Selling UK Property After Moving to the U.S.: Capital Gains and Timing Risks

Selling UK property after becoming a U.S. tax resident can trigger unexpected U.S. capital gains tax. Understand timing risks, FX effects, and double-tax exposure before selling.

UK CITIZENS IN THE US

2/2/20267 min read

Selling UK Property After Moving to the U.S.: Capital Gains and Timing Risks

Relocating from the United Kingdom to the United States is a leap that often involves the most significant asset in a person’s portfolio: the family home. For many British citizens, the plan is simple... move to the U.S., rent out the UK property for a few years to see if the move "sticks," and then sell it later to fund a down payment on an American home.

On the surface, this seems like a logical financial progression. However, from a tax perspective, it is a minefield. The transition from being a UK tax resident to a U.S. tax resident creates a fundamental mismatch between how each country views the sale of real estate. Without a deep understanding of the timing risks, currency "phantom gains," and the loss of UK exemptions, a British expat can easily see 20% to 30% of their home equity eroded by the Internal Revenue Service (IRS).

At Antravia Advisory, we guide international professionals through these transitions. This guide explores why the timing of your property sale is the most critical decision you will make during your relocation.

1. The mismatch: UK PPR vs. U.S. Section 121

In the United Kingdom, the tax system is remarkably generous toward homeowners. Under Private Residence Relief (PRR), you generally pay zero Capital Gains Tax (CGT) when you sell your main home. Even if you move out, the UK grants you a final period of exemption (currently 9 months) and potentially other reliefs if you were working abroad.

The United States has a similar concept, known as the Section 121 Exclusion, but it is far more restrictive.

The $250,000/$500,000 Cap

The IRS allows an individual to exclude up to $250,000 of gain from the sale of their primary residence. If you are married and filing a joint return, that exclusion increases to $500,000.

The Problem: In high-value markets like London, the South East, or Edinburgh, it is common for a long-held family home to have appreciated by significantly more than $500,000 (roughly £390,000 at current rates).

The Consequence: If you sell that home while you are a U.S. tax resident, every dollar of gain above that threshold is subject to U.S. Federal Capital Gains Tax (usually 15% or 20%) plus the 3.8% Net Investment Income Tax (NIIT) and potentially state-level taxes.

The "Two-Out-of-Five" Year Rule

To qualify for the U.S. exclusion at all, you must have owned and lived in the property as your main residence for at least two out of the five years leading up to the date of sale.

If you move to the U.S. and rent out your UK home for more than three years, you may lose the Section 121 exclusion entirely (call us to confirm as this is dependent). Suddenly, the entire gain from the day you bought the house and not just the gain since you moved to the U.S., becomes taxable in America.

2. The cost basis trap: No step-up upon arrival

One of the most dangerous assumptions made by UK citizens is that the U.S. only cares about the value of the house from the day they arrived in the country. This is a myth. The U.S. does not provide a step-up in basis for assets when you become a resident.

Example: You bought a house in Surrey in 2010 for £400,000. When you move to the U.S. in 2026, the house is worth £900,000. If you sell it in 2027 while living in the U.S., the IRS calculates your gain based on the original 2010 purchase price of £400,000.

Because the IRS looks back to the original purchase date, you are effectively being taxed by the U.S. on growth that occurred while you were purely a UK citizen with no connection to the United States. This "retroactive" reach of the IRS is often the biggest shock for departing UK citizens.

3. FX effects: The phantom currency gain

Even if your property value in GBP Pounds Sterling stays exactly the same, you could still owe thousands of dollars in U.S. tax due to currency fluctuations. The IRS requires all transactions to be calculated in U.S. Dollars (USD) based on the exchange rates at the time of the event.

The Purchase vs. Sale

The IRS looks at two distinct points in time:

The Purchase: What was the USD value of the £400,000 you paid in 2010?

The Sale: What is the USD value of the £900,000 you receive in 2027?

If the Pound was weak when you bought and strong when you sold, your "gain" in USD terms will be significantly larger than your gain in GBP. This is known as a phantom gain. You are essentially paying tax on the fact that the British Pound gained strength against the Dollar, regardless of the actual real estate market performance.

