Part 6: US State Tax

The Non-US Founder's Complete Guide to Running a US Business - Part 6 explains how U.S. state tax works for non-U.S. founders, including nexus rules, state income tax, sales tax after the Wayfair decision, SaaS taxability, franchise taxes, payroll tax across states, and how to manage multi-state compliance.

THE NON-US FOUNDER'S COMPLETE GUIDE TO RUNNING A US BUSINESS

3/9/202620 min read

Federal tax gets most of the attention in guides for non-US founders. State tax gets very little. This is a significant gap, because state tax obligations are separate from federal obligations, apply on top of federal tax, and in some cases are more immediately consequential for an early-stage business than anything the IRS imposes.

There are 50 states, each with its own tax laws, its own filing requirements, its own definitions of what creates a taxable presence, and its own enforcement priorities. No founder needs to become an expert in all 50 states. But every founder needs to understand the states that are actually relevant to their business, what the most common state tax traps are, and how to build a compliance structure that keeps state obligations from becoming a crisis.

This part covers state income tax, the sales tax system and the Wayfair economic nexus ruling, franchise taxes and annual fees, payroll tax in multi-state hiring situations, and a state-by-state compliance calendar. It also covers the topic that causes the most problems for non-US founders who sell into the US remotely: sales tax on digital products and SaaS.

See also our USSales.tax page.

1. Why State Tax Is a Separate and Often Overlooked Obligation

The US federal tax system and each state's tax system operate independently. Federal tax compliance does not satisfy state tax obligations, and state tax compliance does not satisfy federal obligations. A founder who files a perfect federal return but ignores California's franchise minimum tax, or who collects revenue from Washington state customers without registering for Washington's Business and Occupation Tax, has two separate compliance problems regardless of how well they handled the federal side.

For non-US founders, state tax is particularly easy to overlook because the formation guides and legal services that helped them set up their entity typically focus on the federal layer. A Wyoming LLC formation service tells you how to form the entity and get the EIN. It does not tell you that if your first paying customer is in California and pays you more than $500,000, you may have California sales tax obligations, or that if you hire a remote employee in New York, you now have New York payroll tax and corporate nexus obligations.

Nexus: the concept that drives state tax obligations

The threshold question in every state tax analysis is whether your business has nexus in a state. Nexus is a sufficient connection between your business and a state to justify that state imposing its tax laws on your business. Without nexus, a state cannot require you to collect sales tax, file an income tax return, or pay franchise taxes.

The traditional standard for nexus was physical presence: an office, employees, inventory, or a regular business presence in the state. The Supreme Court's 2018 decision in South Dakota v. Wayfair expanded this significantly for sales tax purposes, allowing states to impose sales tax collection obligations based on economic activity alone, without any physical presence. The Wayfair ruling changed the sales tax landscape fundamentally and is covered in detail in Section 3 of this part.

For income tax purposes, physical presence nexus still governs in most states, though some states have adopted economic nexus standards for income tax as well. The practical consequence: having a US entity incorporated in Delaware or Wyoming does not mean your only state tax obligation is in Delaware or Wyoming. Every state where you have employees, maintain an office, store inventory, or exceed the economic nexus threshold for that state's tax becomes a state where you have compliance obligations.

2. State Income Tax: Which States Have It and Which Do Not

State income taxes are levied separately from federal income tax. Not all states impose an income tax; those that do apply their own rates, their own definitions of taxable income, and their own rules for apportioning income among states when a business operates in multiple states.

