Foreign-Owned Multi-Member LLC Tax Guide: Form 1065, Section 1446 and What Changes When You Add a Second Member

Adding a second member to a foreign-owned US LLC eliminates Form 5472 entirely and triggers a completely different compliance framework: Form 1065, Schedule K-1 for every partner, and Section 1446 withholding on each foreign partner's share of income whether or not any cash is distributed. This guide covers every ownership scenario, every required form, filing deadlines, withholding rates, FIRPTA, the Form 8832 election, and how to fix prior-year errors before the IRS finds them first.

THE NON-US FOUNDER'S COMPLETE GUIDE TO RUNNING A US BUSINESS

3/18/202617 min read

Adding One Person Changes Everything

The Complete US Tax Guide for Foreign-Owned Multi-Member LLCs

A foreign person forms a US LLC, gets their compliance right, files their Form 5472 correctly for a couple of years, and then adds a family member as a second member. Maybe a son, a spouse, a business partner. The interest might be 10%, it might be 1%. It seems administrative. Nobody mentions it to the accountant. The accountant files another Form 5472 pro forma return the following April because that is what they did last year.

Everything about that filing is now wrong.

The moment a second member joins an LLC, the entire US tax framework changes. The disregarded entity disappears. Form 5472 no longer applies. A completely different set of forms, obligations, and deadlines takes over. This guide explains exactly what those obligations are, covers every scenario involving foreign members, and explains what happens when the transition is missed.

Part One: Why Adding a Second Member Changes Everything

Under the US check-the-box regulations, a single-member LLC with no Form 8832 election is by default a disregarded entity, treated as a sole proprietorship or branch of its owner for US tax purposes. The Form 5472 pro forma 1120 route exists specifically for this structure.

A multi-member LLC with no Form 8832 election is by default a partnership for US tax purposes. Not a corporation, not a disregarded entity. A partnership. This default applies regardless of what the operating agreement says, regardless of how the members think of the arrangement, and regardless of whether the LLC is registered in a US state or was formed for a single passive purpose.

The partnership classification matters enormously because partnerships file Form 1065, issue Schedule K-1 to each partner, and face a completely different penalty structure. And when one or more of those partners is a foreign person, an additional layer of withholding obligations applies under Section 1446 of the Internal Revenue Code, requiring the partnership itself to withhold and remit US tax on behalf of its foreign partners.

None of this is optional and none of it is triggered by a threshold. One foreign member with a 1% interest in a two-member LLC creates the full Section 1446 withholding obligation on that 1% of effectively connected income. The percentage of foreign ownership does not reduce the compliance burden, it only affects the dollar amount of the withholding calculation.

ℹ The Critical Distinction from Form 5472

Form 5472 applies to single-member foreign-owned LLCs and to 25%-or-more foreign-owned corporations. It does not apply to partnerships. A multi-member LLC that has never made a Form 8832 election is a partnership and Form 5472 is simply irrelevant to it, regardless of how much of it is owned by foreign persons.

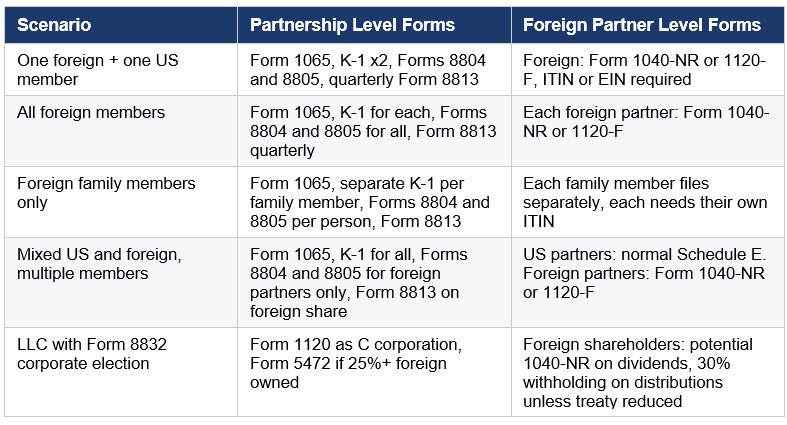

Part Two: The Four Core Scenarios

The compliance picture for a multi-member LLC with foreign involvement depends on exactly who the members are. There are four distinct scenarios, each with its own obligations and risks.

