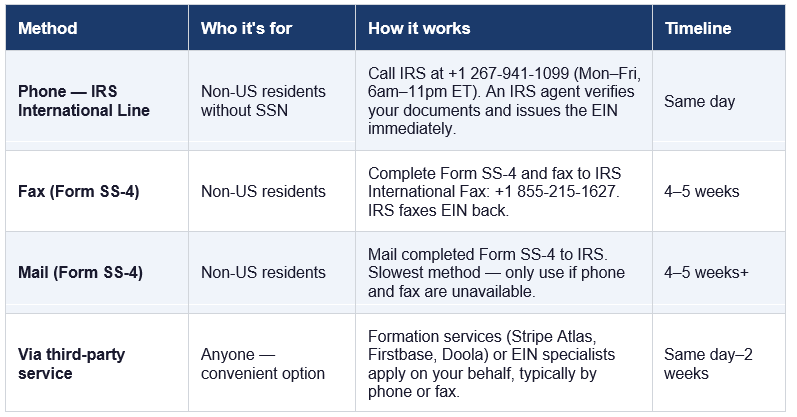

This is not a dead end. There are three methods available to non-US residents, and one of them, the phone application, is fast, free, and results in an EIN on the same call. The table below sets out all your options.

The phone application - step by step

The phone method is the fastest and most reliable option for non-US residents. Here is exactly how it works:

1. Prepare Form SS-4 before you call. Complete the form in full, the IRS agent will ask you questions directly from this form. Key fields: Line 1 (legal name of entity), Line 4a (mailing address so your foreign address is fine), Line 7a/7b (name and SSN/ITIN of responsible party, use your name and write "Foreign" where SSN is requested if you do not yet have an ITIN), Line 9a (type of entity, LLC or corporation), Line 10 (reason for applying, typically "Started new business"), Line 11 (date the entity was or will be formed).

2. Call the IRS International EIN line: +1 267-941-1099. This line is available Monday through Friday, 6:00am to 11:00pm Eastern Time. Wait times vary so calling early in the morning or mid-week typically produces shorter waits.

3. Confirm you are the responsible party. The IRS agent will verify that you are calling on behalf of the entity and that you are authorised to receive the EIN. You do not need an SSN or ITIN to complete this step, you are applying for the entity, and the entity itself has no SSN.

4. Answer the agent's questions. The agent will work through Form SS-4 with you, so confirming the entity name, type, address, principal business activity, and other basic details. Answer clearly and have your completed SS-4 in front of you.

5. Receive your EIN immediately. At the end of the call, the agent will provide your EIN verbally and will send a confirmation letter (CP 575) to your mailing address, typically within four weeks. Write down the EIN immediately, you need it for banking and other registrations before the letter arrives.

Important: The EIN confirmation letter (CP 575) is not always required for banking, but some banks, particularly traditional banks, will request it. If you are using a fintech bank like Mercury or Relay, the EIN number itself is usually sufficient. If you will be banking with a traditional institution, be aware that the CP 575 can take four to six weeks to arrive.

Using a third-party EIN service

If you prefer not to navigate the IRS phone line yourself, numerous services will apply for an EIN on your behalf. Formation services like Stripe Atlas, Firstbase, and Doola typically include EIN application as part of their formation package. Standalone EIN services also exist and typically charge $50–$100 for the service. If using a third-party service, confirm that they apply by phone or fax (not online, which requires the applicant's SSN) and that they will provide you with the EIN confirmation in writing once received.

One important restriction: one EIN per entity

The IRS issues one EIN per entity. If you lose your EIN or cannot locate your confirmation letter, you can retrieve it by calling the IRS Business and Specialty Tax Line (+1 800-829-4933), but you cannot be issued a second EIN for the same entity. Keep your EIN in a secure, accessible location from the moment you receive it.

