UK Pensions and U.S. Tax: The 25% Pension Lump Sum and US Tax

What the Treaty Says, What the IRS Says, and What It Actually Means for UK Expats in America

UK CITIZENS IN THE US

3/17/202615 min read

If you have a UK pension and you have moved to the United States, one of the most consequential financial decisions you will face is when and how to access your pension. The 25% pension commencement lump sum, known in UK legislation as the Pension Commencement Lump Sum or PCLS, is central to that decision. In the UK it is completely free of income tax. In the United States, the position is far less straightforward, and getting it wrong in either direction can be expensive.

This article explains the treaty provisions in detail, sets out the IRS position as established in its own published guidance, addresses the arguments that exist on both sides, and tells you what you actually need to know before you take a penny out of your pension as a US tax resident.

Part 1: What the PCLS is and why it Matters

Under UK pension law, when you access a defined contribution pension such as a SIPP or a workplace pension, you are entitled to take up to 25% of the fund as a tax-free lump sum from age 55 onwards (rising to 57 from 2028). This is the pension commencement lump sum. The remaining 75% is drawn as taxable income, whether through an annuity, flexi-access drawdown, or uncrystallised fund pension lump sums.

The PCLS is not a concession or a relief. It is a statutory entitlement built into the UK pension system. HMRC does not tax it. The pension provider does not withhold income tax on it. It arrives in your bank account gross.

For someone with a SIPP worth £400,000, the PCLS is £100,000. For someone with a larger fund, it could be significantly more, subject to the lump sum allowance that replaced the lifetime allowance from April 2024. For most people it is the single largest tax-free receipt they will ever receive in the UK.

The question of whether the United States also exempts it from tax is therefore not academic. On a £100,000 PCLS, if the US taxes it as ordinary income at a 24% federal rate, the US tax bill alone is approximately $30,000. If an exemption is available and properly claimed, that liability disappears. The stakes are real.

Part 2: The Treaty Framework

The United States and the United Kingdom have a comprehensive income tax treaty in force. The current treaty was signed in 2001 and amended a by protocol in 2002 and and an Exchange of Notes in 2003. Articles 17 and 18 covers pensions and is the relevant provision.

Article 17(1): The General Rule

Article 17(1)(a)

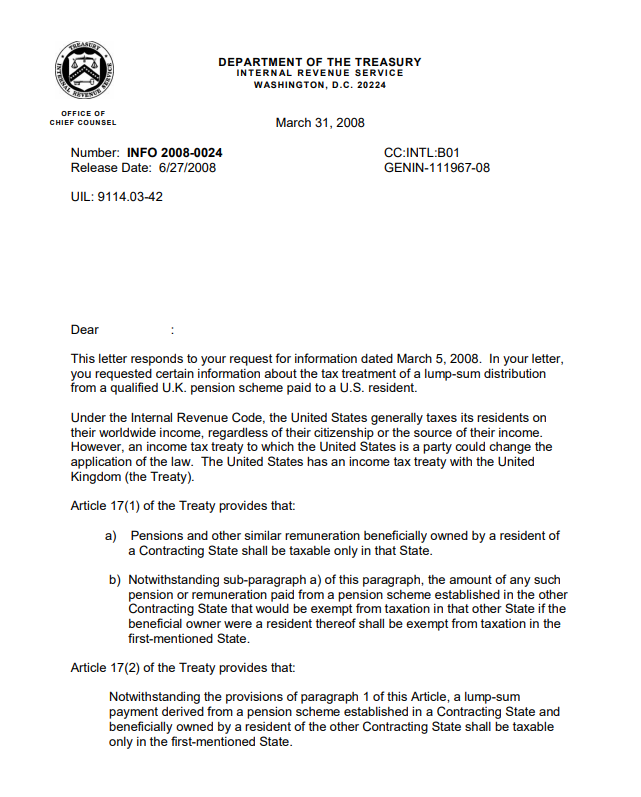

Pensions and other similar remuneration beneficially owned by a resident of a Contracting State shall be taxable only in that State.

This establishes the basic principle that pensions and other similar remuneration beneficially owned by a resident of one contracting state are taxable only in that state. For a UK expat living in the US, this means UK pension income is taxable in the US as the country of residence. That is the default position and it is relatively uncontroversial for periodic pension payments.

Article 17(1)(b) adds an important provision.

