1. Filing Basics: Who Files, When, and How

U.S. individual tax guide for founders, expats, investors, and complex households - Part 1 - US individual tax filing basics explained in detail: who must file, income thresholds, filing statuses, dependents, deadlines, extensions, estimated tax rules, and how to avoid penalties and common filing mistakes.

U.S. INDIVIDUAL TAX GUIDE

3/28/202617 min read

Most people who file a US federal tax return do not think carefully about the foundational decisions that shape it. They enter their income, follow the software prompts, and accept whatever number comes out. For straightforward W-2 employees with no other income and no significant assets, that approach may be adequate. For founders, investors, expats, and anyone with a financial life that extends beyond a single employer, it is not.

The structure of a US tax return is built on a series of decisions made before any income is calculated. Your filing status determines your tax brackets and your standard deduction. Whether you can claim someone as a dependent affects your household's overall position. Your identification numbers must be correct or the return cannot be processed. Your withholding and estimated payments must be sufficient or penalties accrue. And the timing of your filing and payment obligations is more nuanced than the April 15 date most people think of as the tax deadline.

This section covers those foundational decisions. It is designed for people who want to understand how a US return is actually constructed, not just how to complete one.

Who is required to File

Not every person with US income is required to file a federal tax return. The obligation to file depends on your filing status, your gross income for the year, your age, and whether you are claimed as a dependent on someone else's return. The IRS sets gross income thresholds each year above which filing is required, and these thresholds differ by filing status.

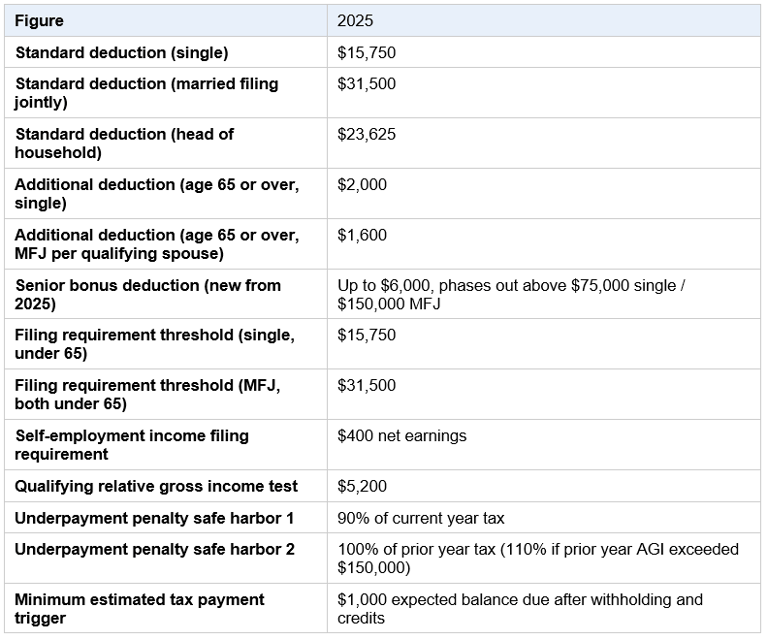

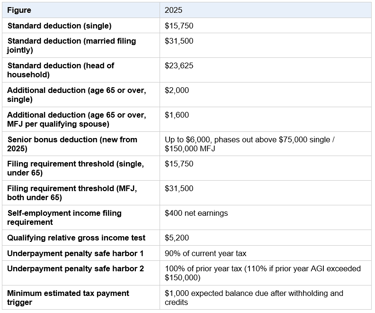

For 2025, a single filer under age 65 is required to file if gross income exceeds $15,750. A married couple filing jointly where both spouses are under 65 must file if combined gross income exceeds $31,500. A head of household filer under 65 must file if gross income exceeds $23,625. These thresholds reflect the standard deduction amounts for each filing status, which means they are adjusted annually.

Self-employment income has its own threshold. Any individual with net self-employment income of $400 or more is required to file, regardless of whether their total gross income exceeds the standard filing threshold. This is because self-employment tax, which covers Social Security and Medicare contributions for the self-employed, is calculated on net self-employment income and must be reported and paid even at relatively low income levels.