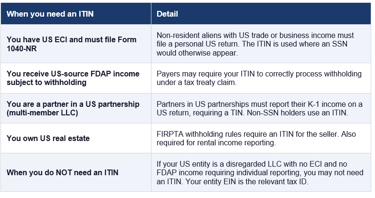

4. The ITIN - What it is, when you need one, and how to get it

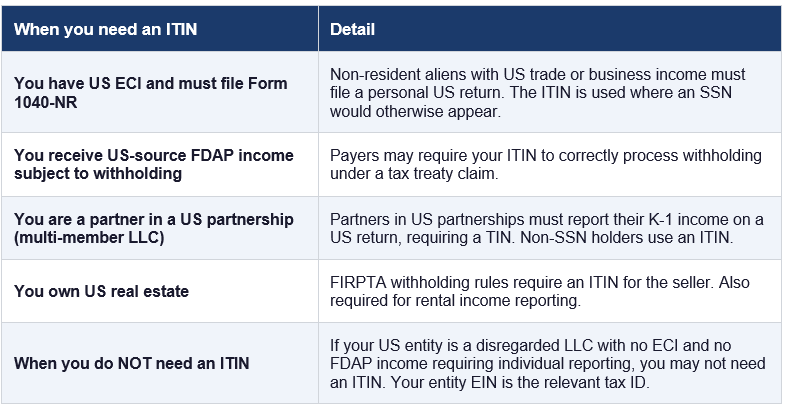

The Individual Taxpayer Identification Number (ITIN) is a personal tax identification number issued by the IRS to individuals who need to file US tax returns or be identified for US tax purposes, but who do not qualify for a Social Security Number. It is a nine-digit number in the format 9XX-XX-XXXX.

Many non-US founders mistakenly believe they need an ITIN as part of the entity formation process. In most cases, you do not need an ITIN at formation, your entity's EIN is the relevant tax identifier for entity-level purposes. The ITIN is a personal identifier, relevant when you as an individual have US tax reporting obligations.

How to apply for an ITIN

ITIN applications are filed on Form W-7 (Application for IRS Individual Taxpayer Identification Number). The process is more involved than the EIN application and requires original identity documents or certified copies.

Option 1: Mail Form W-7 with original documents

You can mail a completed Form W-7 to the IRS ITIN Operations unit, along with original identity documents (typically your passport) or certified copies. The IRS will review your documents, issue your ITIN, and return the original documents. Processing time is typically seven to eleven weeks, though during peak periods (January to April) this can extend to fourteen weeks or more. Mailing your original passport overseas involves risk, many applicants prefer one of the alternatives below.

Option 2: Certifying Acceptance Agent (CAA)

A Certifying Acceptance Agent is an individual or entity authorised by the IRS to verify original identity documents and certify copies for ITIN application purposes. Using a CAA means you do not need to mail your original passport, the CAA certifies a copy and submits it with your W-7. CAAs include many US accountants and tax professionals, some notaries, and some foreign-based professionals authorised by the IRS. This is the most practical option for most non-US founders, find a US accountant or tax professional who is an authorised CAA and can handle the process for you.

Option 3: IRS Taxpayer Assistance Centers

If you are physically in the US, you can visit an IRS Taxpayer Assistance Center (TAC) with your original documents. TAC staff can review your documents in person and forward your W-7 application to the ITIN unit. You must make an appointment in advance. This option is only practical if you are already in the US for other reasons.

ITIN expiry and renewal

ITINs that have not been used on a US federal tax return for three consecutive tax years expire and must be renewed before they can be used again. If your ITIN expires, you apply for renewal on a new Form W-7. If your ITIN was issued before 2013 and has specific middle digits, it may expire on a rolling schedule regardless of usage. Check the expiry status of any existing ITIN before relying on it for a filing.

5. Virtual Office and US Mailing Address - Requirements, Options, and Costs

As a non-US founder, you need a way to receive US business correspondence, from the IRS, from state agencies, from clients, and from your bank. Your registered agent handles formal legal correspondence in your formation state, but there are many other types of correspondence that go to your business mailing address, not your registered agent address.

Do you need a US business address?

The short answer is: for most purposes, you can use a foreign address. The IRS accepts foreign addresses on Form SS-4, Form 5472, and most other federal filings. Delaware and Wyoming accept foreign member addresses in LLC filings. Most fintech banks, Mercury, Relay, Brex, accept foreign addresses for account holders.

