Part 4: US Banking

The Non-US Founder's Complete Guide to Running a US Business - Part 4 explains US banking for non-US founders, what banks and fintechs require, which options are most accessible, how remote vs in-person opening works, what to do after rejection, and how Stripe, Wise, and payment tools fit into a practical US banking setup.

THE NON-US FOUNDER'S COMPLETE GUIDE TO RUNNING A US BUSINESS

3/3/202622 min read

Forming a US entity takes a day. Opening a US bank account as a foreign-owned business can take weeks, requires documentation that nobody told you to prepare, and ends in rejection more often than the formation guides suggest.

This part covers everything you need to know about US banking as a non-US founder: why it is difficult, which institutions are genuinely accessible, what documentation you need, what to do if you are rejected, and how payment processors and alternative financial tools fit into your overall setup. By the end of this section, you will have a clear plan for your US banking infrastructure rather than discovering the problems after your entity is already formed.

1. Why Opening a US Bank Account is sometimes harder than forming the Company

The difficulty non-US founders face in opening US business bank accounts is not accidental. It is the direct result of federal anti-money laundering law, Know Your Customer regulations, and the enforcement actions that US regulators have taken against banks that failed to adequately screen foreign-owned accounts.

The regulatory environment

US banks are subject to the Bank Secrecy Act, the USA PATRIOT Act, and the rules issued by the Financial Crimes Enforcement Network (FinCEN) under those statutes. These rules require banks to verify the identity of their customers, understand the nature of their business, assess the risk that the account may be used for money laundering or terrorist financing, and maintain records sufficient to satisfy regulatory examiners.

Foreign-owned businesses are categorized as higher risk under most bank compliance frameworks. This is not because foreign founders are more likely to engage in financial crime. It is because the bank has less information about them: their credit history is not visible in US systems, their identity documents may be from unfamiliar jurisdictions, their business relationships are harder to verify, and the regulatory consequences of getting it wrong are severe. Banks that have faced enforcement actions for inadequate AML compliance have learned to be conservative, and their conservatism shows up as rejection rates that many founders find frustrating.

What banks are actually evaluating

When a bank reviews an account application from a foreign-owned US entity, its compliance team is asking a specific set of questions. Understanding what those questions are helps you prepare an application that answers them clearly.

• Who actually owns this entity? Banks need to identify beneficial owners with 25% or more ownership and verify their identities. For a sole foreign founder, this means verifying your identity against a government-issued ID and assessing the risk associated with your country of origin.

• What does this business actually do? Banks want to understand your business model clearly. A vague description like 'consulting' triggers more scrutiny than a specific description like 'software development services for US-based SaaS companies.' The more concrete and verifiable your business description, the better.

• Where does the money come from and where does it go? Banks assess expected transaction patterns: How much revenue do you expect per month? How many transactions? Who are your customers? Will you be receiving wire transfers from foreign entities? Will you be sending money abroad? Unusual patterns relative to your stated business model generate scrutiny.

• Is this a real business or a shell? Banks look for evidence that your business has genuine commercial substance. A website, existing customers, signed contracts, or a track record of revenue all help. An entity with no website, no customers, and no transaction history is harder to underwrite.

• Does this entity or its owners appear on sanctions lists? Every bank runs applications against OFAC sanctions lists and other government watch lists. This is automatic and non-negotiable. If your name, your country of operation, or any associated party appears on a relevant list, your application will be declined regardless of other factors.

Countries that create additional friction

Founders from certain countries face additional scrutiny regardless of their personal circumstances. This includes countries that are subject to US sanctions (Iran, North Korea, Cuba, Syria, and the Crimea, Donetsk, and Luhansk regions), countries on the Financial Action Task Force (FATF) grey list or blacklist for deficiencies in anti-money laundering controls, and countries that US banks' internal risk models categorize as elevated risk based on historical patterns.

If you are from a country in any of these categories, your path to a US bank account is not impossible, but it requires more documentation, more patience, and in some cases a personal visit to the bank. Fintech options like Mercury and Relay have somewhat more flexible risk models than traditional banks, but they are not immune to country-based restrictions either.

2. What Banks actually require from Foreign-Owned Businesses

The specific documentation requirements vary by institution, but the following list covers what virtually every US bank or fintech will ask for. Having all of this ready before you apply will significantly reduce the back-and-forth that slows most applications down.