Scenario 1: One Foreign Member, One US Member

Members: One foreign person + one US person (any split)

Key Forms: Form 1065, Schedule K-1 x2, Forms 8804 and 8805 for foreign partner's share

This is the most common scenario and the one that creates the most overlooked compliance gaps. A US citizen or resident teams up with a foreign investor, a foreign family member living abroad, or a foreign business partner. The LLC is a partnership. The US member reports their K-1 income on their personal return in the normal way. The foreign member has a separate set of obligations, and the partnership itself has a withholding obligation it must discharge regardless of whether it makes any distributions.

Scenario 2: All Foreign Members

Members: Two or more foreign persons, no US members

Key Forms: Form 1065, Schedule K-1 for each, Forms 8804 and 8805 for all partners, possibly Form 1042-S

A fully foreign-owned multi-member LLC is still a US partnership and still must file Form 1065. This surprises many foreign business owners who assume that an LLC with no US members and no US-source income has no US filing obligations. That assumption is wrong as soon as the LLC has any US-source income or any effectively connected income, and the partnership return is required regardless.

Scenario 3: Family Members, All Foreign

Members: Father and son, or spouses, or siblings, all foreign persons

Key Forms: Form 1065, Schedule K-1 for each family member, Forms 8804 and 8805, possible ITIN requirements for all

The family member scenario deserves its own treatment because it is where the most casual transitions happen. A foreign parent adds an adult child to the LLC. Two foreign siblings co-own a US business. The family relationship does not create any simplification in US tax law. Each family member is a separate foreign partner with their own K-1, their own potential US filing obligation, and their own ITIN requirement. The partnership has withholding obligations on each member's allocable share of effectively connected income regardless of the family connection.

Scenario 4: Mixed Domestic and Foreign, Multiple Members

Members: Two or more US members plus one or more foreign members

Key Forms: Form 1065, Schedule K-1 for all, Forms 8804 and 8805 on foreign partners' shares only, US members file normally

When a partnership has both US and foreign members, the Section 1446 withholding obligation applies only to the foreign partners' allocable shares of effectively connected income. The US members' shares are not subject to partnership-level withholding because US members handle their own tax obligations through their personal returns. The partnership must track the two populations separately and calculate withholding only on the foreign portion.

Part Three: Form 1065, the Partnership Return

Who Must File

Every US partnership must file Form 1065 for each tax year in which it has income, deductions, or credits, or for any year in which it has two or more members even with no activity. A multi-member LLC that was formed, had no revenue, and did nothing during the year still has a Form 1065 filing obligation for that year. The inactive LLC excuse that fails under Form 5472 fails equally here.

Deadlines

Form 1065 is due on the 15th day of the third month following the close of the tax year. For a calendar year partnership that is March 15, not April 15. This catches people who are accustomed to the individual or corporate April 15 deadline. A six-month extension is available on Form 7004, pushing the deadline to September 15.

The March 15 deadline applies regardless of whether the partnership owes any tax. The partnership itself generally does not pay income tax. It files an information return, passes income and deductions through to its partners via Schedule K-1, and each partner is responsible for their own tax.

Schedule K-1 for Each Partner

Form 1065 must be accompanied by a Schedule K-1 for each partner, showing that partner's allocable share of income, deductions, credits, and other items. The K-1 must include the partner's taxpayer identification number. For US partners, that is a Social Security Number or EIN. For foreign partners, that is either an Individual Taxpayer Identification Number or a foreign EIN.

A foreign partner who does not have an ITIN must apply for one on Form W-7 before the K-1 can be properly completed. The ITIN application process can take several weeks. This is not a last-minute task.

The Late Filing Penalty

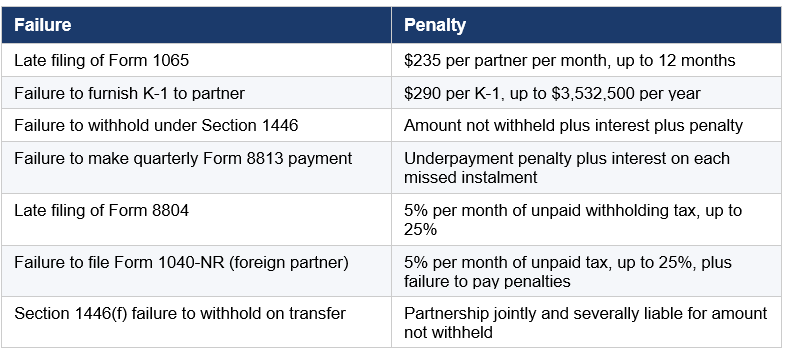

The penalty for late filing of Form 1065 is $235 per partner per month, or fraction of a month, that the return is late, up to a maximum of twelve months. A two-member LLC with a Form 1065 that is one month late faces a $470 penalty. A ten-member LLC faces $2,350 for the same one-month delay. For larger partnerships the penalty can be substantial even before any income tax issues arise.