Notwithstanding sub-paragraph a) of this paragraph, the amount of any such pension or remuneration paid from a pension scheme established in the other Contracting State that would be exempt from taxation in that other State if the beneficial owner were a resident thereof shall be exempt from taxation in the first-mentioned State

This states that an amount paid from a pension scheme established in the other contracting state that would be exempt from taxation in that state if the beneficial owner were a resident thereof shall be exempt from taxation in the first-mentioned state. On a literal reading, because the PCLS would be exempt from UK income tax if the recipient were a UK resident, it should also be exempt in the US. This is the treaty argument for exemption and it has genuine textual support.

Article 17(2): Lump Sums

Article 17(2)

Notwithstanding the provisions of paragraph 1 of this Article, a lump-sum payment derived from a pension scheme established in a Contracting State and beneficially owned by a resident of the other Contracting State shall be taxable only in the first-mentioned State.

This addresses lump sums specifically. It provides that a lump-sum payment derived from a pension scheme established in a contracting state and beneficially owned by a resident of the other contracting state shall be taxable only in the first-mentioned state. For a UK SIPP and a US resident, this would mean the lump sum is taxable only in the UK, the state where the pension scheme is established.

Since the UK exempts the PCLS from income tax, Article 17(2) read alone would produce the result that a UK pension lump sum received by a US resident is taxable only in the UK, and since the UK does not tax it, it would be tax-free in both countries. That is the strongest possible textual reading in favour of exemption (but keep reading!)

The Saving Clause: Where the Argument Unravels

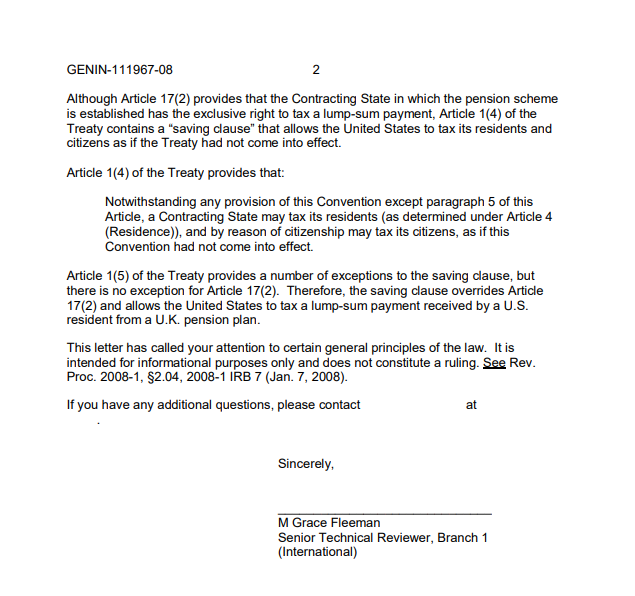

Article 1(4) of the treaty contains what is known as a saving clause.

Notwithstanding any provision of this Convention except paragraph 5 of this Article, a Contracting State may tax its residents (as determined under Article 4 (Residence)), and by reason of citizenship may tax its citizens, as if this Convention had not come into effect.

This is a standard feature of US tax treaties and it effectively allows the United States to tax its residents and citizens as if the treaty had not come into effect, subject to specific exceptions listed in Article 1(5).

The provisions of paragraph 4 of this Article shall not affect: a) the benefits conferred by a Contracting State under paragraph 2 of Article 9 (Associated Enterprises), sub-paragraph b) of paragraph 1 and paragraphs 3 and 5 of Article 17 (Pensions, Social Security, Annuities, Alimony, and Child Support), paragraph 1 of Article 18 (Pension Schemes) and Articles 24 (Relief From Double Taxation), 25 (Non-discrimination), and 26 (Mutual Agreement Procedure) of this Convention; and b) the benefits conferred by a Contracting State under paragraph 2 of Article 18 (Pension Schemes) and Articles 19 (Government Service), 20 (Students), and 28 (Diplomatic Agents and Consular Officers) of this Convention, upon individuals who are neither citizens of, nor have been admitted for permanent residence in, that State.

Article 17(2) is not listed as an exception to the saving clause in Article 1(5). This is the critical point. Because Article 17(2) is not carved out from the saving clause, the US retains the right to tax a lump sum received by a US resident from a UK pension, notwithstanding the exclusive taxation rule in Article 17(2).

The question of whether Article 17(1)(b) survives the saving clause is more complex and has generated more debate. Some practitioners argue that 17(1)(b), as a reciprocal exemption provision, operates differently from 17(2) and may survive the saving clause in a way that 17(2) does not. This is technically arguable but has not been definitively established.