4. Mortgage discharge: A separate taxable event

This is perhaps the most "hidden" risk of all. In the U.S., a mortgage is considered a separate liability from the property it secures. When you pay off a mortgage (usually upon the sale of the house), the IRS views it as a "repayment of debt."

If you took out a £300,000 mortgage when the exchange rate was $1.60/£1, your debt was $480,000. If, by the time you sell the house and pay off the mortgage, the exchange rate is $1.30/£1, it only costs you $390,000 to "buy" the Pounds needed to pay back the bank.

The IRS Result: You may have made a "profit" of $90,000 on the repayment of your debt.

The Tax: This is treated as Ordinary Income, taxed at your highest marginal rate (up to 37%). You cannot use the Section 121 primary residence exclusion to offset this mortgage gain.

5. Why timing the sale matters

Given these complexities, the window of opportunity to sell your UK property is much smaller than most people realize.

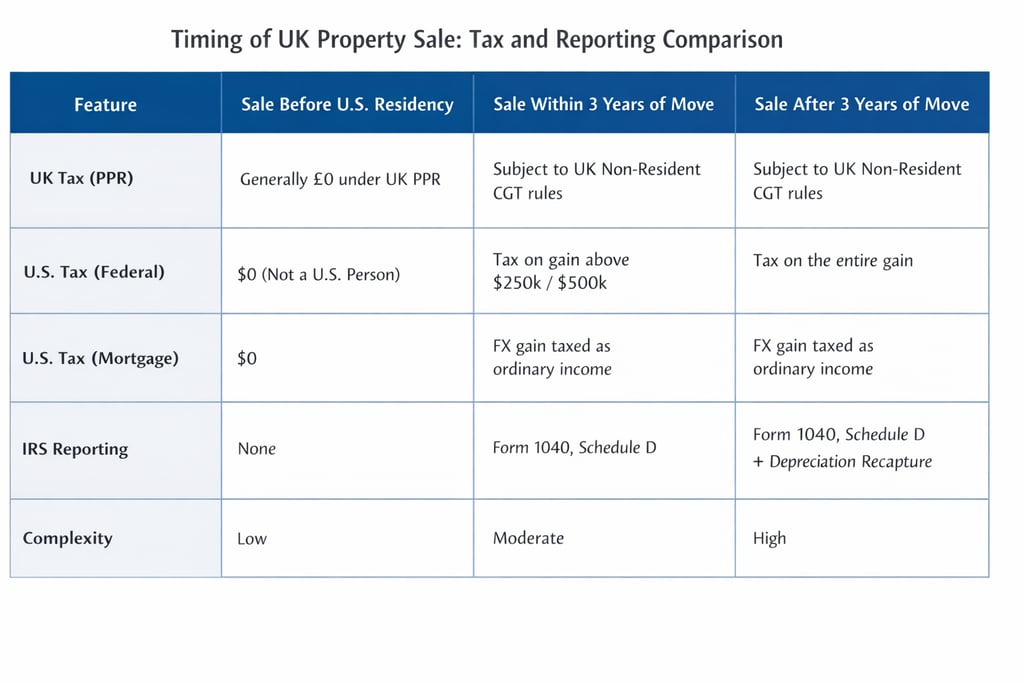

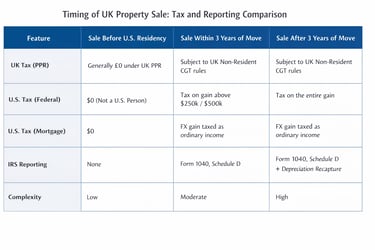

Selling Before Arrival (The Clean Break)

If you sell your home while you are still a UK resident and before you satisfy the Substantial Presence Test in the U.S., the transaction remains entirely outside the U.S. tax net.

Pros: Full UK PRR applies; zero U.S. tax; zero FBAR/FATCA reporting for that asset; no currency gain issues.