Part Four: Section 1446 Withholding, the Obligation Most Partnerships Miss

Section 1446 is the provision of the Internal Revenue Code that creates a partnership-level withholding obligation on effectively connected income allocable to foreign partners. It is the most frequently overlooked compliance requirement for multi-member LLCs with foreign members, and the penalties for getting it wrong sit on top of the Form 1065 penalties already described.

What is Effectively Connected Income

Effectively connected income, commonly referred to as ECI, is income that is effectively connected with the conduct of a trade or business in the United States. For most operating businesses, the income the LLC generates from its US activities is effectively connected income. This includes income from providing services in the US, income from selling goods in the US, and income from US real property in most cases.

Income that is not effectively connected with a US trade or business, such as purely passive investment income like US-source dividends and interest received by a foreign partner who is not engaged in a US business, is subject to a different withholding regime under Section 1441 and is reported on Form 1042-S rather than through the Section 1446 mechanism.

The distinction matters because the withholding rates differ and the forms used differ. A partnership with foreign partners that has both ECI and non-ECI income may have obligations under both regimes simultaneously.

The Withholding Obligation

A partnership that has effectively connected taxable income for a tax year must withhold on each foreign partner's allocable share of that income, whether or not any actual distribution is made to the foreign partner. This point is critical and widely misunderstood. The withholding obligation is not triggered by a cash distribution. It is triggered by the existence of allocable effectively connected income. A foreign partner whose share of ECI sits on the books as an undistributed profit still creates a withholding obligation for the partnership in the year that income is earned.

The Withholding Rates

The applicable withholding rate depends on the character of the foreign partner and the character of the income. For a foreign partner that is a non-corporate foreign person, the rate is generally the highest individual rate applicable to that type of income. For a foreign corporate partner, the rate is the corporate rate. For tax year 2024, the rate on ordinary income for non-corporate foreign partners is 37%. For corporate foreign partners the rate is 21%.

Capital gains allocated to foreign partners are subject to withholding at the applicable capital gains rate, with long-term capital gains generally withheld at 20% for non-corporate partners.

These rates can be modified by an applicable income tax treaty between the US and the foreign partner's country of residence. However, treaty relief must be properly claimed and documented. The partnership cannot simply assume treaty relief applies without obtaining the required documentation from the foreign partner.

⚠ No Distribution Does Not Mean No Withholding

The single most common Section 1446 error is assuming that withholding is only required when cash is distributed to the foreign partner. It is not. If the partnership allocates effectively connected taxable income to a foreign partner in a given year, the partnership must withhold on that allocation whether or not any cash changes hands. A profitable LLC that retains all its earnings still owes Section 1446 withholding on the foreign partner's share.

Form 8804: The Annual Withholding Return

Form 8804 is the Annual Return for Partnership Withholding Tax Under Section 1446. It is filed by the partnership to report the total amount of withholding tax it owes for the year on behalf of all foreign partners. It is due on the same date as Form 1065, which is March 15 for a calendar year partnership, with the same six-month extension available.

Form 8804 is accompanied by a Form 8805 for each foreign partner, which functions similarly to a W-2 or 1099 in that it shows the individual foreign partner's allocable share of effectively connected income and the amount withheld. The foreign partner uses their Form 8805 to claim credit for amounts withheld when they file their own US return.

Form 8813: Quarterly Instalment Payments

The Section 1446 withholding obligation is not just an annual filing. The partnership must make quarterly instalment payments of its withholding tax liability on Form 8813. The quarterly payment dates are April 15, June 15, September 15, and December 15, or the next business day if those dates fall on a weekend or holiday. Each payment covers the withholding tax accrued in that quarter.