However, a US business address is practically useful for several reasons:

– Some traditional US banks require a US business address, not just a registered agent address, to open a business account

– US clients and prospects may be more comfortable with a US-visible address on your website and correspondence

– Certain state-level registrations require a US address for the entity or its managers

– If you want to receive general business mail, cheques, vendor correspondence, government letters, you need somewhere for it to go in the US

Virtual office services

Virtual office services provide a physical US street address (not a PO box) that you can use as your business address. They receive your mail, scan it, and forward it to you digitally. Some also offer occasional access to physical meeting rooms, a local phone number with call answering, and related services.

The major providers include Regus, WeWork (on-demand), Alliance Virtual Offices, iPostal1, Anytime Mailbox, and Stable. Costs range from approximately $50 to $200 per month depending on the location (a Manhattan address costs more than a suburban address) and the level of service included.

Key things to verify when selecting a virtual office service for banking purposes: the address must be a real street address, not a PO box or PMB (Private Mailbox) number. Some banks specifically ask whether an address is a UPS Store, The Mailbox Store, or similar commercial mail receiving agency, and if it is, they may decline. Regus and WeWork addresses are generally accepted because they are genuine office building addresses.

Formation service addresses

Some formation services, particularly those targeting international founders, provide a US business address as part of their package. Firstbase, for example, provides a US address in its formation tier. These addresses work well for IRS correspondence and general business use, but should be checked for bank acceptability before relying on them as your primary banking address.

PO box limitation: The IRS accepts PO boxes for correspondence in some contexts, but many banks and state registrations do not. If your only US address is a PO box or a commercial mail receiving agency registered as a PMB, you may encounter friction with banking, state filings, and some client due diligence requests. A genuine street address, even from a virtual office service, is significantly more useful.

6. The Section 83(b) Election — The 30-Day window you cannot miss

If you receive equity in your US entity in exchange for services, or if you receive equity that is subject to a vesting schedule with repurchase rights, the Section 83(b) election is one of the most important tax decisions you will make as a founder. It must be filed within 30 days of the equity grant. Missing the window cannot be corrected. There are no extensions. The IRS does not accept late elections.

What Section 83(b) does

Under Section 83 of the Internal Revenue Code, when you receive property (including shares) in exchange for services, and that property is subject to a substantial risk of forfeiture (a vesting schedule with company repurchase rights is a classic example), you are normally taxed on the value of the property when it vests, not when it is granted.

For a founder whose shares are worth pennies at grant but potentially millions at vesting, this creates an enormous tax problem: you may owe ordinary income tax on the appreciated value of the shares when they vest, even if you have not sold them and have received no cash. The tax liability is real. The cash to pay it may not be available.

A Section 83(b) election allows you to elect to be taxed at grant rather than at vesting. If you make the election when your shares are worth very little, which is typical at the time of founding, you recognise a very small amount of ordinary income at grant and nothing at vesting. When you eventually sell the shares, the difference between your sale price and your grant price is taxed as capital gains, not ordinary income, and if you hold for more than a year, it qualifies for long-term capital gains rates.

The economic logic: You file an 83(b) election, pay minimal tax on shares worth $0.001 each, and convert all future appreciation to capital gains. You do not file, and when your shares vest at $10 per share, you owe ordinary income tax on that appreciation, potentially at rates exceeding 37% federally plus state tax, with no cash in hand to pay it.

When Section 83(b) applies to non-US founders

Section 83(b) is a US tax provision and applies to US tax obligations. For a non-US founder who is a non-resident alien, the analysis is more nuanced: if you do not have US-source compensation income from your equity, you may not have a US tax liability at vesting in the same way a US resident would. However, filing the 83(b) election is still frequently recommended for non-US founders in C-Corps for two reasons.

First, your tax residency status may change. If you later become a US resident, through a visa change, extended US presence, or green card, the election you did or did not make at founding becomes relevant to your US tax position. Second, the election is relevant to your home country tax position in some jurisdictions, and the documentation establishes the cost basis of your shares for future capital gains calculations everywhere.

Consult your US tax advisor about whether an 83(b) election is appropriate for your specific situation, particularly if you are a non-resident alien at the time of grant. Do not skip this step without getting a clear answer.