Entity documents

• Certificate of Formation or Certificate of Incorporation: the state-issued document confirming your entity exists. This must be the official version, not a draft or a copy of your filed application.

• Employer Identification Number (EIN): your federal tax identification number. Some banks accept a verbal EIN during the application and request the IRS confirmation letter (CP 575) before account activation. Others require the CP 575 upfront.

• Operating Agreement (for LLCs) or Bylaws and Board Resolutions (for C-Corps): the internal governance document establishing who has authority to open accounts and act on behalf of the entity. Banks use this to verify that the person applying is authorized to do so.

• Any DBA (Doing Business As) registration if your business operates under a trade name different from its legal name.

Personal identification documents

• Passport: your current, valid passport is the standard identification document for non-US founders. Some banks also accept a national identity card from certain countries.

• Secondary ID: some banks request a second form of identification, such as a driver's license from your home country.

• Proof of address: a recent utility bill, bank statement, or official government document showing your personal address. This must be current (typically within 90 days) and in your name.

Business information

• Business description: a clear, specific description of what your company does, who its customers are, and how it generates revenue. Write this out in advance rather than improvising it during the application.

• Expected transaction volume: banks ask for an estimate of monthly revenue, average transaction size, and number of transactions per month. Be honest and realistic. Overstating expected volume to appear more established creates compliance flags later.

• Source of funds: where the initial deposit is coming from and where ongoing business revenue originates. For early-stage companies, this typically means your personal savings or an initial capital contribution.

• Business website: most banks verify that your business website exists and is consistent with your stated business description. An unbuilt or under-construction website creates friction.

• Customer information: some banks ask for the names of your existing customers or the names of the jurisdictions you will be transacting with. For founders who have not yet launched, this is sometimes unavoidable friction.

US address

This is one of the most common sticking points. Most banks require a US address for the business, separate from your registered agent address. As discussed in Part 3, a virtual office address from a legitimate provider such as Regus or Alliance Virtual Offices is generally acceptable. A PO box, a UPS Store mailbox, or a commercial mail receiving agency address registered as a private mailbox is typically not acceptable for banking purposes.

Some fintech banks, particularly Mercury, have been more flexible on this requirement for international founders, accepting foreign addresses in certain cases. However, this is not guaranteed, and having a US virtual office address ready before you apply removes a point of friction that can otherwise delay or derail your application.

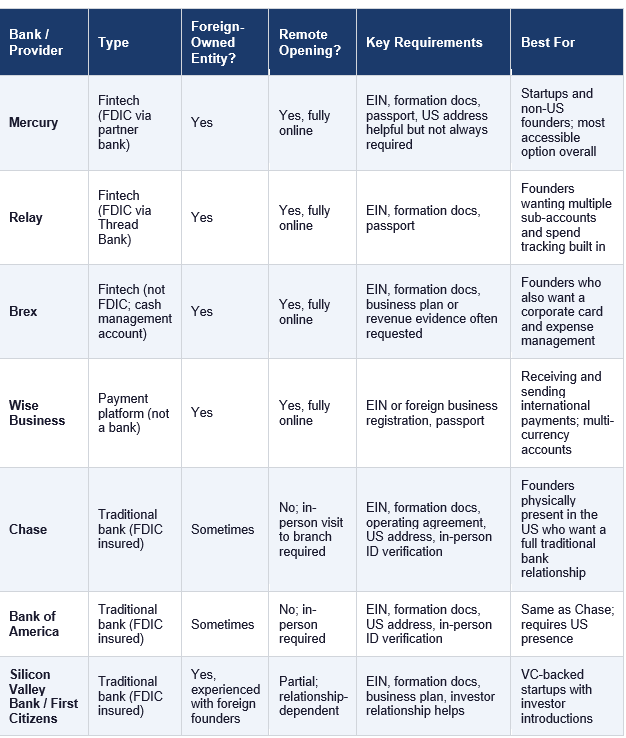

3. Which Banks Are Most Accessible for Non-US Founders

The landscape of US business banking has changed significantly over the past decade. Fintech banking platforms have made US accounts genuinely accessible to foreign-owned entities in a way that was not possible when all banking required an in-person visit. The table below summarizes the most relevant options.