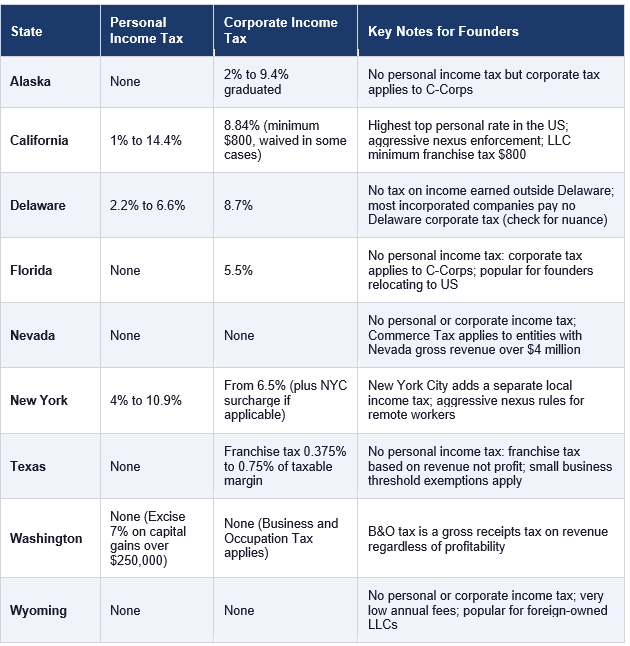

States with no income tax

Nine states currently impose no personal income tax: Alaska, Florida, Nevada, New Hampshire (which taxes only interest and dividends, with that tax being phased out), South Dakota, Tennessee (which similarly taxed only investment income, now eliminated), Texas, Washington (which taxes capital gains above a threshold but not ordinary income), and Wyoming. For non-US founders who establish a US physical presence and become US tax residents, choosing to locate in one of these states eliminates the state personal income tax layer entirely.

Of these, Florida, Nevada, Texas, and Wyoming are the most commonly chosen by non-US founders who are building a US presence. Florida and Texas offer large markets and significant business infrastructure alongside zero personal income tax. Nevada and Wyoming offer low overall tax burdens and are commonly used as formation states for entities whose owners have no specific state operating preference.

States with the highest income tax rates

California has the highest top marginal personal income tax rate in the United States, currently 13.3% on income over approximately $1 million. For a non-US founder who becomes a California resident or whose business generates California-source income, this rate applies on top of the federal rate, creating an effective combined marginal rate that can exceed 50% for high earners. California also has an 8.84% corporate income tax rate and a minimum franchise tax of $800 per year for LLCs and corporations.

New York has a top personal income tax rate of 10.9%, with an additional New York City income tax of up to 3.876% for city residents. New Jersey reaches 10.75% at the top. Oregon reaches 9.9%. These rates are relevant for any founder who physically relocates to one of these states or whose business generates income sourced in these states.

State income tax apportionment

When a business operates in multiple states, it does not pay income tax on its full income to every state where it operates. Instead, it apportions its income among states using a formula that reflects the share of its business activity in each state. Most states use a three-factor apportionment formula based on sales, payroll, and property, though the weighting of these factors varies. An increasing number of states now use a single-sales-factor formula, meaning only the share of sales in the state determines the state's slice of taxable income.

For a non-US founder selling primarily to US customers from a single-state US entity, apportionment is straightforward: the income is apportioned to the state where the sales activity occurs, or where the customer is located, depending on the state's rules. For a founder with employees in multiple states, customers across the country, and physical operations in more than one state, apportionment becomes a more complex annual calculation that requires careful record-keeping of where revenue is sourced and where activities occur.

State income tax by state: quick reference

3. Sales Tax: The Biggest Compliance Trap for Non-US Founders

Sales tax is the single most commonly overlooked and most frequently problematic state tax obligation for non-US founders selling into the US market. It is not an income tax. It is a transaction tax collected from customers at the point of sale and remitted to the state by the seller. The seller acts as an agent of the state for collection purposes.

The complexity of US sales tax is genuinely unusual by global standards. Unlike the VAT systems used in most of the world, which are administered at the federal level with a single rate and consistent rules, US sales tax is administered at the state level, with 45 states plus the District of Columbia imposing it at varying rates, different product taxability rules, different filing frequencies, and different exemption structures. Below the state level, counties, cities, and special districts add their own rates. The total number of distinct sales tax jurisdictions in the United States exceeds 12,000.

The Wayfair ruling: economic nexus changes everything

Before June 2018, the prevailing standard for sales tax nexus was physical presence. A business without a physical presence in a state, meaning no employees, no office, no inventory, and no agents operating there, was not required to collect that state's sales tax, even if it had substantial sales to customers in that state. This was the rule established by the Supreme Court in Quill Corp. v. North Dakota (1992).

