Part 7: Paying Yourself as a Non-US Founder

The Non-US Founder's Complete Guide to Running a US Business - Part 7 explains how non-U.S. founders can legally pay themselves from a U.S. business, covering salaries, LLC distributions, C-Corp dividends, management fees, FICA rules, totalization agreements, and the tax impact in both the U.S. and the founder’s home country.

THE NON-US FOUNDER'S COMPLETE GUIDE TO RUNNING A US BUSINESS

3/15/202622 min read

How you take money out of your US business is one of the most consequential decisions you will make as a non-US founder, and one of the least discussed in generic guides. The mechanics of extraction affect your US tax liability, your home country tax liability, your FICA obligations, your entity's deductibility, your compliance burden, and in some cases the legal standing of the transaction itself.

There is no single right answer. The optimal method for a Canadian founder running a disregarded LLC is different from what works for an Israeli founder with a Delaware C-Corp and a VC investor, which is again different from what makes sense for a UK founder who has an operating company at home and a US entity that functions primarily as a sales vehicle. This part explains each available method in full, what it costs in the US, what it triggers at home, and when each approach is appropriate.

1. The Four Ways to Take Money Out of Your US Business

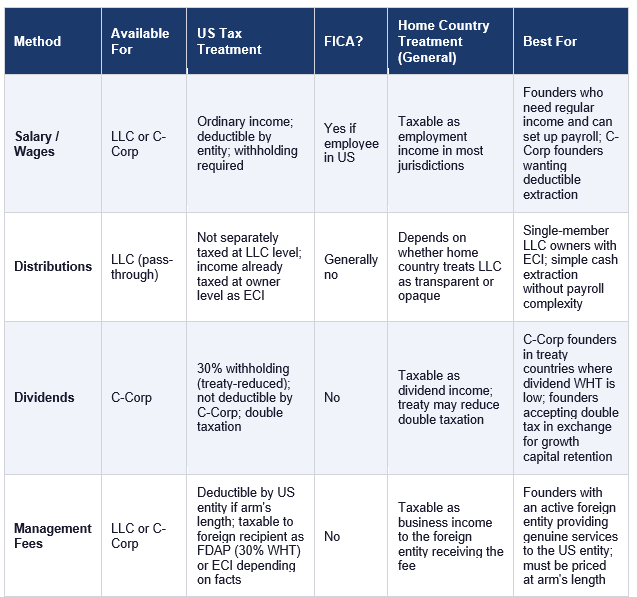

There are four primary mechanisms through which a non-US founder can extract value from a US entity: salary or wages, distributions, dividends, and management fees. Each has a distinct legal structure, a distinct US tax treatment, and a distinct interaction with your home country tax system. Understanding all four before you establish a pattern is important, because changing your extraction method after the fact can be disruptive and sometimes costly.

The table above provides a framework. The sections that follow explain each method in the detail required to make an informed decision for your specific situation.

2. Salary and Wages

Paying yourself a salary from your US entity is the most familiar extraction method and, in many situations, the most straightforward from a compliance perspective. But it carries specific requirements and costs that distinguish it from the other methods.

How it works

A salary is compensation paid to you as an employee of your US entity in exchange for services you perform for that entity. For the US entity, salary payments are a deductible business expense, which reduces the entity's taxable income. For you as the recipient, salary is ordinary income subject to US income tax withholding and, depending on your situation, FICA taxes.

Paying yourself a salary requires the US entity to set up payroll. This means registering with the IRS as an employer, obtaining state employer identification numbers in any state where payroll is processed, establishing a payroll system, withholding federal and state income tax and applicable employment taxes from each paycheck, depositing withheld amounts with the IRS and state agencies on the required schedule, and filing quarterly payroll tax returns (Form 941 at the federal level, plus state equivalents). It also means issuing a W-2 to yourself at the end of each year.

Do non-resident alien founders owe FICA on their salary?