Part 3: What the IRS Has Actually Said

In June 2008, the IRS Office of Chief Counsel published a document that is the closest thing to official IRS guidance on this question. It is Information Letter INFO 2008-0024, issued by M. Grace Fleeman, Senior Technical Reviewer, Branch 1 (International). It is publicly available on the IRS website, and copied at the end of this article.

The letter was written in response to a specific request for information about the US tax treatment of a lump-sum distribution from a qualified UK pension scheme paid to a US resident. It is short, precise, and worth reading in full. The key passage states:

Although Article 17(2) provides that the Contracting State in which the pension scheme is established has the exclusive right to tax a lump-sum payment, Article 1(4) of the Treaty contains a 'saving clause' that allows the United States to tax its residents and citizens as if the Treaty had not come into effect. Article 1(5) of the Treaty provides a number of exceptions to the saving clause, but there is no exception for Article 17(2). Therefore, the saving clause overrides Article 17(2) and allows the United States to tax a lump-sum payment received by a U.S. resident from a U.K. pension plan.

The letter then clarifies that it does not constitute a ruling and is intended for informational purposes only. It is therefore not binding on the IRS or on taxpayers. But it is the IRS's own articulation of its position, signed by a senior official in the international division, and it there has been some consistency with how the IRS has approached this question in practice ever since (Although clearly, we do not have access to every IRS decision)

An IRS Information Letter is not a revenue ruling or a formal private letter ruling. It does not carry the same legal weight as binding guidance. But it reflects the IRS position and it is the document practitioners cite when this question arises.

Part 4: The Argument for Exemption and Why Most Practitioners Reject It

The Textual Case for Exemption

The argument in favour of exempting the PCLS from US tax rests primarily on Article 17(1)(b). The provision states clearly that amounts that would be exempt in the source state if the recipient were resident there shall be exempt in the residence state. The PCLS is exempt in the UK. On a literal reading, it should therefore be exempt in the US.

Proponents of this view argue that 17(1)(b) operates as a specific exemption provision rather than simply as an allocation rule, and that it may have a stronger claim to surviving the saving clause than 17(2). They also note that the IRS's 2008 letter specifically addresses 17(2) and does not directly address 17(1)(b), leaving the argument under that provision technically open.

Why the Weight of Opinion Goes the Other Way

Despite the textual argument, the overwhelming majority of cross-border tax practitioners treat the PCLS as taxable in the US. There are several reasons for this.

First, the anti-double-non-taxation principle. The UK SIPP system works as follows. Contributions go in with UK tax relief, meaning the money was never taxed as income on the way in. The fund grows free of UK income tax and capital gains tax. The 25% comes out free of UK income tax. The 75% is taxed as income when drawn. The net result for the 25% is that the money was never taxed in the UK at any point, either on the way in or the way out. Allowing it to also escape US tax creates a situation where a significant sum is taxed nowhere. The treaty is generally not designed to produce double non-taxation, and the IRS resists interpretations that lead to that result.

Second, the saving clause analysis. Even if 17(1)(b) provides a stronger textual basis than 17(2), the saving clause in Article 1(4) is broad. The exceptions in Article 1(5) are exhaustive. Neither 17(1)(b) nor 17(2) appears in those exceptions. The IRS's position is that the saving clause applies to both and overrides both.

Third, the absence of favourable authority. No revenue ruling, no court case, and no formal IRS guidance has accepted the exemption argument for the PCLS. The 2008 information letter points the other way. Without favourable authority, arguing for exemption may require taking a treaty position on Form 8833, which invites scrutiny and potentially audit attention.

The Practical Risk Calculation

For a US expat taking a large PCLS, the decision is not purely academic. It involves weighing the strength of a legal argument that has not been definitively tested against the risk of an IRS challenge, potential underpayment penalties, interest, and the cost of defending the position.

Most practitioners advise their clients to treat the PCLS as taxable US ordinary income and manage the tax liability through planning rather than through a treaty exemption claim that may not succeed. That is the conservative and common approach. It is not necessarily the only approach, but the burden of proof for the exemption position lies with the taxpayer.

Part 5: The Source of Contributions Argument

One nuance that most practitioner commentary acknowledge is the source of contributions argument. Not all pension contributions attract UK tax relief. If a portion of your SIPP was funded by contributions on which no UK tax relief was claimed, the double non-taxation argument does not apply to that portion. Those contributions were genuinely post-tax money.