Beyond the basic income thresholds, certain situations require filing regardless of income level. These include receipt of advance premium tax credit payments, net earnings from self-employment of $400 or more, wages from a church or church-controlled organization that did not withhold Social Security and Medicare taxes, and certain situations involving household employment taxes.

Even if you are not required to file, filing may be in your interest. If federal income tax was withheld from your wages and your income is below the filing threshold, you can only recover that withholding by filing a return. Refundable credits such as the Earned Income Credit are also only available to those who file.

The Five Filing Statuses

Filing status is one of the most consequential decisions in building a US tax return. It determines your tax brackets, your standard deduction amount, your eligibility for various credits and deductions, and the income thresholds at which phaseouts begin. Choosing the wrong filing status, whether through misunderstanding or oversight, produces an incorrect return.

Single

Single filing status applies to individuals who are unmarried on the last day of the tax year and do not qualify for another filing status. Divorced or legally separated individuals are treated as single for the entire year if the divorce or separation was finalized by December 31, regardless of when during the year it occurred. Widowed individuals are generally treated as single in the year following the year of their spouse's death unless they qualify for qualifying surviving spouse status.

Single is the filing status with the narrowest tax brackets and the lowest standard deduction. An individual who qualifies for head of household status but files as single pays more tax than necessary.

Married Filing Jointly

Married filing jointly is the filing status available to legally married couples who choose to combine their income, deductions, and credits on a single return. It generally produces the most favorable tax outcome for couples where one spouse earns significantly more than the other, because the combined income is spread across the joint tax brackets, which are wider than single brackets for the lower and middle income ranges.

For a married couple to file jointly, both spouses must agree to file together and both must sign the return. A US citizen or resident alien may file jointly with a nonresident alien spouse only if both spouses elect to treat the nonresident alien as a US resident for tax purposes. That election is irrevocable without IRS consent and brings the nonresident alien spouse's worldwide income into the US tax calculation. It should not be made without careful analysis.

Married Filing Separately

Married filing separately is available to legally married individuals who choose not to file a joint return. It is almost always the least favorable filing status from a pure tax calculation standpoint. The tax brackets are identical to single brackets, the standard deduction is half the married filing jointly amount, and numerous credits and deductions are reduced or eliminated entirely for married filing separately filers.

Despite these disadvantages, married filing separately can be the correct choice in specific circumstances. It may protect one spouse from liability for the other's tax obligations. It may be required where one spouse refuses to sign a joint return. It may produce a better outcome in certain situations involving income-driven student loan repayment, where filing jointly would increase the payment obligation. And in some cases involving a nonresident alien spouse, married filing separately avoids the consequences of the joint election described above.

Head of Household

Head of household is a filing status available to unmarried individuals who pay more than half the cost of maintaining a home for a qualifying person for more than half the year. It provides wider tax brackets than single and a higher standard deduction. It is specifically designed for single parents and others who bear primary financial responsibility for a household.

The requirements are precise. The taxpayer must be unmarried or considered unmarried on the last day of the year. They must have paid more than half the cost of keeping up a home. And a qualifying person, typically a qualifying child or qualifying relative, must have lived in that home for more than half the year. Meeting these requirements is frequently misunderstood, and head of household status is one of the most commonly incorrectly claimed filing statuses on individual returns.

Qualifying Surviving Spouse

Qualifying surviving spouse status is available for the two tax years following the year of a spouse's death, provided the surviving spouse has a dependent child and continues to maintain the home as the child's principal residence. It allows the surviving spouse to use the married filing jointly tax brackets and standard deduction, which are significantly more favorable than single or head of household. After the two-year qualifying period, the surviving spouse typically moves to head of household or single status.

Dependents: Who Qualifies and why this matters

Claiming a dependent on your return is not simply a matter of declaring that someone lives in your household. The IRS applies two separate sets of tests, one for qualifying children and one for qualifying relatives, and the rules governing each are specific.

Qualifying Child

A qualifying child must meet five tests:

relationship,

age,

residency,

support, and

joint return.

The relationship test requires that the child be your son, daughter, stepchild, foster child, sibling, step-sibling, or a descendant of any of these. The age test requires that the child be under age 19 at the end of the year, or under age 24 if a full-time student, or permanently and totally disabled at any age. The residency test requires that the child have lived with you for more than half the year. The support test requires that the child have not provided more than half of their own support during the year. The joint return test requires that the child not have filed a joint return with their own spouse for the year, with an exception for returns filed solely to claim a refund.