FICA taxes consist of Social Security tax (6.2% each on employer and employee, this changes annually) and Medicare tax (1.45% each on employer and employee, with an additional 0.9% employee-only surtax on wages above $200,000 for single filers). The combined employee and employer FICA cost on wages up to the Social Security wage base is 15.3% of wages.

Whether a non-resident alien founder owes FICA on salary paid by their US entity depends on their visa status and work location. Non-resident aliens working in the United States on certain visa categories may be subject to FICA in the same way as US citizens. Non-resident aliens working entirely outside the United States for a US entity present a more nuanced analysis, as FICA applies to wages for services performed within the United States. If you are physically working from your home country and your employment relationship with the US entity reflects that, FICA may not apply. But this requires careful structuring and documentation to support the position.

The practical reality is that many non-US founders who pay themselves a salary from their US entity while working primarily from abroad do not set up formal US payroll at all, particularly in the early stages. Instead, they take distributions or management fees. Salary is most appropriate when the founder has a genuine employment relationship with the US entity that is reflected in a written employment agreement, performs services primarily for that entity, and is either physically present in the US with the right to work there, or has structured the employment clearly as a non-US arrangement.

The reasonable compensation requirement for C-Corps

For C-Corp founders, the salary paid to the founder-employee has an additional significance: it is the primary mechanism for extracting value from the corporation in a tax-deductible way. C-Corp dividends are not deductible at the corporate level; salary is. This creates an incentive for founder-shareholders to pay themselves high salaries to reduce the corporate tax base.

The IRS monitors this. Compensation paid to shareholder-employees of closely held C-Corps must be reasonable for the services actually performed. If the IRS determines that compensation is excessive, it can recharacterize the excess as a dividend, which eliminates the corporate deduction and subjects the payment to dividend withholding tax at the shareholder level. The standard is what an arm's length employer would pay a non-shareholder employee performing the same services in the same market. Maintaining documentation of the founder's role, comparable market compensation data, and the board's process for setting compensation helps defend the reasonableness of the salary chosen.

3. Distributions from a Single-Member LLC

For a non-US founder who has chosen the single-member LLC structure, distributions are typically the primary method of moving money from the entity to the owner. Understanding exactly how they work from a tax perspective requires revisiting the disregarded entity concept.

How distributions work for a disregarded LLC

A single-member LLC is a disregarded entity for US federal tax purposes. The IRS treats the LLC's income as the owner's income directly, as if the LLC did not exist. This means that when the LLC earns income, the owner is taxed on that income at the time it is earned, not when it is distributed. A distribution from the LLC to the owner is simply a movement of money that the owner has already been taxed on. It does not create a new US tax event.

This is fundamentally different from a C-Corp dividend, which creates a taxable event when it is paid. For the disregarded LLC owner, the tax year in which the income is earned is when the tax obligation arises, regardless of whether a distribution is made. Taking a distribution in the same year the income was earned, in the following year, or not at all does not change the federal income tax due on that income.

When distributions do matter from a US tax perspective

Although distributions from a disregarded LLC do not create a federal income tax event for the owner, they are reportable transactions on Form 5472. Any distribution from the LLC to its foreign owner must be disclosed on Form 5472 as a reportable transaction between the entity and its foreign owner. This is an information reporting obligation, not a tax obligation, but it is one that must be met.

Distributions also matter from a cash management perspective. The owner is liable for tax on the LLC's income in the year it is earned, regardless of distributions. If the LLC earns significant income in a year but retains most of it for reinvestment, the owner may face a personal tax liability without having received the cash to pay it. Planning distributions to coincide with estimated tax payment obligations helps avoid this cash flow mismatch.

How your home country treats LLC distributions

This is where the analysis becomes country-specific and often surprising. As discussed in Part 1 and Part 13, not every country treats a US LLC as a transparent entity. The United Kingdom, for example, treats most US LLCs as opaque for UK tax purposes. This creates a mismatch: the US treats the LLC income as taxable to you when earned, while the UK may not recognize a taxable event until a distribution is made (treating the LLC more like a corporation from which you receive a dividend).