In theory, a taxpayer could argue that the 25% lump sum attributable to post-tax contributions should be treated differently from the 25% attributable to relieved contributions. In practice, tracing contributions in a SIPP that has been running for many years and has received both employer contributions, personal contributions with relief, and possibly transfers from other schemes is extraordinarily complex.

Most practitioners do not attempt this analysis because the tracing burden is prohibitive and the IRS has not provided a mechanism for it. It remains a theoretical argument that has not been practically validated.

Part 6: Timing and Planning Considerations

Given that the PCLS is likely to be taxable in the US, the practical question becomes how to minimise the tax impact rather than whether to avoid it altogether.

Taking the PCLS Before Becoming a US Tax Resident

The most effective planning tool available is timing. If you take your pension commencement lump sum before you become a US tax resident, the IRS generally has no claim on it (unless of course you are a US citizen). It arrives as a UK tax-free receipt before the US taxation framework applies to you. Once spent or invested, it is outside the pension wrapper and the US tax position going forward relates only to the invested proceeds, not to the pension distribution itself.

This option requires that you are at the pension access age of 55 or above and that your move to the US is far enough in the future that you can crystallise the pension before departure. For those who have already moved, this option is no longer available.

If you are planning to move to the United States and you are over 55 with a meaningful SIPP, taking the PCLS before you establish US tax residency is one of the most significant planning opportunities available to you. It should be addressed before your move, not after.

Income Spreading for those already in the US

For those who are already US tax residents and have not yet crystallised their pension, the taxable PCLS may be ordinary income in the year of receipt. If you take it in a year when your other US income is lower, for example in a gap year between employment, or before Social Security begins, the marginal rate applied to it may be lower. Spreading the crystallisation over multiple tax years may not possible for the PCLS itself, which is a single event, but the year of crystallisation can be chosen strategically. UK pension rules could allow phased crystallisation (but check for your specific pension), producing tax-free amounts over time rather than one single all-at-once event.

Foreign Tax Credit Interaction

The UK does not tax the PCLS. There is therefore no UK tax to credit against the US liability. The foreign tax credit mechanism, which prevents double taxation by allowing UK tax paid to offset US tax due, does not help with the PCLS because there is no UK tax paid. This is part of why the double non-taxation concern drives the IRS position and why the planning focus must be on timing rather than on credits.

State Tax

Federal income tax is not the only consideration. Most US states that have an income tax will also treat the PCLS as taxable income. Florida, Texas, and a handful of other states have no state income tax, which is one reason Florida is particularly attractive for UK expats planning to crystallise pensions. If you are resident in a high-income-tax state such as California or New York, the combined federal and state tax burden on the PCLS can be substantial.

Part 7: Uncrystallised Fund Pension Lump Sums

A separate but related issue arises with Uncrystallised Fund Pension Lump Sums, known as UFPLSs. An UFPLS is a withdrawal directly from an uncrystallised pension fund where 25% of each withdrawal is tax-free in the UK and 75% is taxable. Rather than designating a specific amount as the PCLS upfront and then drawing from a drawdown fund, the member blends the two elements in each withdrawal.

For US tax purposes, the treatment of an UFPLS is even less certain than for a standard PCLS. Because the tax-free and taxable elements are blended in each payment rather than separated into a distinct lump sum event, it is not clear whether the 25% tax-free element of each UFPLS payment should be treated as a separate lump sum for the purposes of IRS INFO 2008-0024, as periodic pension income, or as something else entirely.

No specific IRS guidance addresses UFPLSs, which only became available in the UK from April 2015, after the 2008 information letter was published. Practitioners have taken varying positions. Given the uncertainty, UFPLSs for US-resident pension holders carry particular risk and require specific advice.

Part 8: What to Do if you have already taken the PCLS

If you have already taken your pension commencement lump sum as a US tax resident and have not reported it on your US tax return, you have a problem that needs to be addressed. The approach depends on whether the omission was wilful or non-wilful in the IRS's assessment.

Non-Wilful Omissions

If you simply did not know that the PCLS was reportable as US income, that is likely a non-wilful omission although this is a facts-and-circumstances determination. The IRS has a Streamlined Filing Compliance Procedure designed for US taxpayers who have inadvertently failed to report foreign income. Under the domestic version of the streamlined procedure, you file amended returns for the three most recent tax years, pay the tax due plus interest, and pay a 5% miscellaneous offshore penalty based on the highest aggregate value of unreported foreign accounts during the period. This is significantly cheaper than the alternative.