Qualifying Relative

A qualifying relative must meet four tests: relationship or member of household, gross income, support, and not a qualifying child. The relationship test is satisfied either by a specific family relationship or by having lived with you as a member of your household for the entire year. The gross income test requires that the qualifying relative's gross income be less than $5,200 for 2025. The support test requires that you provide more than half of the person's total support for the year. And the person must not be a qualifying child of any taxpayer for that year.

Why Dependents Matter

Claiming a qualifying dependent unlocks several tax benefits. The child tax credit of $2,000-$2,200 per qualifying child under age 17 is directly tied to dependent status. The credit for other dependents of $500 applies to dependents who do not qualify for the child tax credit. The child and dependent care credit, education credits, the earned income credit, and head of household filing status all depend on having a qualifying dependent. For households with multiple dependents, getting the dependency analysis right has a meaningful effect on total tax liability.

Where two parents are divorced or separated and both could potentially claim a child as a dependent, the IRS has tiebreaker rules that determine who has the primary right to claim. Generally the parent with whom the child lived for the greater part of the year has the right. However the custodial parent may release that right to the noncustodial parent using Form 8332. This is a common source of disputes and amended returns.

Taxpayer Identification Numbers

Every individual who files a US tax return must have a taxpayer identification number. There are three types relevant to individual filers.

Social Security Number

A Social Security number is issued by the Social Security Administration to US citizens, permanent residents, and certain temporary workers authorized to work in the United States. It serves as the primary taxpayer identification number for individual filers and is required on the federal tax return of every person who has one or is eligible for one.

Individual Taxpayer Identification Number

An Individual Taxpayer Identification Number, known as an ITIN, is issued by the IRS to individuals who are required to file a US tax return but are not eligible for a Social Security number. This includes nonresident aliens with US income, resident aliens who cannot obtain a Social Security number, and the foreign spouses and dependents of US citizens or resident aliens. An ITIN is obtained by filing Form W-7 with the IRS along with certified copies of identity documents. Processing typically takes six to ten weeks.

An ITIN is for tax purposes only. It does not authorize work in the United States, does not provide eligibility for Social Security benefits, and is not the same as a Social Security number for any purpose other than tax filing.

Employer Identification Number

An Employer Identification Number is issued to businesses and entities rather than individuals. An individual who operates a sole proprietorship, is a partner in a partnership, or has household employees may need an EIN. For most individual filers who are employees or straightforward self-employed persons, a Social Security number is sufficient.

Errors in taxpayer identification numbers on a return cause it to be rejected or significantly delayed. For international filers in particular, verifying that the correct number is used and that it exactly matches IRS records is worth checking before filing. A mismatch between the name and identification number on file with the IRS and the name and number on the return is one of the most common processing errors.

Filing Deadlines and Extensions

The US federal tax year runs from January 1 to December 31. The deadline for filing individual returns is April 15 of the following year. When April 15 falls on a Saturday, Sunday, or legal holiday, the deadline moves to the next business day.

The Extension: What it does but does not do

An automatic six-month extension of time to file is available to all individual taxpayers by filing Form 4868 by April 15. The extension moves the filing deadline to October 15. No explanation or justification is required. The IRS does not approve or deny extension requests. Filing Form 4868 by April 15 automatically grants the extension.

The extension extends the time to file the return. It does not extend the time to pay any tax that is owed. This is one of the most consequential and most commonly misunderstood aspects of the extension. If you owe federal income tax for the year, the IRS expects that tax to be paid by April 15 regardless of whether an extension has been filed.

If tax is owed and not paid by April 15, the failure-to-pay penalty begins accruing at 0.5% per month on the outstanding balance, plus interest at the federal short-term rate plus three percentage points. Filing the extension while leaving the balance unpaid does reduce the failure-to-file penalty, which would otherwise run at 5% per month, but it does not eliminate the failure-to-pay penalty on the unpaid amount.

The correct approach when filing an extension is to estimate the tax owed as accurately as possible and pay that estimated amount with the Form 4868 filing. If the estimate is higher than the actual liability, the overpayment is refunded when the return is filed. There is no penalty for overpaying.