Mercury

Mercury is the most commonly recommended US banking option for non-US founders, and for good reason. Its application process is fully online, it is designed with technology companies and startups in mind, and its compliance team has experience with foreign-owned entities. Mercury is not a bank itself but operates through partner banks that are FDIC insured. Your deposited funds are FDIC insured up to $250,000 per depositor per institution.

Mercury offers checking and savings accounts, ACH and wire transfers, a Visa debit card, and integrations with QuickBooks, Xero, Stripe, and other standard business tools. It does not charge monthly fees for standard accounts. Its online dashboard is clean and designed for founders who are managing their own finances rather than delegating to a bookkeeper.

Mercury's main limitation is that it is a fintech platform rather than a full-service bank, which means it does not offer loans, lines of credit, or the full range of services that a traditional bank relationship provides. For most early-stage non-US founders, this is not a limitation that matters in the near term.

Relay

Relay is a fintech business banking platform built specifically for small businesses. Like Mercury, it offers a fully online application process and is accessible to foreign-owned entities. Relay's distinctive feature is its sub-account structure: you can create up to 20 separate checking accounts within a single business profile, which makes it useful for founders who want to manage cash allocation by category (tax reserves, payroll, operating expenses) without maintaining multiple separate bank accounts.

Relay operates through Thread Bank, which is FDIC insured. It integrates with QuickBooks, Xero, Gusto, and other standard tools. Like Mercury, it does not charge monthly fees for standard accounts and does not offer lending products.

Brex

Brex is primarily a corporate card and spend management platform that has expanded into business banking. Its cash management account is not a traditional bank account and is not FDIC insured in the traditional sense; instead, deposits are swept into money market funds or FDIC-insured partner bank accounts depending on the account configuration. Brex is most valuable for founders who want integrated expense management, a corporate card with spend controls, and reimbursement workflows alongside their banking.

Brex has historically been more selective about which businesses it onboards, often preferring companies with existing revenue, investment, or a credible business plan. Early-stage pre-revenue founders sometimes find Mercury or Relay more accessible for initial account opening, with Brex added later once the business has traction.

Traditional banks

Chase, Bank of America, Wells Fargo, and other traditional US banks offer business accounts to foreign-owned entities, but the process is significantly more complex than with fintech alternatives. Most require an in-person visit to a branch in the United States to open a business account, which means you need to be physically present in the US at some point during the account opening process. The documentation requirements are more extensive, the review process is longer, and the rejection rate for foreign-owned entities is higher.

The advantages of a traditional bank account are real: full banking services including credit lines and loans, international wire capabilities, a long-established banking relationship that can be useful for future financing, and the credibility that comes with a Chase or Bank of America account name on your invoices. For founders who are physically in the US and plan to build a US presence, establishing a traditional bank relationship alongside a fintech account is worth doing. For founders managing entirely from abroad, starting with Mercury or Relay is more practical.

Practical note: Many non-US founders open a Mercury or Relay account as their primary banking platform, then add a traditional bank account later when they have a US presence or need services that fintech platforms do not offer. This staged approach is completely sensible and avoids the friction of trying to open a traditional account before you have the documents and US presence that make it straightforward.

4. In-Person vs. Remote Account Opening

One of the most practical questions a non-US founder faces is whether they need to be physically present in the United States to open a bank account. The answer depends entirely on which institution you are applying to.

Fully remote options

Mercury, Relay, Brex, and Wise Business all offer fully remote account opening. You complete the application online, upload your documents digitally, and receive your account details without visiting the US. For these platforms, there is no requirement that you ever set foot in the United States as part of the account opening process. Verification is conducted through document upload and, in some cases, video calls or third-party identity verification services.

In-person requirements at traditional banks

Chase, Bank of America, Wells Fargo, Citibank, and most other traditional US banks require in-person identity verification for business account opening. This means you or an authorized officer of the company must visit a branch in the United States with original identity documents. The branch visit must typically be at a branch that handles business accounts rather than just consumer accounts, and you may need to schedule an appointment in advance.

Some founders plan a US trip specifically to open bank accounts. If you are going to do this, call the specific branch in advance to confirm their process for foreign-owned entities, bring every document on the list above (and extras), and be prepared for the possibility that the branch officer you meet is unfamiliar with the specific requirements for foreign-owned business accounts. Asking to speak with the branch's business banking specialist rather than a general teller will save time.