The consequence of this mismatch is that the timing of your UK tax liability on LLC income may differ from your US tax liability. In some cases, this can create double taxation: you pay US tax on the income when earned, and UK tax on the same income when distributed, without a clean credit mechanism to offset one against the other. Getting clarity on your home country's treatment of your LLC structure before you establish a distribution pattern is essential. Part 13 covers this by jurisdiction.

4. Dividends from a C-Corporation

If your US entity is a C-Corp, the primary non-salary method of extracting value is a dividend. A dividend is a distribution of corporate profits to shareholders, declared by the board of directors. It is not deductible by the corporation and is taxed in the hands of the recipient.

US withholding on dividends

Dividends paid by a US C-Corp to a non-resident alien shareholder are FDAP income and are subject to US withholding tax at the default rate of 30% on the gross amount. The corporation withholds the tax before paying the dividend and remits it to the IRS. The shareholder receives the net amount.

If a tax treaty exists between the US and your country of residence, the treaty rate typically reduces the withholding. For founders from the UK, Canada, Australia, Germany, and France, the treaty dividend rate for a significant shareholder (typically one owning 10% or more) is generally 5%. For smaller ownership percentages, the treaty rate is typically 15%. These rates are substantially lower than the 30% default but still represent a real cost on top of the 21% corporate tax already paid.

The double taxation calculation

The combined tax cost of extracting C-Corp profits as dividends is worth calculating explicitly so you understand what you are working with. Starting with $100 of pre-tax corporate profit:

• The C-Corp pays 21% federal corporate income tax, leaving $79 of after-tax profit

• If the $79 is distributed as a dividend to a non-resident alien shareholder in a treaty country at a 5% withholding rate, the withholding is $3.95, leaving $75.05

• Effective combined federal tax rate: approximately 25% on the original $100 of profit

• At the default 30% dividend withholding rate (no treaty), the withholding would be $23.70, leaving $55.30, for an effective combined rate of approximately 44.7%

State corporate income tax adds to these numbers where applicable. Home country tax on the dividend received may add further, depending on the jurisdiction and applicable credits. The point is that the combined cost is manageable in treaty countries but can be punishing in non-treaty situations. If you are from a country without a US tax treaty, the C-Corp dividend extraction path is significantly less efficient.

When to pay dividends and when not to

For early-stage C-Corps that are reinvesting all profits into growth, the dividend question does not arise because there are no distributable profits. The double taxation problem is deferred until the business generates consistent cash flow that the founders want to extract. By that point, the exit structure often becomes the more relevant consideration: a sale of shares is taxed as capital gains, not as dividends, and the capital gains treatment may be significantly more efficient.

For profitable, cash-generative C-Corps whose founders want regular income, the salary mechanism is typically more efficient than dividends because salary is deductible at the corporate level. The combination of a reasonable salary plus a dividend for any remaining profits is more tax-efficient than dividends alone, provided the salary can be justified as reasonable compensation for services performed.

5. Management Fees from your US Entity to your Foreign Entity

Management fees are payments made by your US entity to a foreign entity you own in exchange for genuine services that the foreign entity provides to the US business. They are one of the most useful tools available to non-US founders with an active foreign entity, and one of the most scrutinized by tax authorities on both sides of the transaction.

When management fees make sense

Management fees make sense when the following conditions are genuinely met: you have a real foreign entity that provides identifiable services to the US entity; those services have a market value that can be documented; and the US entity actually uses and benefits from those services. Common examples include strategic management and oversight services provided by the foreign parent, shared staff costs where the foreign entity employs people who spend a portion of their time on US entity work, technology or systems access provided by the foreign entity to the US entity, and marketing or business development services.

When all of these conditions are met, the management fee is deductible by the US entity as an ordinary and necessary business expense, which reduces the US entity's taxable income. The fee received by the foreign entity is taxable in that entity's jurisdiction as business income. The net effect is that profits generated by the US entity are partially shifted to the foreign entity, where they may be taxed at a lower rate or in a jurisdiction that interacts more favorably with your personal tax situation.