The Supreme Court overruled Quill in South Dakota v. Wayfair, Inc. (2018), holding that states can impose sales tax collection obligations on out-of-state sellers based on economic activity alone, without any physical presence. South Dakota's law, which the Court upheld as the model, imposed an obligation on sellers with more than $100,000 in annual sales into South Dakota or more than 200 separate transactions into the state.

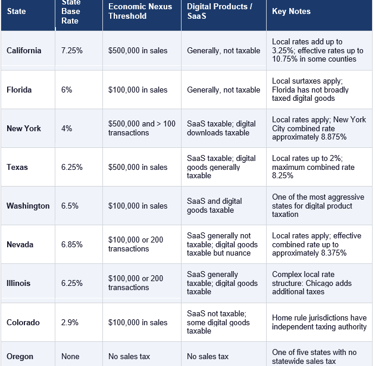

Following Wayfair, every state with a sales tax enacted its own economic nexus threshold. The most common threshold, adopted by the majority of states, is $100,000 in annual sales or 200 transactions into the state. Some states set higher thresholds: California at $500,000, New York at $500,000 and 100 transactions. A handful of states set lower thresholds or have unique variations.

This affects remote sellers directly: A non-US founder selling a software product, a digital subscription, or physical goods to US customers does not need a US office, US employees, or any US physical presence to have sales tax obligations in multiple states. Crossing the economic nexus threshold in any state creates a registration and collection obligation in that state, regardless of where the seller is physically located.

What is subject to sales tax

Physical goods are the traditional subject of sales tax, and most tangible personal property is taxable in most states unless a specific exemption applies. However, the taxability of digital products and services varies enormously from state to state, and this is where non-US founders selling SaaS, digital subscriptions, or downloadable content face the most uncertainty.

SaaS and software

Software as a Service is taxable in approximately half of US states. States that tax SaaS include Texas, New York, Washington, Illinois, Pennsylvania, and others. States that do not tax SaaS include California (which does not tax SaaS if it is true remotely accessed software, though the rules have been contested), Florida, and others. The analysis turns on how the state categorizes the product: is it a sale of software, a service, or access to a service? The same product can be taxable in one state and exempt in a neighboring state.

Digital downloads

Downloadable software, e-books, digital music, and similar digital products are taxable in most states that tax digital goods. However, the rules are not uniform: some states tax only certain categories of digital goods, others have broad definitions that sweep in most downloadable content, and some states are silent on digital goods in their statutes, creating uncertainty about whether the silence means exempt or taxable.

Professional and consulting services

Most states do not impose sales tax on professional services such as legal, accounting, management consulting, or software development services. However, several states, including Hawaii, New Mexico, South Dakota, and West Virginia, tax most services. Texas taxes data processing services. New York taxes certain services to tangible personal property. Any founder selling services into multiple states should confirm the taxability of their specific service type in each state where they have economic nexus.

The registration, collection, and remittance process

Once you have economic nexus in a state, the compliance process involves three steps: registering with the state's Department of Revenue (or equivalent agency) for a sales tax permit, collecting the applicable sales tax rate from customers at the point of sale, and filing sales tax returns and remitting the collected tax on the schedule the state requires.

Registration is done through each state's online portal. Most states issue a sales tax permit within a few days of application. Some states require a deposit or bond for new registrants. The registration process itself is not complicated, but it triggers ongoing filing obligations that must be maintained.

Collection requires knowing the correct rate for each transaction. In states with local sales tax rates, the applicable rate depends on where the buyer is located, not where the seller is located. A sale to a customer in a Chicago suburb may have a different combined rate than a sale to a customer in downtown Chicago. Sales tax automation software such as TaxJar, Avalara, or Vertex handles this calculation automatically for most e-commerce and SaaS platforms by integrating with your billing system.

Filing frequency is determined by the state based on your transaction volume. High-volume sellers typically file monthly. Medium-volume sellers file quarterly. Lower-volume sellers may be permitted to file annually. The state will notify you of your assigned filing frequency when you register, and it may change your frequency as your volume grows.