Hybrid approaches

A small number of traditional banks have developed remote account opening processes for specific customer segments, particularly for venture-backed startups with investor introductions. Silicon Valley Bank (now operating under First Citizens Bank) has historically been willing to work with foreign-founded startups remotely when they come with a referral from a known VC or accelerator. If you have those connections, they are worth using. If you do not, plan for an in-person visit or start with a fintech option.

5. What to Do if you get Rejected

Rejection is common enough that it should be treated as a possible outcome to plan for, not a disaster. Banks rarely explain precisely why they rejected an application, which makes the next step less obvious. Here is a systematic approach to working through a rejection.

Ask why, even if the answer is vague

Banks are not obligated to explain their rejection decisions in detail, and many will not. But asking politely whether there is a specific documentation gap or a policy issue can sometimes produce useful information. If the bank indicates that the issue is missing documentation rather than a policy prohibition, you can address the gap and reapply.

Try a different institution in the same category

If Mercury rejects your application, try Relay. If Relay rejects it, try Wise Business. Different fintech platforms have slightly different risk models and different geographic coverage. What triggers a rejection at one institution may not trigger one at another. Similarly, if one traditional bank declines, another may not.

Address the likely cause

The most common reasons for rejection of foreign-owned entity applications are: incomplete or inconsistent documentation, a country of origin that falls into a high-risk category, a business description that is too vague or that raises questions the application does not answer, the absence of a US business address, and the absence of a credible business plan or evidence of operations. If you can identify which of these applies to your situation, address it before reapplying.

Build more substance first

If you are applying for a bank account before your business has any customers, any revenue, or any operational history, you are asking the bank to underwrite a higher-risk account with less information than they would prefer. Sometimes the most effective approach is to build some commercial substance first: get your first paying customer, register a proper website, establish a paper trail of business activity, and then reapply with a stronger application package.

Consider a referral

For traditional banks in particular, a referral from an existing business customer, an attorney, or an accountant who has a relationship with the bank can significantly improve your application's chances. Banks view referred applications with a higher degree of trust, particularly for foreign-owned entities where their normal verification channels are less effective.

6. Stripe, Wise, and Payment Processors as Complements to Banking

A US bank account and a payment processor are different things, and understanding the difference matters for how you build your financial infrastructure. Many founders conflate them, and the result is either an incomplete setup (relying on a payment processor when they actually need a bank account) or an overcomplicated one (maintaining too many platforms when fewer would serve the same purpose).

What a bank account does

A US bank account holds your money, allows you to receive and send ACH and wire transfers, provides a routing number and account number for direct payment relationships, and gives you a place to maintain operating funds. It is the foundation of your US financial infrastructure. Almost everything else connects to it.

What a payment processor does

A payment processor facilitates the movement of money from your customers to your account. It handles the mechanics of accepting credit cards, debit cards, bank transfers, and other payment methods, deducting a processing fee (typically 2.7% to 3.5% for card transactions plus a fixed per-transaction fee), and depositing the net amount into your linked bank account. Stripe is the dominant payment processor for technology companies. Square is common for point-of-sale businesses. PayPal is widely used for consumer-facing transactions.

Stripe

Stripe is the most widely used payment processing platform for non-US founders building technology businesses. It supports businesses in over 40 countries, including allowing non-US founders to operate through a US Stripe account linked to their US entity. Stripe requires a US bank account to receive payouts, an EIN, and documentation confirming the legal existence of your entity. It does not require you to be physically present in the US.

For non-US founders, Stripe's most important capability is that it allows you to accept US dollar payments from US customers, process them through your US entity, and receive the funds in your Mercury or Relay account, all without being in the US. This is one of the core practical benefits of the US entity setup that many founders build their entire payment infrastructure around.

Stripe also offers Stripe Atlas, a formation service that includes a Delaware C-Corp or Wyoming LLC, an EIN application, and Mercury bank account setup as an integrated package. For founders who want a single-vendor starting point, Stripe Atlas is a reasonable option, though the legal documents it produces are basic and you should have them reviewed by an attorney before relying on them for anything significant.

Wise Business

Wise (formerly TransferWise) offers a business account that provides local bank account details in multiple currencies, including a US routing number and account number that can receive ACH transfers. This is not a traditional bank account and does not carry FDIC insurance in the same way that a Mercury or Relay account does, but it functions like one for many practical purposes: receiving US dollar payments, holding balances, and converting and sending money internationally.