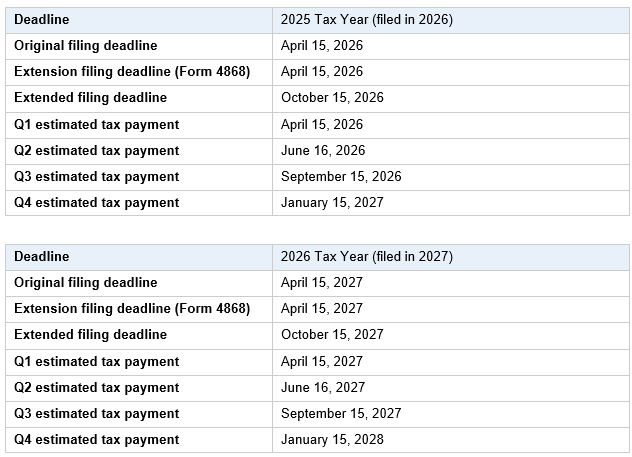

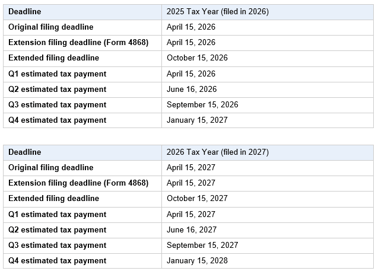

2025 and 2026 Key Dates

Special Deadlines for Taxpayers Outside the United States

US citizens and resident aliens who live outside the United States and Puerto Rico on April 15, and whose main place of business or post of duty is outside the United States and Puerto Rico, are granted an automatic two-month extension to June 15 without filing Form 4868. This extension covers both filing and payment, unlike the standard October 15 extension which covers only filing. Interest on any tax owed still accrues from April 15 even under this two-month extension.

An additional extension to October 15 is available by filing Form 4868 by June 15.

Estimated Tax Payments

The United States operates a pay-as-you-go tax system. Tax is expected to be paid throughout the year as income is earned, not in a single payment at the filing deadline. For employees, this is handled automatically through withholding from wages. For self-employed individuals, investors, and others whose income is not subject to withholding, this is handled through quarterly estimated tax payments.

Who pays Estimated Tax

You are generally required to make estimated tax payments if you expect to owe at least $1,000 in federal tax after subtracting withholding and refundable credits, and if your withholding and refundable credits will cover less than 90% of the tax shown on your current year return or less than 100% of the tax shown on your prior year return, whichever is smaller. The 100% of prior year tax threshold rises to 110% for taxpayers whose prior year adjusted gross income exceeded $150,000.

Failing to pay sufficient estimated tax during the year results in an underpayment penalty, calculated separately for each quarter based on the shortfall for that period. The penalty applies even if a refund is ultimately due on the annual return.

The Safe Harbors

The two safe harbors that protect against the underpayment penalty are worth understanding precisely. The first safe harbor is met if withholding and estimated payments cover at least 90% of the current year tax liability. The second safe harbor is met if withholding and estimated payments cover at least 100% of the prior year tax liability, rising to 110% for higher-income taxpayers. Meeting either safe harbor eliminates the underpayment penalty regardless of how much tax is ultimately owed.

For founders, freelancers, and investors whose income fluctuates significantly from year to year, the prior year safe harbor is often the more practical target. Paying 100% or 110% of the prior year tax liability through estimated payments ensures no underpayment penalty regardless of current year income, while allowing the final balance to be settled at filing.

How to Pay Estimated Tax

Estimated tax payments are made in four installments covering the dates shown in the table above. Payments can be made online through the IRS Direct Pay system at irs.gov, through the Electronic Federal Tax Payment System, by check payable to the United States Treasury accompanied by Form 1040-ES, or through certain third-party payment processors. The IRS Direct Pay and EFTPS options are free. Third-party processors charge a fee.

Withholding: The Other Side of the Pay-As-You-Go System

For employees, tax is withheld from each paycheck and remitted directly to the IRS by the employer. The amount withheld is based on the information provided on Form W-4, Employee's Withholding Certificate. Getting withholding right is important. Too little withholding results in a balance due at filing and potentially an underpayment penalty. Too much withholding results in a refund that represents an interest-free loan to the federal government.