Managing multi-state sales tax compliance

The practical reality for a non-US founder selling to US customers across multiple states is that manual management of sales tax compliance does not scale. A founder selling a SaaS product with customers in 30 states faces 30 separate filing obligations at different frequencies, with different rates, different rules about what is taxable, and different due dates. Attempting to manage this manually using spreadsheets creates errors, missed filings, and audit exposure.

The standard approach for founders at this scale is to use a sales tax automation platform. TaxJar automates collection rate calculation, filing, and remittance and integrates with Stripe, Shopify, WooCommerce, and most common e-commerce and billing platforms. Avalara is a more enterprise-oriented platform with deeper integration options and a broader range of tax types. Both platforms handle the Wayfair compliance burden by automatically monitoring your nexus thresholds in each state, alerting you when you cross into a new state's obligation, and handling registration and ongoing filing.

Antravia Advisory note: Sales tax automation is one of the highest-value investments a non-US founder selling digitally into the US can make. The cost of a TaxJar or Avalara subscription is modest compared to the cost of a sales tax audit, back taxes, interest, and penalties in even a single state. If you are currently handling US sales tax manually or not at all, addressing this should be near the top of your compliance priority list.

States with no sales tax

Five states impose no statewide sales tax: Alaska, Delaware, Montana, New Hampshire, and Oregon. Of these, Delaware and Wyoming are the most commonly chosen formation states, which leads some founders to incorrectly assume that forming in a no-sales-tax state exempts them from sales tax obligations in other states. It does not. Sales tax obligations are determined by where your customers are located, not where your entity is formed.

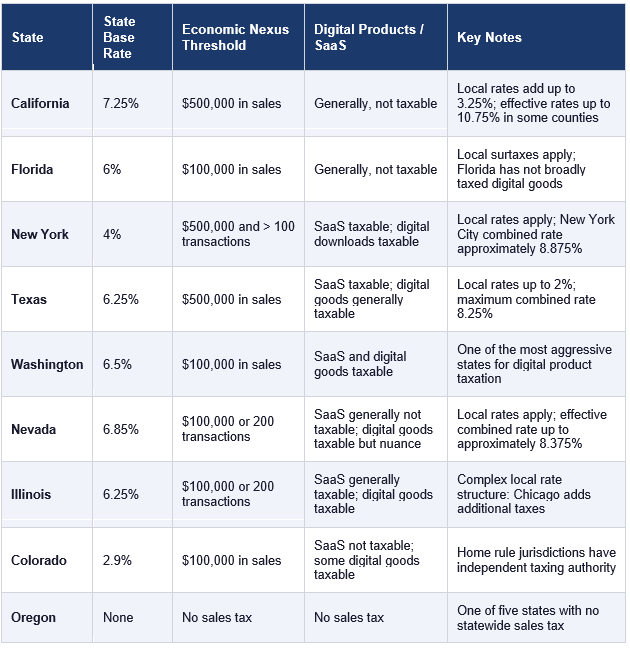

4. Sales Tax by State: Quick Reference

The following table covers the states most likely to be relevant for non-US founders selling digital products, SaaS, or physical goods to US customers. Rates shown are state base rates; local rates are added on top and vary by jurisdiction. Economic nexus thresholds and digital product taxability rules change frequently; confirm current rules with a sales tax professional or automation platform before relying on this table.

5. Franchise Taxes and Annual Fees

Franchise taxes are state-level taxes imposed on the privilege of doing business in the state as a corporation or LLC, separate from income tax. They exist even in states that have no income tax, and they apply even to entities that have no revenue. Failure to pay franchise taxes and file annual reports results in the entity losing good standing, which can eventually lead to administrative dissolution and loss of the entity's right to conduct business in the state.

Delaware franchise tax

Delaware's franchise tax is the most commonly encountered by non-US founders because Delaware is the most popular formation state. For LLCs, Delaware charges a flat $300 annual franchise tax plus a $50 registered agent fee. For corporations, the franchise tax calculation is more complex and depends on the method used.

Delaware provides two methods for calculating corporate franchise tax. The Authorized Shares Method calculates the tax based on the number of shares authorized in the Certificate of Incorporation. For a company with 10,000,000 authorized shares, this method can produce a franchise tax bill of several thousand dollars, sometimes significantly more depending on the exact share count. The Assumed Par Value Capital Method calculates the tax based on the relationship between authorized shares and paid-in capital. For an early-stage company with a large authorized share count but modest paid-in capital, this method typically produces a tax at or near the minimum of $400 per year.