The arm's length requirement

Management fees between related entities must be set at arm's length, meaning the price must be what an unrelated third party would charge for the same services in the same circumstances. This is the transfer pricing requirement discussed in Part 5. A management fee that is set at a round number without any economic analysis, or that represents a significant portion of the US entity's revenue without a corresponding service justification, will be scrutinized by the IRS and potentially disallowed.

The consequences of a disallowed management fee are significant: the deduction is denied, increasing the US entity's taxable income and its tax liability, plus interest on underpaid tax and potential penalties. On the foreign entity's side, the revenue that was reported as a management fee may need to be reversed, with corresponding adjustments to that entity's returns.

Documentation requirements

A defensible management fee arrangement requires written documentation before the arrangement begins, not after. The documentation should include a written intercompany services agreement that describes the services to be provided, the basis on which the fee is calculated, the payment terms, and the period covered. It should be supported by evidence of the services actually performed: time records, meeting notes, deliverables, and any other record that demonstrates the foreign entity provided what the agreement says it would. And the fee itself should be supported by a brief analysis of comparable market rates for the same services from unrelated providers.

This does not need to be an elaborate transfer pricing study for a small or early-stage business. A clear intercompany agreement, a simple comparable market analysis (referencing published consulting rates, industry benchmarks, or comparable service provider quotes), and consistent monthly invoicing with supporting evidence of service delivery is sufficient for most founders. The discipline of maintaining this documentation from the start is far less burdensome than reconstructing it retroactively during an audit.

US withholding on management fees

The US withholding treatment of management fees depends on how the services are characterized. If the management services are performed outside the United States by the foreign entity, the fee may be sourced outside the US and not subject to US withholding. If the services are performed inside the United States, the fee may be ECI or FDAP income subject to withholding. The analysis turns on where the services are actually performed, which should be documented clearly in the intercompany agreement and the records of actual service delivery.

If US withholding applies to a management fee, the US entity as payer is responsible for withholding at the applicable rate and remitting to the IRS. Failure to withhold when required creates liability for the US entity.

See also - Transfer Pricing for International Businesses: Why Documentation Matters Before $10M Revenue

6. Payroll Setup for Founders who want to pay themselves a US Salary

If you have decided that paying yourself a salary from your US entity is appropriate for your situation, here is what that actually requires.

Federal employer registration

You need an EIN, which your entity should already have. The EIN is your employer identification number at the federal level. As an employer, your US entity is responsible for withholding federal income tax from each paycheck, withholding the employee portion of FICA taxes (6.2% Social Security plus 1.45% Medicare), paying the employer portion of FICA taxes (the same amounts), depositing these withheld and employer amounts with the IRS on the required schedule, filing Form 941 (Employer's Quarterly Federal Tax Return) four times per year, and issuing Form W-2 to each employee at the end of the year.

State employer registration

In every state where you or your employees physically work, you must register separately as a state employer. This involves registering with the state's department of revenue for income tax withholding and registering with the state's workforce agency for unemployment insurance. Each state has its own registration process, its own withholding tables, its own deposit schedule, and its own quarterly reporting requirements.

Payroll software

Running payroll manually is error-prone and time-consuming. The standard approach for early-stage US entities is to use a payroll software platform that handles withholding calculations, tax deposits, quarterly filings, and W-2 generation automatically. Gusto is the most commonly recommended platform for small businesses and startups, offering full-service payroll with automated federal and state tax filings, benefits administration, and contractor payment management. Rippling and Justworks are alternatives that combine payroll with HR management tools. QuickBooks Payroll integrates with QuickBooks accounting if that is your primary bookkeeping platform.

For a single founder-employee in one state, any of these platforms will handle the compliance burden at a cost of approximately $40 to $100 per month. The cost scales with the number of employees and states. The cost of not using a payroll platform, measured in missed deposits, incorrect withholding, and filing penalties, is typically much higher than the subscription fee.