Cons: You must find a place to live in the interim and may miss out on future UK property growth.

Selling within the first 3 Years

If you sell within three years of moving, you may still qualify for the U.S. Section 121 exclusion (meeting the 2-out-of-5-year rule).

Pros: You can exclude up to $500,000 of the gain.

Cons: You are still subject to the "mortgage discharge" currency gain and must report the sale on a U.S. tax return.

The "Rental" Trap

If you decide to rent out your UK home, you are now a "foreign landlord" in the eyes of the IRS.

Depreciation: You must depreciate the property for U.S. tax purposes. When you eventually sell, you must "recapture" that depreciation at a 25% tax rate.

Reporting: You must file Schedule E with your 1040, reporting all UK rental income and expenses in USD.

Loss of Exclusion: If you rent for more than 3 years, you may lose the $250k/$500k exclusion entirely.

6. The Antravia Strategy: Proactive Planning

At Antravia Advisory, we recommend that UK citizens perform a "mock sale" calculation before they move. We look at the original purchase price, current mortgage balance, and estimated market value to determine exactly what the U.S. tax bill would look like if the sale happened one, three, or five years after arrival.

Key Actions to Take:

Obtain Valuations: Get a formal valuation of your property on the date you leave the UK. While the U.S. doesn't give you a step-up, this documentation is vital for other planning.

Review the Mortgage: If you have a large mortgage and the currency has shifted significantly, consider paying down the mortgage before becoming a U.S. tax resident to avoid the mortgage discharge gain.

Coordinate the Sale: If your gain is likely to exceed $500,000, the tax savings from selling before you move can be life-changing.

7. Summary: Selling Post-Move vs. Pre-Move

Conclusion

Selling your UK home after moving to the U.S. is not a simple real estate transaction but it is a complex cross-border tax event. The interaction of the 2-out-of-5-year rule, the limited USD exclusion, and the hidden traps of currency gains on mortgages can turn a profitable sale into a tax nightmare.

The most important takeaway for any UK citizen is that residency triggers the clock. Once you become a U.S. person, every month you wait to sell your UK home changes the tax math. By planning the timing of your sale, so ideally before you establish substantial presence, you can protect your equity and ensure your move to the U.S. is a financial success.

Would you like us to run a "Currency Phantom Gain" projection based on your current mortgage and the historical exchange rates from when you purchased your home? Contact Us

Disclaimer: This guide is for educational purposes only. Tax laws, particularly the Section 121 exclusion and the UK/U.S. tax treaty, are subject to change. Always consult with a qualified professional at Antravia or a licensed tax attorney before proceeding.

Our UK Expats in US Series

UK Citizens Moving to the U.S.: Tax Issues to Understand Before You Arrive

ISAs and UK Investments Under U.S. Tax: What Stops Being Tax-Free

Selling UK Property After Moving to the U.S.: Capital Gains and Timing Risks

UK Pensions and U.S. Tax: What Happens to Your SIPP When You Move to America

UK Pensions and U.S. Tax: The 25% Pension Lump Sum and US Tax

US–UK Tax Treaty Explained: Dual Residency, Pensions, and Cross-Border Tax Planning for UK Expats

FBAR and FATCA for UK Expats: Reporting Your UK Accounts to the IRS

FIRPTA Explained: U.S. Tax Withholding When Foreign Owners Sell Property

U.S. Tax for Foreign Owners of Rental Property: A Guide for UK Investors

Disclaimer:

Content published by Antravia is provided for informational purposes only and reflects research, industry analysis, and our professional perspective. It does not constitute legal, tax, or accounting advice. Regulations vary by jurisdiction, and individual circumstances differ. Readers should seek advice from a qualified professional before making decisions that could affect their business.

See also our Disclaimer page

Antravia Advisory

Accounting built for complexity

Not legal advice, always verify with your Accountant

Email:

Contact us:

© 2025. All rights reserved. | Disclaimer | Privacy Policy | Terms of Use |

contact@antravia.com

Antravia LLC

941 W Morse Blvd suite 100

Winter Park

Florida

32789