Delaware bills corporations using the Authorized Shares Method by default. You must request recalculation using the Assumed Par Value Capital Method and pay the lower result. The difference between the two methods for a typical early-stage startup can be thousands of dollars per year. Always calculate your Delaware franchise tax under both methods and pay the lower amount.

California minimum franchise tax

California imposes a minimum franchise tax of $800 per year on every LLC, corporation, and partnership registered to do business in California, regardless of whether the entity is profitable, regardless of whether it has any California revenue, and regardless of whether it is active. This $800 applies in the first year of registration and every year thereafter until the entity formally withdraws from California registration.

For non-US founders who have registered a foreign entity (formed in Delaware or Wyoming) to do business in California because they have a California employee or California operations, this $800 minimum applies from day one. If you later cease California operations and want to eliminate the obligation, you must file a formal withdrawal from California registration, which requires a Certificate of Withdrawal filed with the California Secretary of State.

Wyoming annual report fee

Wyoming charges an annual report fee based on the value of the entity's assets located in Wyoming. For most non-US-founded LLCs with no Wyoming assets, this results in the minimum fee of approximately $60 per year. This makes Wyoming one of the lowest-cost states for annual maintenance, which is a primary reason it is popular for foreign-owned LLCs with no US physical operations.

Texas franchise tax

Texas does not impose a personal income tax or a traditional corporate income tax, but it does impose a franchise tax on most business entities, including LLCs. The Texas franchise tax is based on a business's taxable margin, which is calculated as total revenue minus the greater of cost of goods sold, compensation, or 30% of total revenue, with the result capped at 70% of total revenue. The tax rate is 0.375% for wholesale and retail businesses and 0.75% for all other businesses.

Texas provides an exemption for businesses with total revenue at or below the No Tax Due threshold, which has been adjusted over time and should be confirmed with current Texas Comptroller guidance. Most early-stage founders with Texas nexus but modest revenue will qualify for this exemption and owe no Texas franchise tax in early years, though the filing obligation (or a no-tax-due report) still applies.

6. Payroll Tax When You Hire Across Multiple States

Hiring US-based employees creates state tax obligations in every state where those employees are located. This is one of the most significant ways that a US entity's state tax footprint expands as the business grows. Each state where you have an employee requires separate registration with the state's tax authority, separate payroll tax withholding and remittance, and separate unemployment insurance contributions.

State income tax withholding

Every state with a personal income tax requires employers to withhold state income tax from employee wages and remit those amounts to the state. As an employer, your obligation is to withhold the correct amount based on each employee's state of residence, remit those amounts on the schedule the state requires (which can be monthly, semi-monthly, or quarterly depending on your payroll size), and file quarterly or annual reconciliation returns.

The complication arises when employees work remotely. An employee who lives in New Jersey but works for a company headquartered in New York creates a two-state withholding situation. New York applies a "convenience of the employer" rule that taxes income of employees who work from home for their own convenience (rather than because the employer requires it) as New York-source income, even if the employee is physically in New Jersey. Pennsylvania applies similar rules. These rules create unexpected tax obligations for employees and employers alike.

State unemployment insurance

State unemployment insurance (SUI) is a payroll tax paid entirely by the employer, not the employee. Every state with employees requires SUI registration and quarterly payments. The SUI rate for a new employer varies by state (typically between 1% and 4%) and applies to each employee's wages up to the state's taxable wage base, which varies from approximately $7,000 in some states to over $50,000 in others. As an employer's history in the state develops, the SUI rate is experience-rated: employers with more unemployment claims from former employees pay higher rates.

Multi-state nexus from remote employees

Hiring a single employee in a state creates income tax nexus in that state for the entity, not just payroll tax obligations. A C-Corp with a remote employee in California is doing business in California and must register to do business there, pay California's minimum franchise tax, and potentially file California corporate income tax returns apportioning income to California. The same applies in New York, Illinois, and other states with corporate income taxes.