Pay frequency

US payroll can be processed weekly, biweekly, semimonthly, or monthly. The most common frequencies for founders paying themselves are semimonthly (twice per month, on fixed dates such as the 1st and 15th) or monthly. The IRS deposit schedule for payroll tax deposits depends on the size of your payroll: small employers depositing less than $50,000 in payroll taxes annually deposit monthly; larger employers deposit more frequently. Your payroll software will handle the deposit schedule automatically.

7. FICA: Do Non-Resident Founders owe it?

FICA (Federal Insurance Contributions Act) taxes fund Social Security and Medicare. They are paid by employees and employers on wages and self-employment income. For non-resident alien founders, the FICA analysis is one of the most commonly misunderstood areas of US tax, and the answer depends on several factors that vary by individual circumstance.

The general rule

Non-resident aliens are generally subject to FICA on wages paid for services performed in the United States. If you are physically working in the United States, regardless of your immigration status, and you receive wages for those services, FICA taxes generally apply unless a specific exemption covers your situation.

Non-resident aliens are generally exempt from FICA on wages for services performed outside the United States. If you are working from your home country and receiving compensation from your US entity for that work, FICA may not apply. However, this position requires documentation: your employment agreement should specify that you are working outside the United States, your payroll records should reflect your non-US work location, and you should not be spending significant time in the US performing the same services for which you are paid.

Visa-based exemptions

Certain visa categories exempt the holder from FICA taxes regardless of where services are performed. Non-resident aliens in F, J, M, or Q status are exempt from FICA on wages paid for services in their primary immigration purpose: students on F visas, exchange visitors on J visas. However, these exemptions apply to the specific activities the visa was issued for, not to general employment by a US business. A founder on a tourist visa or Visa Waiver working in the US is not exempt from FICA.

Self-employment tax for LLC owners

Self-employment tax is the self-employed equivalent of FICA: 15.3% on net self-employment income up to the Social Security wage base, plus 2.9% Medicare on income above that threshold. For a US citizen or resident operating a disregarded LLC, net income from the LLC is generally subject to self-employment tax.

For a non-resident alien operating a disregarded LLC, the analysis is different. Non-resident aliens are not subject to self-employment tax on net income from a trade or business in the United States if they are treated as employees rather than self-employed for FICA purposes, or if they fall under an exception. However, the majority of non-resident alien LLC owners operating active US businesses do face some form of employment tax exposure, either through self-employment tax if treated as self-employed or through FICA if treated as employees of their own LLC. The specific treatment depends on the facts of the arrangement and should be confirmed with a US tax advisor.