Wise's core strength is international money movement. Its exchange rates are close to mid-market (the rate you see on Google), and its fees for international transfers are typically significantly lower than traditional bank wire fees. For founders who need to move money between their US entity and foreign accounts regularly, Wise is one of the most cost-effective tools available.

Wise Business accounts are available to non-US residents and foreign-owned entities and can be opened fully remotely. They are most useful as a complement to a primary Mercury or Relay account rather than as a replacement. Use Mercury for your primary US banking and operations. Use Wise for international transfers and multi-currency management.

PayPal

PayPal's business accounts are widely used but carry higher fees than Stripe for most transaction types and are more associated with consumer marketplaces and freelance work than with B2B or SaaS transactions. For non-US founders, PayPal is most relevant if your customers specifically expect or request PayPal payment, if you are selling on platforms like eBay or Etsy that integrate with PayPal, or if you operate in markets where PayPal is the dominant digital payment method. For most technology and service businesses targeting US enterprise or SMB customers, Stripe will be more appropriate.

Setting up Stripe for a foreign-owned US entity

The Stripe account setup process for a foreign-owned US entity requires the following:

• A valid email address for the business

• Your US entity's EIN

• Your US entity's legal name and formation state

• A US business address (your virtual office address is acceptable)

• Your personal information as the account representative: name, date of birth, and address

• A copy of your government-issued ID for identity verification

• Your US bank account details (routing number and account number) for payouts

Stripe reviews new accounts before activating full processing capabilities. During the review period, you can accept payments but payouts may be held. The review typically completes within a few days for straightforward applications, but can take longer for accounts with unusual transaction patterns or incomplete documentation.

7. Receiving USD Payments Without a US Bank Account

There is a period for some founders between forming the US entity and successfully opening a US bank account. During this period, you may have customers ready to pay you but no US account to receive payment to. This is a solvable problem, though the solutions have limitations.

Wise Business as an interim solution

A Wise Business account provides a US routing number and account number that can receive ACH payments from US customers. While Wise is not a traditional bank, it is a legitimate and widely accepted way to receive US dollar payments. Many founders use a Wise account as their primary USD receiving account while their Mercury application is under review, then switch their customers to the Mercury account once it is active.

Stripe with international payouts

Stripe supports payouts to non-US bank accounts in certain currencies and countries. If you are using Stripe to collect payments from US customers, you can configure payouts to go to a foreign bank account in your home country rather than a US account. Stripe converts the USD to your local currency at its exchange rate and transfers to your foreign account. This is less efficient than having a US account because of currency conversion costs, but it is functional as an interim arrangement.

Invoicing in USD via international wire

For B2B customers paying larger amounts, you can invoice in USD and request payment via international wire to a foreign USD account. Many international banks, particularly in the UK, EU, Canada, and Australia, offer USD-denominated accounts or correspondent banking arrangements that allow you to receive USD wires and hold them without immediate conversion. This works well for consulting or service businesses with fewer, larger invoices but is impractical for high-volume consumer or subscription transactions.

Watch out: Collecting money in your personal foreign bank account for a US business entity creates legal and tax complications. Revenue earned by the US entity should flow through the US entity's accounts, not through your personal accounts. Mixing the two undermines the separation between you and the entity and creates bookkeeping problems that are expensive to untangle.

8. Multi-Currency Accounts, FX, and Moving Money Home

If you are a non-US founder running a US business, you will at some point need to move money from your US entity to your personal accounts in your home country. The mechanics of this involve currency exchange, international wire transfers, and potentially significant costs if you do not manage the process deliberately.

The FX problem

When you move money from a USD account to a foreign currency account, the conversion happens at whatever exchange rate your bank or platform applies, minus its spread. Traditional bank wire transfers typically apply exchange rates that are 2% to 4% worse than the mid-market rate, plus fixed wire fees of $20 to $50 per transfer. On a $10,000 transfer, this can mean $200 to $450 in costs. On regular monthly transfers, this adds up to thousands of dollars per year.

Lower-cost alternatives

Wise is consistently one of the most cost-effective options for international money movement, charging fees typically in the range of 0.4% to 1.5% depending on the currency pair and amount, at exchange rates very close to mid-market. For regular transfers from your US account to a foreign account, routing through Wise rather than through a traditional bank wire can save a meaningful amount over time.