This is not a reason to avoid hiring remote employees. It is a reason to understand the full state tax consequence of each hire and account for it in your compliance budget. A single California employee can add the $800 California minimum franchise tax, California payroll tax registration and filings, and potential California income tax apportionment to your annual compliance obligations. These costs are manageable if anticipated and chaotic if discovered retroactively.

7. Good Standing: What It Is and Why It Matters

Every state requires entities registered to do business there to maintain good standing by filing required annual reports and paying required fees and taxes on time. An entity that fails to file its annual report or pay its franchise tax loses good standing and is eventually subject to administrative dissolution or revocation of its authority to do business in the state.

The consequences of losing good standing are more serious than they might appear. An entity that is not in good standing may be unable to bring a lawsuit in that state's courts to enforce a contract. It may be unable to obtain a certificate of good standing, which is typically required by lenders, investors, and counterparties in M&A transactions. It may face personal liability for the officers and directors who allowed the entity to fall out of good standing while continuing to conduct business. And reinstating good standing after it has been lost typically requires paying all overdue fees, taxes, and penalties plus a reinstatement fee, which can be expensive in states like California.

Maintaining good standing is simple if you build it into your annual compliance calendar: know which states require annual reports, know the due dates, and make sure reports are filed and fees paid on time each year. Your registered agent in each state should remind you of upcoming annual report deadlines, but the responsibility for filing rests with you as the entity owner, not with the registered agent.

8. Annual Compliance Calendar: Federal and State Combined

The following calendar consolidates federal and state-level compliance deadlines into a single reference. Dates shown assume a calendar tax year. All state-level deadlines vary by state; the dates shown are the most common patterns. Always confirm current deadlines with a US tax advisor or directly with the relevant state agency.

January 15

Fourth quarter estimated tax payment due for the prior tax year. This applies to individuals with U.S. estimated tax obligations, including many nonresident founders filing Form 1040-NR.

January 31

Forms W-2 must be furnished to employees, and most Forms 1099 such as Form 1099-NEC must be furnished to recipients. This applies to any U.S. entity that paid employees or independent contractors during the prior year.

January 31

Forms W-2 must also be filed with the Social Security Administration. Form 1099-NEC must be filed with the IRS by this date.

February 28 (paper filing) / March 31 (electronic filing)

Many other information returns such as Form 1099-MISC must be filed with the IRS by these deadlines depending on whether the filing is paper or electronic.

March 15

Form 1065 partnership return due. This applies to partnerships and multi-member LLCs taxed as partnerships for calendar-year entities.

April 15

Form 1120 corporate income tax return due for calendar-year C-corporations.

April 15

Form 5472 with a pro forma Form 1120 due for foreign-owned single-member LLCs that are treated as disregarded entities.

April 15

Form 1040-NR due for many nonresident individuals who have U.S. income effectively connected with a U.S. trade or business. However, some nonresident filers without U.S. wage withholding may instead have a June 15 filing deadline.

April 15

First estimated tax payment for the current year due for individuals with U.S. estimated tax obligations.

June 15

Second estimated tax payment due for individuals with U.S. estimated tax obligations.

September 15

Third estimated tax payment due for individuals with U.S. estimated tax obligations.

September 15

Extended deadline for Form 1065 partnership returns if an extension was filed.

October 15

Extended deadline for Form 1120 corporate returns if an extension was filed.

October 15

Extended deadline for Form 5472 with pro forma Form 1120 for foreign-owned single-member LLCs if an extension was filed.

October 15

Extended deadline for Form 1040-NR if the taxpayer filed for an extension.

Varies by state

State annual report filings. These apply to entities registered in states that require annual reports or franchise tax filings.

Ongoing throughout the year

Sales tax returns must be filed monthly, quarterly, or annually depending on the state and the filing frequency assigned when the business registers for sales tax.

Ongoing throughout the year

Payroll tax deposits must be made either monthly or semi-weekly depending on the employer’s payroll tax liability. This applies to entities that employ U.S. workers.

Extension tip: Extensions of time to file do not extend the time to pay. If you file for an extension on your federal or state income tax return, you must still pay your estimated tax liability by the original due date to avoid interest and underpayment penalties. The extension only gives you more time to complete and submit the return itself.