Form W-4 and how Withholding is Calculated

Form W-4 was significantly redesigned starting in 2020. The current version asks for information about multiple jobs, additional income not subject to withholding, deductions expected to exceed the standard deduction, and additional withholding amounts per pay period. The IRS provides a withholding estimator at irs.gov/W4App that allows employees to calculate the correct withholding based on their full financial picture.

For employees with straightforward situations, the standard W-4 election produces reasonably accurate withholding. For employees with investment income, self-employment income on the side, significant deductions, or household situations that affect their tax position, a more careful W-4 calculation is warranted.

Adjusting Withholding during the Year

A new Form W-4 can be submitted to an employer at any time during the year to adjust withholding. This is appropriate whenever a significant life change affects tax liability. Marriage, divorce, the birth of a child, a substantial change in investment income, or the start of self-employment activity can all require a withholding adjustment. Changes submitted during the year take effect in the next payroll cycle.

Refunds, Balances Due, and Amended Returns

Refunds

A refund arises when total payments through withholding and estimated tax exceed the actual tax liability for the year. Refunds are processed by the IRS after the return is filed. The IRS typically issues refunds within 21 days for electronically filed returns with direct deposit elected. Paper returns and returns requiring manual review take significantly longer.

A refund is not a bonus. It represents an overpayment of tax that the government is returning. For taxpayers who consistently receive large refunds, adjusting withholding or estimated payments to better match actual liability produces the same annual tax outcome but avoids the interest-free loan to the government.

Balances Due

A balance due arises when total payments are less than the actual tax liability. The balance must be paid by April 15 regardless of whether a filing extension has been requested. Payment can be made by direct bank transfer through IRS Direct Pay, by credit or debit card through an approved processor, by check, or through an installment agreement if full payment is not possible by the deadline.

Where full payment is not possible, filing the return on time and paying as much as possible is always better than not filing. The failure-to-file penalty of 5% per month is significantly more expensive than the failure-to-pay penalty of 0.5% per month. Filing the return and setting up a payment arrangement stops the failure-to-file penalty from accruing.

Amended Returns

Errors on a filed return are corrected by filing Form 1040-X, Amended US Individual Income Tax Return. An amended return can be filed to correct income, deductions, credits, or filing status. The deadline for filing an amended return to claim a refund is the later of three years from the original filing deadline or two years from the date tax was paid.

Amended returns cannot be filed electronically in all cases, though the IRS has expanded e-filing options for amended returns in recent years. Processing time for amended returns is typically sixteen weeks, significantly longer than for original returns.

Filing an amended return does not restart the audit statute of limitations. The IRS generally has three years from the filing date of the original return to examine it. An amendment does not extend that period unless the amendment itself shows a substantial omission of income, in which case the six-year statute of limitations may apply.

Recordkeeping

Accurate recordkeeping is not optional. It is the foundation of a defensible tax return. The IRS may examine any return within the applicable statute of limitations, typically three years from filing, and the burden of proof for deductions and credits claimed on a return rests with the taxpayer. Without adequate records, a legitimate deduction becomes indefensible.

How Long to Keep Records

The general rule is to keep records for at least three years from the date the return was filed or the due date of the return, whichever is later. This covers the standard three-year examination period. Where income has been substantially omitted from a return, the IRS has six years to examine. There is no statute of limitations for fraudulent returns or for returns that were never filed.

Records related to property should be kept for as long as you own the property plus the standard retention period, because cost basis information is needed to calculate gain or loss on sale. Records related to retirement accounts should be kept indefinitely, as the basis in after-tax contributions must be traceable over the life of the account.

What Records to Keep

For income: W-2 forms from employers, 1099 forms for investment income, freelance income, and retirement distributions, brokerage statements showing transaction details, and records of any income not captured on an information return.

For deductions: receipts for charitable contributions, mortgage interest statements on Form 1098, property tax records, medical expense receipts, business expense records including mileage logs, and documentation for any deduction claimed on the return.

For investments: purchase confirmations, cost basis records, records of stock splits and dividends reinvested, and sale confirmations. Where an employer has provided equity compensation, the Form 3921 for incentive stock options and Form 3922 for employee stock purchase plans are essential for calculating basis correctly.