How to file a Section 83(b) election

6. Draft the election letter. The election is a written statement filed with the IRS — there is no official form. It must include: your name, address, and SSN or ITIN; a description of the property received; the date of transfer; the tax year for which the election is made; the nature of the restrictions on the property; the fair market value of the property at the time of transfer; and the amount paid for the property (typically the par value of the shares).

7. File within 30 days of the grant date. The election must be received by the IRS — not postmarked — within 30 days of the date the equity was transferred to you. Day one is the date of transfer, not the date you signed the stock purchase agreement.

8. Send to the IRS Service Center where you file your return. For non-resident aliens this is typically the IRS center in Austin, Texas. Send by certified mail with return receipt so you have proof of filing and delivery.

9. Keep a copy permanently. The IRS does not issue a confirmation of receipt for 83(b) elections. Your proof of filing is your certified mail receipt and return receipt card. Keep copies of the election letter and mailing confirmation in your permanent records — you may need them years later when you sell your shares.

10. Provide a copy to your company. The company should keep a copy of your election in its corporate records.

30-day deadline is absolute: The IRS has been clear that late Section 83(b) elections are not accepted, regardless of the reason for the delay. Not knowing about the requirement is not a valid excuse. If you receive vesting equity in a US entity, address the 83(b) question on day one — before the paperwork is signed if possible.

7. Beneficial Ownership Information (BOI) Reporting - The Full Process (for Foreigners Owning US Companies)

The Corporate Transparency Act (CTA) originally created a new federal reporting obligation that required most US entities to disclose their beneficial owners to the Financial Crimes Enforcement Network (FinCEN). Following FinCEN’s interim final rule issued in March 2025, all US-formed entities (and their beneficial owners, including non-US persons) are now fully exempt.

Who must file

All entities formed in the United States, including LLCs, corporations, and similar entities typically used by non-US founders, are now exempt from BOI reporting. There is no filing obligation regardless of ownership percentage or control, even for a single-member LLC 100% owned and controlled by a foreign founder.

Litigation caveat: BOI reporting requirements have been subject to significant legal challenges since their introduction, with court orders at various points temporarily blocking or pausing enforcement. The status shifted multiple times and ultimately led to FinCEN’s March 2025 interim final rule that exempts all domestically formed entities and their beneficial owners (including foreign ones). Before relying on any guidance about current BOI filing obligations, including the guidance in this section, confirm the current enforcement status with a US advisor or by checking FinCEN’s website (fincen.gov/boi) directly.

8. Operating Agreement Deep Dive - What to Include and Why

The operating agreement is your LLC's constitutional document. For a single-member LLC, it is simpler than for a multi-member entity, but in both cases, it needs to be comprehensive enough to serve its purpose: governing the relationship between the LLC and its members, establishing the authority of the manager, and providing the procedural framework for major decisions.

Essential provisions for all LLCs

Regardless of whether your LLC has one member or many, your operating agreement should cover the following:

– Identification of the entity: Full legal name, state of formation, date of formation, and registered agent details.

– Member details: Names, addresses, and membership interest (ownership percentage) of all members. For a single-member LLC, this confirms you as the 100% owner.

– Management structure: Whether the LLC is member-managed (members make day-to-day decisions) or manager-managed (a designated manager, who may or may not be a member, makes decisions). For a single-member LLC, the member is typically also the sole manager. For multi-member LLCs, the management structure significantly affects governance.

– Capital contributions: What each member has contributed or is required to contribute, cash, property, services, or a combination. This establishes the starting point for each member's economic rights in the entity.

– Profit and loss allocation: How profits and losses are allocated among members. For a single-member LLC this is simple, 100% to the sole member. For multi-member LLCs, this must address both ordinary allocations and special allocations where members' economic interests do not follow their ownership percentages.

– Distributions: When and how distributions are made, who has authority to approve them, and whether there is a minimum distribution requirement.

– Decision-making and voting: What decisions require member approval, at what threshold (simple majority, supermajority, or unanimity), and what the manager can decide unilaterally.

– Transfer restrictions: Rules governing the transfer of membership interests, typically prohibiting transfers without member approval, establishing right of first refusal, and addressing what happens on death, disability, or withdrawal of a member.

– Dissolution: The process for dissolving the LLC, distributing remaining assets, and winding up affairs.