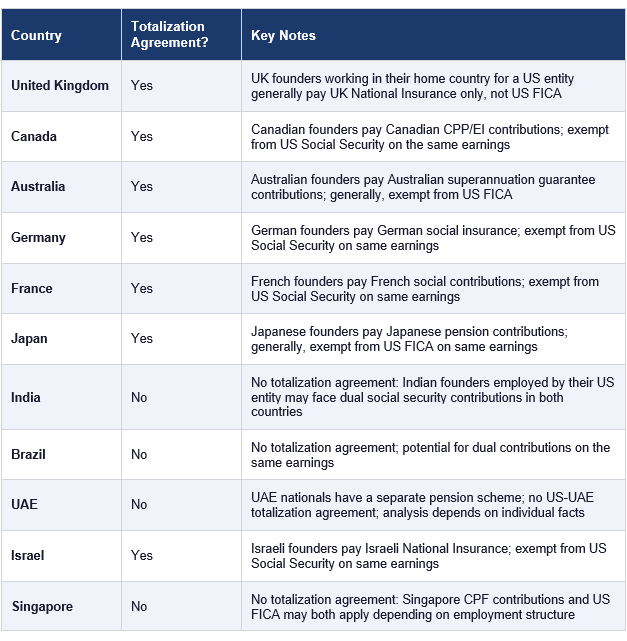

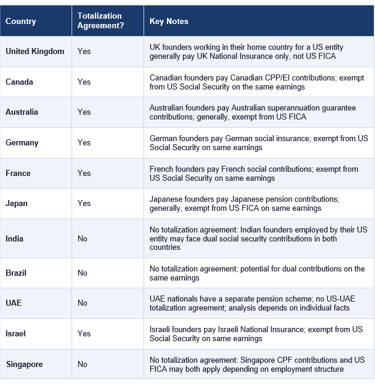

8. Totalization Agreements: Avoiding Double Social Security Contributions

A totalization agreement is a bilateral treaty between the United States and another country that coordinates the Social Security systems of both countries to prevent workers from paying Social Security taxes to both countries on the same earnings. For a non-US founder who is subject to social security contributions in their home country and who also has potential FICA exposure in the United States, a totalization agreement can eliminate the double contribution.

The United States has totalization agreements with approximately 30 countries. These agreements generally provide that a worker who is covered by one country's system is exempt from the other country's system for the same work. A UK founder who pays National Insurance contributions in the UK on the same earnings from their US entity would generally be exempt from US FICA on those earnings under the US-UK totalization agreement, provided they hold a Certificate of Coverage from the relevant UK authority.

How to claim totalization agreement benefits

To claim an exemption from US FICA under a totalization agreement, you generally need a Certificate of Coverage from your home country's social security authority. In the UK, this is issued by HM Revenue and Customs. In Canada, by Service Canada. In Australia, by the Australian Tax Office. The Certificate of Coverage confirms that you are covered under the home country system for the relevant period and that the earnings in question are subject to home country contributions, not US FICA.

The Certificate of Coverage is provided to your employer (the US entity, which in a founder context is yourself as the employing entity) and should be maintained as documentation supporting the FICA exemption claimed on payroll records. Without the certificate, the FICA exemption is harder to support in an audit.

Totalization agreement quick reference

No agreement does not mean you owe both: Even without a totalization agreement, the specific facts of your employment arrangement may mean that US FICA does not apply, for example because your services are genuinely performed outside the United States. The table above reflects the treaty position only. The full FICA analysis depends on the individual facts of your arrangement and requires professional advice.

9. Timing of Distributions and why it matters

The timing of distributions from a US entity is not tax-neutral. Both US and home country tax consequences can be affected by when you take money out, in what amounts, and in what legal form. Understanding the timing dynamics helps you make deliberate decisions rather than discovering unexpected tax consequences after the fact.

US timing considerations for LLC owners

For a single-member LLC owner, US income tax liability is determined by when the income is earned by the LLC, not when it is distributed. If your LLC earns $200,000 in a calendar year, you owe US tax on $200,000 for that year regardless of whether you took a distribution. However, the timing of distributions within the year affects your cash position relative to your quarterly estimated tax payment obligations.

A practical approach is to take distributions at approximately the same time as quarterly estimated tax payments are due: mid-April, mid-June, mid-September, and mid-January for the prior year's fourth quarter. Taking a distribution in conjunction with each estimated payment ensures you have the cash to meet the payment while not leaving excessive amounts sitting in the LLC earning no return.

US timing considerations for C-Corp shareholders

For a C-Corp shareholder, dividends are taxable in the year they are received, not in the year the profits were earned. This gives the corporation and its board some control over the timing of the tax event for shareholders. Declaring a dividend in December versus January of the following year determines which tax year the shareholder includes the income in. For a shareholder expecting a higher income year next year, delaying the dividend to the current lower-income year can be beneficial. For a shareholder expecting lower income next year, deferring the dividend can also be beneficial.

Dividend declarations by a C-Corp must be documented by a board resolution specifying the dividend amount, the record date, and the payment date. A dividend payment made without board documentation is informally treated as a salary or disguised dividend and can create tax and employment tax complications.