For cross-border taxpayers: records of foreign taxes paid, foreign income received by category and jurisdiction, and documentation supporting treaty positions claimed on Form 8833. These records should be maintained in both the original currency and the US dollar equivalent at the applicable exchange rate.

The Difference Between Filing a Return and Filing it Correctly

The IRS receives hundreds of millions of tax returns each year. Most of them are processed automatically. The vast majority of errors in individual returns are never detected. But undetected errors are not the same as no errors. An incorrect return that survives IRS processing may have understated a liability that remains legally owed, overstated a refund that may be clawed back in an examination, or established an incorrect position that compounds into larger errors in subsequent years.

The most common errors in individual returns are not mathematical. Tax software handles arithmetic reliably. The most common errors are analytical. They arise from misclassifying income, missing deductions that exist but require knowledge to find, claiming deductions or credits for which the taxpayer does not actually qualify, choosing the wrong filing status, and failing to coordinate between different parts of a complex return so that the pieces fit together correctly.

For taxpayers with business income, investment portfolios, retirement accounts in multiple vehicles, cross-border income, or equity compensation, the interactions between these elements require judgment that software alone cannot supply. The software will produce a number. Whether that number is correct depends on the quality of the analysis behind it.

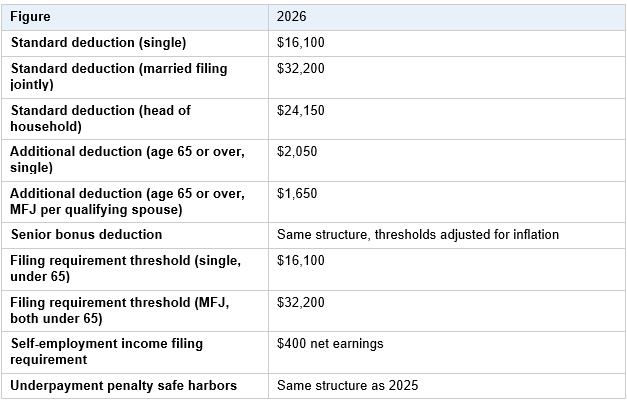

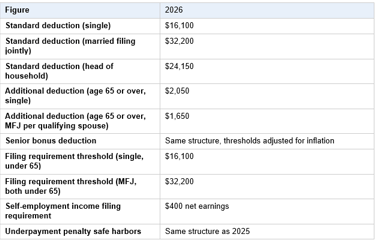

Key Figures: 2025 and 2026

About Antravia Advisory

Antravia Advisory is a cross-border tax and advisory firm working with individuals whose tax positions are not straightforward. We support founders, investors, expats, and internationally mobile households who need more than basic tax preparation.

We advise on US individual tax, international reporting, and the interaction between multiple tax systems, including situations involving foreign income, overseas assets, and dual-country obligations. This includes expats living in the United States, US persons living abroad, and families managing financial lives across jurisdictions.

Our work goes beyond filing. We focus on structuring, planning, and ensuring that positions are technically correct, defensible, and aligned across years.

U.S. individual tax guide for founders, expats, investors, and complex households

Part 1 Filing Basics: Who Files, When, and How

Part 2 Wages, Interest, Dividends, and Ordinary Income

Part 3 Self-Employment and Freelance Income

Part 4 Investment Income, Capital Gains, and Property Transactions

Part 5 Retirement Income and Social Security

Part 6 Adjustments to Income

Part 7 Standard Deduction and Itemized Deductions

Part 8 Tax Credits

Part 9 Tax Payments, Penalties, Refunds, and Amended Returns

Part 10 Cross-Border and Complex Individual Issues

Disclaimer:

Content published by Antravia is provided for informational purposes only and reflects research, industry analysis, and our professional perspective. It does not constitute legal, tax, or accounting advice. Regulations vary by jurisdiction, and individual circumstances differ. Readers should seek advice from a qualified professional before making decisions that could affect their business.

See also our Disclaimer page

Antravia Advisory

Accounting built for complexity

Not legal advice, always verify with your Accountant

Email:

Contact us:

© 2025. All rights reserved. | Disclaimer | Privacy Policy | Terms of Use |

contact@antravia.com

Antravia LLC

941 W Morse Blvd suite 100

Winter Park

Florida

32789