Additional provisions for multi-member LLCs

Multi-member LLCs require additional provisions that address the more complex dynamics of shared ownership:

– Deadlock provisions: What happens when members cannot agree on a major decision, mediation, arbitration, or a buy-sell mechanism.

– Buy-sell provisions: The mechanism by which one member can buy out another, triggered by departure, death, disability, or irreconcilable disagreement. Common structures include shotgun clauses (one party names a price, the other chooses to buy or sell at that price) and right of first refusal (departing member must offer their interest to remaining members before selling to a third party).

– Non-compete and non-solicitation: Restrictions on members competing with the LLC or soliciting its clients or employees during and after their membership. Enforceability varies significantly by state.

– Anti-dilution protections: Whether existing members have pre-emptive rights to maintain their percentage ownership when new members are admitted.

The single-member operating agreement and corporate veil protection

Many founders question whether a single-member LLC really needs an operating agreement if there is no one else to govern the relationship with. The answer is yes and for several important reasons.

First, banks request it. Mercury, Relay, Brex, and virtually all traditional banks require an operating agreement as part of the account-opening process for an LLC. Without one, you cannot open a bank account.

Second, it establishes the separation between you and the entity. One of the primary benefits of an LLC is limited liability, the principle that your personal assets are protected from the LLC's debts and obligations. Courts can pierce the corporate veil and hold members personally liable when the LLC and the member are treated as interchangeable, when personal and business finances are commingled, when the LLC has no governance documents, and when the LLC is not treated as a separate entity in practice. An operating agreement, properly executed and followed, is part of the evidence that the LLC is a genuine separate entity.

Third, clients and counterparties may request it as part of due diligence, particularly for larger contracts where they want to verify who has authority to sign on behalf of the entity.

9. Maintaining Your Corporate Records

Formation is not a one-time event, it creates ongoing obligations to maintain and organise your corporate records. A company with poor or missing records faces problems at every subsequent stage: banking, fundraising, legal disputes, audit, and exit. This section sets out what records you need to maintain and for how long.

For LLCs

– Certificate of Formation (or Certificate of Organisation) — keep permanently

– Executed Operating Agreement and any amendments — keep permanently

– EIN confirmation letter (CP 575) — keep permanently

– All annual reports filed with the state — keep permanently

– Bank account opening documents — keep for at least 7 years

– BOI filings and any updates — keep permanently while entity is active

– Resolutions or written consents for major decisions — keep permanently

– Copies of all contracts signed by the LLC — keep for at least 7 years after expiry

– Financial records, bank statements, invoices — keep for at least 7 years (IRS statute of limitations is generally 3 years, but 6 years for substantial understatement of income, and unlimited for fraud)

For C-Corps

All of the above, plus:

– Certificate of Incorporation — keep permanently

– Bylaws and all amendments — keep permanently

– All board and shareholder resolutions and written consents — keep permanently

– Stock ledger and all stock issuance, transfer, and cancellation records — keep permanently

– Stock certificates or evidence of book-entry shares — keep permanently

– All executed stock purchase agreements, option grant notices, and equity plan documents — keep permanently

– Section 83(b) elections and proof of filing — keep permanently

– All investor agreements (SAFEs, convertible notes, preferred stock purchase agreements) — keep permanently

Digital record-keeping: All of these documents should exist in signed, executed form, not just as drafts or template files. Store them in a secure, organised digital system with regular backups. Many founders use a corporate records folder in a cloud storage service (Google Drive, Dropbox) alongside a physical or digital records book. The exact system matters less than the discipline of keeping it current.

10. Common Formation Mistakes — The Full List

Having covered the formation process in detail, it is worth cataloguing the specific mistakes that cause the most downstream problems for non-US founders. These are not hypothetical, as they are the issues that arise repeatedly when founders come to clean up their structure later.

– Not checking name availability before committing: Filing an Articles of Organization only to find the name is unavailable or confusingly similar to an existing entity wastes time and filing fees. Check availability first.

– Using a PO box or forwarding address as the principal business address: Some state filings and most bank applications require a genuine street address. A PO box creates friction at multiple downstream steps.