Other platforms worth evaluating for international money movement include OFX, for larger transfers where its fee structure is competitive; Airwallex, which offers multi-currency accounts and competitive FX for businesses operating across multiple currencies; and your existing home country bank, which may offer competitive USD wire receiving rates if you have a USD-denominated account there.

Tax implications of moving money home

Moving money from your US entity to your personal accounts is not a neutral act from a tax perspective. How it is taxed in both the US and your home country depends on the legal form of the transfer: salary, distribution, dividend, or management fee. The specific treatment is covered in detail in Part 7. The key point at this stage is that the banking mechanics of moving money and the tax treatment of moving money are separate questions, and you need clarity on both before you establish a regular transfer pattern.

Currency timing

For founders with significant USD-to-home-currency exposure, the timing of conversions can matter. Exchange rates move, sometimes significantly, and converting a large amount at an unfavorable rate can be materially more expensive than converting the same amount a few weeks earlier or later. Most founders at the early stage are not hedging their currency exposure formally, but being aware of the rate environment and avoiding large conversions during periods of known volatility (major economic announcements, political events) is straightforward good practice.

9. Setting Up Payment Processing: Stripe, Square, and PayPal

Payment processing is how money gets from your customers into your US bank account. The right setup depends on your business model: how your customers pay, in what amounts, at what frequency, and through which channels.

Stripe: the default for online businesses

For any founder building a software product, a subscription service, a digital marketplace, or a professional services business that invoices clients online, Stripe is the standard starting point. Its API is the most developer-friendly of the major processors, its dashboard is clear and useful for non-technical founders, it handles subscriptions and recurring billing natively, and it integrates with virtually every accounting, CRM, and operational tool you are likely to use.

Stripe's standard pricing for US-based processing is 2.9% plus $0.30 per successful card transaction. Volume discounts are available at higher transaction volumes. ACH direct debit processing is cheaper: 0.8% per transaction, capped at $5.00. For B2B businesses with larger average transaction values, routing customers through ACH where possible reduces processing costs meaningfully.

Square: for businesses with physical transactions

Square is optimized for businesses that accept payments in person: retail, food and beverage, personal services, and similar. Its point-of-sale hardware integrates with its payment processing, inventory management, and reporting tools. For non-US founders building businesses that have a physical US retail or service component, Square is worth evaluating. For fully online businesses, Stripe is almost always the better choice.

PayPal: for specific use cases

PayPal's business accounts are widely used and widely recognized, but its fees are generally higher than Stripe's for card processing (typically 3.49% plus $0.49 per transaction for standard card payments) and its experience for B2B invoicing and subscription management is less polished. PayPal's main advantages are brand recognition with consumers who feel more comfortable paying via PayPal than entering card details directly, and strong integration with marketplace platforms. If a meaningful portion of your customers specifically request PayPal, offer it. If not, Stripe is cleaner.

Tax reporting obligations for payment processors: Form 1099-K

US payment processors are required to report transaction volumes to the IRS under certain thresholds. Form 1099-K is issued by payment processors to both the merchant (you) and the IRS when your account exceeds the applicable reporting threshold. The threshold has been subject to legislative change and IRS guidance in recent years, so confirming the current threshold with your tax advisor each year is important. As of February 2026, as of the IRS news release on the “One, Big, Beautiful Bill,” the 1099-K dollar limit is described as reverting to $20,000 (per IRS). Be aware that 1099-K reporting affects how your US income needs to be reconciled in your tax filings, even though the form itself does not create additional tax due beyond what your actual income would generate.

10. Business Credit Cards for Non-US Founders

Access to US business credit is one of the more frustrating aspects of being a foreign-owned entity. US business credit cards typically require either a personal Social Security Number or a strong established US business credit history, and most non-US founders have neither at the start. Here is what is actually accessible.

Secured and deposit-backed cards

Several platforms offer business cards backed by a security deposit or account balance rather than a credit check. Brex offers a corporate card that it extends based on the company's financial profile (cash balance, funding, revenue) rather than the founder's personal credit score. For VC-backed companies, Brex is often willing to extend meaningful credit limits. For pre-revenue or bootstrapped companies, the limit is tied to the cash balance in the connected account.

Mercury also offers a business credit card (Mercury IO) that is charge-card style for Mercury account holders, with credit limits based on account balances. This is accessible to foreign founders who have established a Mercury account.