Home country timing considerations

The timing of when your home country taxes the income from your US entity depends on whether your home country treats the entity as transparent or opaque. For transparent treatment (as Canada generally applies to US LLCs), the income is taxed when earned, same as the US. For opaque treatment (as the UK generally applies to US LLCs), the income may be taxed when distributed, creating a potential timing difference from the US treatment. In situations where the US taxes income when earned and your home country taxes it when distributed, you may be managing two different tax cycles simultaneously, each with their own payment timing and cash flow implications.

This is one of the reasons why getting clarity on your home country's treatment of your US entity structure before you begin operations is valuable. If you know your home country treats the LLC as opaque, you can plan your distribution timing to align your home country tax payment with the cash flow from the distribution. If you do not know how your home country treats the structure, you may end up with cash flow surprises that are expensive to manage.

10. How your Home Country treats each Method

The home country tax treatment of income extracted from a US entity is covered in detail in Part 13 by jurisdiction. This section provides a framework for thinking about the question before you get to that level of detail, because the general principles apply regardless of which country you are in.

Salary

A salary paid by your US entity to you personally is almost universally treated as employment income in your home country. Most countries tax employment income at rates comparable to or higher than investment income. The US will have withheld income tax and potentially FICA from the salary; your home country will want to tax the same income as well. The mechanism for avoiding double taxation is the credit system: most countries allow you to credit the foreign tax paid against your domestic liability on the same income. Whether the credit fully covers the US tax depends on your home country's tax rate and the applicable treaty.

Distributions from an LLC

The home country treatment of LLC distributions depends entirely on whether your home country treats the LLC as transparent or opaque. If transparent, the income is already considered yours when earned, and the distribution is not a new taxable event. If opaque, the distribution may be treated as a dividend from a foreign corporation, taxed at your home country's dividend rates with credit available for any US withholding. The UK, as noted, generally treats US LLCs as opaque, creating potential mismatches. Canada generally treats them as transparent. Australia and Germany have their own rules that require individual analysis.

Dividends from a C-Corp

A dividend from a US C-Corp is recognizable to most home country tax systems as a dividend from a foreign company. Most countries tax dividends received by residents as income, with rates ranging from the same as ordinary income to preferential rates for qualified dividends or participation exemptions for corporate recipients. Tax treaties between the US and your home country typically address the credit for US withholding against your home country liability on the same dividend.

Management fees

Management fees received by your foreign entity from the US entity are business income of the foreign entity, taxed in that entity's jurisdiction at the applicable corporate or business income tax rate. The fee reduces your US entity's taxable income, which is the primary US benefit. The home country benefit depends on the tax rate your foreign entity pays on that income compared to what the income would have been taxed at if left in the US entity. This is the essence of the management fee planning strategy: shifting income from a higher-tax jurisdiction to a lower-tax jurisdiction through a legitimate intercompany service arrangement.

11. Practical Recommendations by Situation

Having covered each extraction method in detail, the following guidance addresses the most common founder situations. These are starting frameworks, not final answers. Your specific situation requires professional advice from someone who understands both your US position and your home country position simultaneously.

Single-member LLC, no US physical presence, working from home country

The most common scenario for early-stage non-US founders. The cleanest approach is typically to leave income in the LLC throughout the year to fund operations, take distributions at quarterly intervals aligned with estimated tax payments, and not set up US payroll. The LLC's ECI is taxed on Form 1040-NR at year end. Distributions are reported on Form 5472 as reportable transactions. Home country tax on the same income depends on your jurisdiction's treatment of the LLC. Get clarity on whether your home country treats the LLC as transparent or opaque before your first distribution.

C-Corp, founder remains outside the US, pre-revenue or early revenue

In this stage, there is typically no cash to distribute, and the double taxation question is theoretical rather than practical. The founder is not yet taking salary if there is no revenue to fund it. Focus on maintaining the corporate formalities, keeping accurate books, and understanding the mechanics for when cash flow begins. When the time comes to extract cash, model the salary versus dividend comparison with your specific treaty rate and home country tax rate, and decide which combination is most efficient.