– Getting the EIN before the entity is formed: The EIN is issued to a specific entity that must already exist. Applying for an EIN before the state has processed your Articles of Organization can result in the EIN being issued to a nonexistent entity. Always form first, then apply for the EIN.

– Missing the Section 83(b) election: The most consequential and irreversible mistake on this list. If your equity is subject to vesting, file the 83(b) election within 30 days of grant with no exceptions.

– Not executing the operating agreement before opening a bank account: Banks ask for it. Having a signed, dated operating agreement before you apply saves a round-trip delay in account opening.

– Failing to register in operating states: Forming in Delaware or Wyoming and then operating in California, New York, or Texas without registering as a foreign entity creates penalties, back fees, and potential inability to enforce contracts in those states.

– Treating the registered agent as your only compliance obligation: Having a registered agent does not mean your compliance obligations are handled. The registered agent receives mail on your behalf, the compliance filings, tax returns, and annual reports are your responsibility.

– Ignoring the BOI filing: The penalties for wilful non-compliance are significant. Even founders who are unaware of the requirement are expected to meet it. Add it to your formation checklist.

– Using a personal address as the LLC's business address with a US bank: Some banks accept foreign personal addresses; others do not. Check in advance whether your bank requires a US business address and arrange a virtual office if so.

– Not telling your home country accountant: Forming a US entity changes your personal tax position in your home country. Your home country accountant cannot advise you correctly without knowing the US entity exists.

Before you move to Part 4

Part 4 covers US banking, the step that many founders find harder than forming the entity itself. It covers which banks are accessible to foreign-owned entities, what the application process involves, what to do if you are rejected, and how payment processors and fintech alternatives fit into your banking strategy.

Before you move on, confirm the following from this Part are complete or in progress:

– Entity formed and Certificate of Formation or Incorporation received

– Registered agent engaged and confirmed

– Operating agreement (LLC) or bylaws and initial resolutions (C-Corp) executed and filed in your records

– EIN obtained and recorded securely

– Section 83(b) election filed if you received vesting equity, within 30 days of grant

– BOI report filed with FinCEN (or status confirmed with your advisor)

– Foreign state registrations filed if you have US operating presence outside your formation state

– Home country accountant notified of the new US entity

Antravia Advisory: We help non-US founders navigate formation correctly, from entity selection through to EIN applications, operating agreements, and coordination with home country advisors. If you want to make sure this is done right, get in touch.

Continue to Part 4: US Banking — The Hardest Part Nobody Warns You About →

About Antravia Advisory

Antravia Advisory is a US-based tax and accounting advisory firm headquartered in Winter Park, Florida, operating nationally and internationally.

We advise international businesses entering the United States and complex US companies operating across multiple states, entities, and revenue structures. Our work spans advanced tax strategy, multi-state sales tax oversight, cross-border structuring, and high-level accounting architecture for e-commerce brands, subscription and SaaS businesses, platform-based models, and multi-entity groups.

We work with founders and leadership teams who require technical precision, structural clarity, and financial frameworks built for scale, capital events, and long-term resilience.

The Non-US Founder’s Complete Guide to Running a US Business

Part 1 — Before You Start

Part 2 — Choosing Your US Entity

Part 3 — Formation

Part 4 — US Banking

Part 5 — US Federal Tax

Part 6 — US State Tax

Part 7 — Paying Yourself

Part 8 — Accounting and Bookkeeping

Part 9 — Annual Compliance Calendar

Part 10 — Hiring in the US

Part 11 — Intellectual Property and Contracts

Part 12 — Your Home Country Obligations

Part 13 — Applied Business Types

Part 14 — Exiting, Winding Down, or Restructuring

Disclaimer:

Content published by Antravia is provided for informational purposes only and reflects research, industry analysis, and our professional perspective. It does not constitute legal, tax, or accounting advice. Regulations vary by jurisdiction, and individual circumstances differ. Readers should seek advice from a qualified professional before making decisions that could affect their business.

See also our Disclaimer page

Antravia Advisory

Accounting built for complexity

Not legal advice, always verify with your Accountant

Email:

Contact us:

© 2025. All rights reserved. | Disclaimer | Privacy Policy | Terms of Use |

contact@antravia.com

Antravia LLC

941 W Morse Blvd suite 100

Winter Park

Florida

32789