Ramp

Ramp is a corporate card and expense management platform similar to Brex. It extends credit based on the company's financial profile rather than personal credit and is available to foreign-owned US entities. Ramp's strength is its expense management and accounting integration features, making it useful for companies that want automated receipt capture, category-based spend controls, and direct sync to QuickBooks or Xero.

Personal cards as a temporary bridge

In the early stage, many founders use a personal credit card from their home country for US business expenses, then reimburse themselves from the US entity. This is acceptable as a short-term practice if the expenses are documented, properly recorded in the company's books, and the reimbursement is handled through a formal expense report. It creates bookkeeping complexity if extended, and it means you are not building US business credit history, so it should be treated as a bridge rather than a permanent arrangement.

Building US business credit over time

US business credit is built through a combination of having a DUNS number (issued by Dun and Bradstreet), establishing trade credit with US vendors who report to business credit bureaus, and maintaining a consistent banking relationship. This is a slow process but starts from day one if you are intentional about it. Ask your vendors whether they report to business credit bureaus. Pay all business obligations on time. Keep your business banking and bookkeeping current. Over 12 to 24 months, a consistent business credit profile will open more credit options than are available at the start.

11. Banking Setup Checklist

Use the following checklist to confirm your US banking infrastructure is complete before moving on.

• Primary US bank account opened (Mercury, Relay, or traditional bank)

• EIN confirmed and linked to the bank account

• US business address confirmed with the bank

• Debit card received and activated

• Online banking access confirmed

• Stripe account set up and connected to your US bank account (if applicable)

• Wise Business account set up for international transfers (if applicable)

• Business credit card or Brex/Ramp account set up (if needed)

• Bookkeeping software connected to your US bank account

• US bank account details communicated to your US accountant

• Any foreign bank accounts that will interact with the US entity identified for your home country accountant

Before you move to Part 5

Part 5 covers US federal tax in detail: how the US tax system works for non-US founders, the distinction between resident and non-resident taxation, the forms you are required to file, withholding obligations, tax treaties, and the specific rules that apply depending on whether your entity is an LLC or a C-Corp.

Before you move on, confirm the following from this part are addressed:

• Your primary US bank account is open or an application is in progress

• You have a clear plan for your payment processing setup

• You understand how you will move money from your US entity to your personal accounts and what that costs

• You have not been mixing personal and business funds through personal accounts

• Your bookkeeping software is connected or ready to connect to your banking

Antravia Advisory: Banking friction is one of the most common places where non-US founders get stuck and lose momentum. If you are having difficulty opening a US account or want guidance on structuring your US financial infrastructure, we can help you work through it.

Continue to Part 5: US Federal Tax

About Antravia Advisory

Antravia Advisory is a US-based tax and accounting advisory firm headquartered in Winter Park, Florida, operating nationally and internationally.

We advise international businesses entering the United States and complex US companies operating across multiple states, entities, and revenue structures. Our work spans advanced tax strategy, multi-state sales tax oversight, cross-border structuring, and high-level accounting architecture for e-commerce brands, subscription and SaaS businesses, platform-based models, and multi-entity groups.

We work with founders and leadership teams who require technical precision, structural clarity, and financial frameworks built for scale, capital events, and long-term resilience.

The Non-US Founder’s Complete Guide to Running a US Business

Part 1 — Before You Start

Part 2 — Choosing Your US Entity

Part 3 — Formation

Part 4 — US Banking

Part 5 — US Federal Tax

Part 6 — US State Tax

Part 7 — Paying Yourself

Part 8 — Accounting and Bookkeeping

Part 9 — Annual Compliance Calendar

Part 10 — Hiring in the US

Part 11 — Intellectual Property and Contracts

Part 12 — Your Home Country Obligations

Part 13 — Applied Business Types

Part 14 — Exiting, Winding Down, or Restructuring

Disclaimer:

Content published by Antravia is provided for informational purposes only and reflects research, industry analysis, and our professional perspective. It does not constitute legal, tax, or accounting advice. Regulations vary by jurisdiction, and individual circumstances differ. Readers should seek advice from a qualified professional before making decisions that could affect their business.

See also our Disclaimer page

Antravia Advisory

Accounting built for complexity

Not legal advice, always verify with your Accountant

Email:

Contact us:

© 2025. All rights reserved. | Disclaimer | Privacy Policy | Terms of Use |

contact@antravia.com

Antravia LLC

941 W Morse Blvd suite 100

Winter Park

Florida

32789