A partnership that discovers its Section 1446 obligation only at year end and makes a single annual payment has already missed three quarterly instalments and faces underpayment penalties on each of them. The quarterly nature of this obligation is one of the most overlooked aspects of running a partnership with foreign members.

The Penalty for Failure to Withhold

A partnership that fails to withhold under Section 1446 is liable for the amount that should have been withheld, plus interest, plus a failure-to-withhold penalty. The partnership cannot escape this liability by pointing to the fact that the foreign partner eventually paid their own US tax. The obligation sits on the partnership independently of whether the foreign partner fulfills their own filing obligations.

If the partnership can demonstrate that the foreign partner paid the tax that should have been withheld, it can seek relief from the withholding penalty under Regulations section 1.1446-3(f), but this requires affirmative demonstration and is not automatic.

Part Five: The Foreign Partner's Own US Obligations

Form 1065 and the Section 1446 withholding regime are the partnership's obligations. Separately, each foreign partner has their own US filing obligations based on their allocable share of the partnership's income.

Non-Resident Alien Individuals

A foreign partner who is a non-resident alien individual and who has effectively connected income from the partnership must file Form 1040-NR, the US Non-Resident Alien Income Tax Return. The Schedule K-1 from the partnership feeds into this return. The amount withheld by the partnership on Form 8805 is taken as a credit against the tax liability on the 1040-NR.

The Form 1040-NR is due June 15 for a calendar year non-resident alien who does not have wages subject to US withholding, or April 15 if they do. An extension is available on Form 4868.

Non-resident alien individuals must also comply with any applicable treaty provisions. If a tax treaty reduces the US tax on their allocable income, they claim the treaty benefit on the 1040-NR, but they must still file the return to claim it. A foreign partner cannot simply receive a K-1, take comfort in the Section 1446 withholding having been done, and file nothing personally. The withholding is a payment on account, not a final settlement.

Foreign Corporate Partners

A foreign corporation that is a partner in a US LLC must file Form 1120-F, the US Income Tax Return of a Foreign Corporation, if it has income effectively connected with a US trade or business. The partnership K-1 feeds into the 1120-F in the same way it feeds into the 1040-NR for individual partners. The Section 1446 withholding credit appears on the 1120-F.

Form 1120-F is due by the 15th day of the sixth month following the close of the tax year for a foreign corporation that does not maintain an office or place of business in the US, which is June 15 for a calendar year. An extension to December 15 is available.

The ITIN Requirement

Every foreign partner must have a US taxpayer identification number. For non-resident alien individuals, this is an Individual Taxpayer Identification Number obtained on Form W-7. For foreign corporations, it is a foreign EIN obtained on Form SS-4. Without a valid TIN, the partnership cannot properly complete the K-1, and the foreign partner cannot file their own US return or claim the withholding credit.

The W-7 process requires the foreign individual to submit original identity documents or certified copies, along with evidence of foreign status. Processing typically takes seven to eleven weeks. Applications can be made through an IRS Taxpayer Assistance Center, through a Certified Acceptance Agent, or by mail. For foreign individuals who have never had any US presence, the Certified Acceptance Agent route is often the most practical.

Part Six: US Real Property and FIRPTA

If the multi-member LLC holds US real property interests, the Foreign Investment in Real Property Tax Act adds another layer of complexity. Under FIRPTA, gain from the disposition of a US real property interest by a foreign person is treated as effectively connected income and is subject to withholding at the time of sale.

The Partnership as a US Real Property Holding Company

If 50% or more of the value of a partnership's assets consists of US real property interests, the partnership may be classified as a US Real Property Holding Corporation equivalent for FIRPTA purposes, which triggers additional reporting and withholding requirements on the disposition of partnership interests by foreign partners.

Withholding on Distributions Attributable to FIRPTA Gains

When a partnership that holds US real property interests makes a distribution to a foreign partner that is attributable to gain from a US real property interest, the partnership must withhold 21% of that distribution. This applies to distributions of proceeds from property sales, not just distributions of operating income.

The Section 1446(f) Withholding on Partnership Interest Transfers

Since 2018, Section 1446(f) requires a transferee who purchases a partnership interest from a foreign partner to withhold 10% of the amount realized on the transfer if the partnership is engaged in a US trade or business. If the transferee fails to withhold, the partnership itself becomes jointly and severally liable for the withholding. This provision catches many buyers of partnership interests who are unaware that they have a withholding obligation when purchasing from a foreign seller.