Wilful Omissions

If you were aware that the PCLS was potentially taxable in the US and chose not to report it, the analysis is more serious. Wilful non-disclosure of foreign income can attract substantial FBAR penalties, civil fraud penalties, and in egregious cases, criminal prosecution. This is not a situation to address without proper professional advice.

Amended Returns

For more recent omissions where no foreign account reporting is involved, simply filing an amended Form 1040-X for the relevant year, reporting the PCLS as income, and paying the tax and interest may be the most straightforward approach. The appropriate route depends on the specific facts and the overall compliance picture.

Part 9: The Bottom Line

The 25% pension commencement lump sum from a UK pension MAY almost certainly taxable in the United States for a US tax resident. The IRS has said so in its own published, but not binding, guidance, the saving clause analysis supports that conclusion, and the weight of professional opinion is consistent with it.

The treaty argument for exemption under Article 17(1)(b) exists and has not been definitively closed by the courts or by formal IRS guidance. But it has also never been validated, and relying on it carries real risk. For most people with meaningful pension funds, the risk of an IRS challenge and the associated costs of defending an untested treaty position outweigh the benefit.

The most effective planning tool is timing. Taking the PCLS before becoming a US tax resident eliminates the US tax exposure entirely. For those already in the US, the focus should be on managing the year of crystallisation to minimise the effective tax rate, taking advantage of states with no income tax, and ensuring that the pension interaction with other aspects of the US tax return, the treaty election for accumulation, and any FBAR or Form 8938 reporting, is handled correctly as a whole.

Do not take your pension commencement lump sum as a US tax resident without first obtaining specific advice from a cross-border tax specialist who understands both UK pension structures and the US/UK treaty. The planning window before you crystallise your pension is the most valuable time to act. Once the distribution is made, the options are limited to managing the tax bill rather than avoiding it.

Key References

• IRS Information Letter INFO 2008-0024 (June 27, 2008), M. Grace Fleeman, Senior Technical Reviewer, Branch 1 (International) — available at irs.gov/pub/irs-wd/08-0024.pdf

• US/UK Income Tax Treaty (2001) with protocols (2002, 2003) — Article 1 (Saving Clause), Article 17 (Pensions)

• IRC Section 72 — Annuities, Certain Proceeds of Endowment and Life Insurance Contracts

• Form 8833 — Treaty-Based Return Position Disclosure

• IRS Streamlined Filing Compliance Procedures — irs.gov

About Antravia Advisory

Antravia Advisory is a cross-border tax and advisory firm founded by a chartered accountant with 25 years of experience in international tax and financial architecture. We advise UK expats in the United States, international founders operating across borders, and complex US businesses with international operations. We work with clients who need someone who understands both sides of the equation.

antraviaadvisory.com | contact@antravia.com

Disclaimer: This article is published for informational purposes only and reflects research, professional analysis, and our perspective on a genuinely uncertain area of cross-border tax law. It does not constitute legal, tax, or accounting advice. The US tax treatment of UK pension lump sums involves real legal complexity, and individual circumstances differ significantly. Readers should obtain specific professional advice before making any pension decisions. Antravia Advisory does not accept liability for reliance on this article.

Our UK Expats in US Series

UK Citizens Moving to the U.S.: Tax Issues to Understand Before You Arrive

ISAs and UK Investments Under U.S. Tax: What Stops Being Tax-Free

Selling UK Property After Moving to the U.S.: Capital Gains and Timing Risks

UK Pensions and U.S. Tax: What Happens to Your SIPP When You Move to America

UK Pensions and U.S. Tax: The 25% Pension Lump Sum and US Tax

US–UK Tax Treaty Explained: Dual Residency, Pensions, and Cross-Border Tax Planning for UK Expats

FBAR and FATCA for UK Expats: Reporting Your UK Accounts to the IRS

FIRPTA Explained: U.S. Tax Withholding When Foreign Owners Sell Property

U.S. Tax for Foreign Owners of Rental Property: A Guide for UK Investors

Disclaimer:

Content published by Antravia is provided for informational purposes only and reflects research, industry analysis, and our professional perspective. It does not constitute legal, tax, or accounting advice. Regulations vary by jurisdiction, and individual circumstances differ. Readers should seek advice from a qualified professional before making decisions that could affect their business.

See also our Disclaimer page

Antravia Advisory

Accounting built for complexity

Not legal advice, always verify with your Accountant

Email:

Contact us:

© 2025. All rights reserved. | Disclaimer | Privacy Policy | Terms of Use |

contact@antravia.com

Antravia LLC

941 W Morse Blvd suite 100

Winter Park

Florida

32789