C-Corp, VC-backed, founder relocating to the US

This situation requires immigration advice, pre-immigration tax planning, and a review of your home country entity structure before you become a US tax resident. Once you are a US tax resident, your worldwide income is taxable in the US. If you own a foreign company, it may become a Controlled Foreign Corporation with current US inclusion obligations. The salary from your C-Corp is taxable as ordinary income in the US. Optimize the extraction structure before you move, not after. This is one of the highest-value planning opportunities available to founders, and one that closes permanently once you acquire US tax residency.

Founder with both a US LLC and a home country operating company

This is the multi-entity situation where management fees are most relevant. If your home country company provides genuine services to the US LLC, a well-documented management fee arrangement shifts income to the home country entity and reduces US LLC taxable income. The arm's length requirement must be met. Document the arrangement before transactions begin. Invoice monthly with supporting evidence of services delivered. Have a brief transfer pricing analysis prepared to support the fee level. Review the arrangement annually as the business grows and the services evolve.

Before you move to Part 8

Part 8 covers accounting and bookkeeping for foreign-owned US entities: why it matters more than for domestic entities, which accounting software works best, how to handle intercompany transactions, FX accounting, and what records you are required to maintain and for how long.

Before you move on, confirm that you have clarity on the following from this part:

• Which extraction method or combination of methods is appropriate for your entity type and personal situation

• Whether you need US payroll set up, and if so, which platform you will use

• Whether you understand how your home country treats the extraction method you have chosen

• Whether a totalization agreement applies to your situation and whether you have obtained the necessary Certificate of Coverage if so

• Whether any management fee arrangement between your US entity and a foreign entity is documented with a written intercompany agreement and transfer pricing support

• Whether you have aligned your distribution timing with your estimated tax payment schedule

Antravia Advisory: The extraction question is where US tax planning and home country tax planning must work together. Getting the method right, the timing right, and the documentation right requires someone who understands both sides of the equation. We work with non-US founders to structure their extraction strategy so it is efficient in both jurisdictions and defensible in either.

Continue to Part 8: Accounting and Bookkeeping

© Antravia Advisory | antravia.com | This guide is for informational purposes only and does not constitute legal or tax advice.

About Antravia Advisory

Antravia Advisory is a US-based tax and accounting advisory firm headquartered in Winter Park, Florida, operating nationally and internationally.

We advise international businesses entering the United States and complex US companies operating across multiple states, entities, and revenue structures. Our work spans advanced tax strategy, multi-state sales tax oversight, cross-border structuring, and high-level accounting architecture for e-commerce brands, subscription and SaaS businesses, platform-based models, and multi-entity groups.

We work with founders and leadership teams who require technical precision, structural clarity, and financial frameworks built for scale, capital events, and long-term resilience.

The Non-US Founder’s Complete Guide to Running a US Business

Part 1 — Before You Start

Part 2 — Choosing Your US Entity

Part 3 — Formation

Part 4 — US Banking

Part 5 — US Federal Tax

Part 6 — US State Tax

Part 7 — Paying Yourself

Part 8 — Accounting and Bookkeeping

Part 9 — Annual Compliance Calendar

Part 10 — Hiring in the US

Part 11 — Intellectual Property and Contracts

Part 12 — Your Home Country Obligations

Part 13 — Applied Business Types

Part 14 — Exiting, Winding Down, or Restructuring

Disclaimer:

Content published by Antravia is provided for informational purposes only and reflects research, industry analysis, and our professional perspective. It does not constitute legal, tax, or accounting advice. Regulations vary by jurisdiction, and individual circumstances differ. Readers should seek advice from a qualified professional before making decisions that could affect their business.

See also our Disclaimer page

Antravia Advisory

Accounting built for complexity

Not legal advice, always verify with your Accountant

Email:

Contact us:

© 2025. All rights reserved. | Disclaimer | Privacy Policy | Terms of Use |

contact@antravia.com

Antravia LLC

941 W Morse Blvd suite 100

Winter Park

Florida

32789