9. What Triggers a State Tax Audit

State tax audits are initiated by state revenue agencies independently of IRS activity, though the two sometimes coordinate, particularly when a federal audit adjustment has state tax implications. Understanding what draws state scrutiny helps you build compliance practices that reduce audit risk.

Sales tax: the primary trigger

Sales tax audits are the most common type of state tax audit faced by non-US founders selling to US customers. The triggers include inconsistency between reported sales figures and income reported on other returns, registration in a state without filing returns, crossing the economic nexus threshold without registering, and information received from other states (states share nexus information under the Streamlined Sales and Use Tax Agreement).

Payroll tax discrepancies

States compare payroll tax filings with W-2 and 1099 reports filed with the IRS and with the Social Security Administration. Discrepancies between reported wages and payroll tax deposits are a common trigger for payroll tax audits. Misclassification of employees as independent contractors is also an active enforcement priority in California, New York, and other states.

Income apportionment inconsistencies

When an entity files income tax returns in multiple states, the apportionment percentages across those states should total 100%. A company that apportions 40% of its income to California, 35% to New York, and 20% to Texas has accounted for only 95% of its income. The missing 5% may represent income that should have been apportioned to other states but was not. State auditors look for these gaps, which can indicate either errors in the apportionment calculation or income that was not reported in any state.

Federal audit adjustments

When the IRS audits a federal return and makes an adjustment that increases taxable income, most states require the taxpayer to report that adjustment and pay any additional state tax due within a specified period, typically 60 to 90 days after the federal adjustment is final. Failure to report federal adjustments to the relevant states is itself an audit trigger and a basis for additional penalties.

Before You Move to Part 7

Part 7 covers how to pay yourself as a non-US founder: the four methods available, the tax treatment of each in the US, the interaction with your home country tax, and the practical mechanics of salary, distributions, dividends, and management fees. It also covers FICA, totalization agreements, and the timing considerations that affect both your US and home country position.

Before you move on, confirm the following from this part:

• You know which states you have nexus in, based on where your employees are located, where you have physical operations, and where your customers are located

• You have assessed whether you have crossed the economic nexus threshold in any state for sales tax purposes

• You have registered for sales tax in every state where you have economic nexus and are collecting and remitting correctly, or you are using a sales tax automation platform to manage this

• You are paying Delaware, Wyoming, California, or other applicable state franchise taxes and annual fees on time each year

• You have registered for payroll tax in every state where you have employees

• Your entity is in good standing in every state where it is registered

Antravia Advisory: State tax is one of the areas where the gap between what founders think they owe and what they actually owe tends to be largest. If you have been selling to US customers for more than a year and have not formally assessed your sales tax exposure, or if you have hired US employees without reviewing the state registration consequences, now is the time to address it. We can help you work through the exposure and build a compliant structure going forward.

Continue to Part 7: Paying Yourself as a Non-US Founder

About Antravia Advisory

Antravia Advisory is a US-based tax and accounting advisory firm headquartered in Winter Park, Florida, operating nationally and internationally.

We advise international businesses entering the United States and complex US companies operating across multiple states, entities, and revenue structures. Our work spans advanced tax strategy, multi-state sales tax oversight, cross-border structuring, and high-level accounting architecture for e-commerce brands, subscription and SaaS businesses, platform-based models, and multi-entity groups.

We work with founders and leadership teams who require technical precision, structural clarity, and financial frameworks built for scale, capital events, and long-term resilience.

Disclaimer:

Content published by Antravia is provided for informational purposes only and reflects research, industry analysis, and our professional perspective. It does not constitute legal, tax, or accounting advice. Regulations vary by jurisdiction, and individual circumstances differ. Readers should seek advice from a qualified professional before making decisions that could affect their business.

See also our Disclaimer page

Antravia Advisory

Accounting built for complexity

Not legal advice, always verify with your Accountant

Email:

Contact us:

© 2025. All rights reserved. | Disclaimer | Privacy Policy | Terms of Use |

contact@antravia.com

Antravia LLC

Winter Park

Florida

32789