Part Seven: The Form 8832 Election and When It Makes Sense

A multi-member LLC does not have to accept its default partnership classification. It can elect to be treated as a corporation for US tax purposes by filing Form 8832, the Entity Classification Election. Once the election is made, the LLC files Form 1120 as a corporation, and the Section 1446 partnership withholding regime no longer applies.

What the Election Changes

If the LLC elects corporate treatment, the partnership framework disappears entirely. There are no K-1s, no Form 1065, no Section 1446 withholding. Instead, the LLC files a Form 1120 as a C corporation. If foreign persons own 25% or more of the corporation, Form 5472 becomes relevant again. The corporation is subject to US corporate income tax on its worldwide income. Distributions to foreign shareholders may be subject to dividend withholding under Section 1441.

When the Election Might Be Considered

The corporate election is not inherently better or worse than partnership treatment. It depends entirely on the specific situation. Partnership treatment offers flow-through taxation, which means income is taxed once at the partner level rather than twice at the corporate level and again when distributed. Corporate treatment eliminates the partnership compliance complexity including Section 1446 withholding but introduces corporate-level tax.

For a multi-member LLC that is purely a holding vehicle with minimal operating activity, partnership treatment is usually simpler overall despite the K-1 complexity. For an operating business with complex intercompany relationships and multiple foreign owners who want to limit their personal US filing footprint, the analysis is more nuanced.

The election is generally effective on the date specified in the form, which can be up to 75 days before the filing date or up to twelve months after. Once made, the election generally cannot be changed for 60 months without IRS consent.

⚠ The Transition Risk

If an LLC transitions from partnership to corporation via a Form 8832 election, the transition is treated as a deemed contribution of all assets and liabilities to a new corporation in exchange for stock. This deemed transaction can have significant tax consequences if the partnership has appreciated assets, built-in gains, or existing debt. The election should never be made without modelling the deemed transaction consequences first.

Part Eight: The Transition Trap

As discussed at the outset, the most dangerous moment in the lifecycle of a foreign-owned LLC is the transition from single-member to multi-member. This section covers exactly what needs to happen when that transition occurs, and what the exposure looks like if it does not.

What Must Happen When a Second Member Joins

The moment a second member is admitted to an LLC, the following applies from that date forward. The LLC is no longer a disregarded entity. Form 5472 is no longer the correct form. The LLC must obtain a new EIN if it does not already have one suitable for a partnership return. Form 1065 becomes the annual filing requirement. If the new or existing member is a foreign person, Section 1446 withholding obligations apply from the first day of the tax year in which the foreign partner is a member.

The year in which the transition occurs is a split year for compliance purposes. If the LLC was a disregarded entity for the first part of the year and a partnership for the remainder, the LLC may need to file both a pro forma 1120 with 5472 for the disregarded entity period and a Form 1065 for the partnership period, depending on the timing and the nature of the transactions in each period. This is one of the more complex compliance situations in US tax and generally requires professional guidance.

What Happens When the Transition is Missed

If the transition is missed and the LLC continues filing Form 5472 pro forma returns after becoming a multi-member partnership, the returns filed are technically wrong form filings. The partnership's Form 1065 obligation was never discharged. The Section 1446 withholding was never calculated or remitted. Foreign partners received no K-1s.

The penalty exposure in this scenario compounds across every year the error persists. The Form 1065 late filing penalty accrues per partner per month. The Section 1446 failure to withhold creates a separate liability with interest. The foreign partners' own US filing obligations were never triggered because they received no K-1s, creating potential delinquency on their 1040-NR or 1120-F returns as well.

Correcting this requires filing delinquent Form 1065 returns for all affected years, issuing corrected K-1s, calculating and remitting the Section 1446 withholding that was not made, and addressing the foreign partners' own filing delinquencies. It is a substantial remediation project and one that becomes more complex and more expensive with every additional year that passes.

Part Nine: Complete Compliance Summary by Scenario

Part Ten: Penalty Overview

Part Eleven: Practical Checklist for Multi-Member LLCs with Foreign Partners

Work through the following before each filing season and whenever the membership of the LLC changes.

1. Confirm the current membership of the LLC and whether any member is a foreign person.

2. Confirm whether a Form 8832 corporate election has been made. If yes, the corporate regime applies. If no, the partnership regime applies.

3. Obtain or verify a valid ITIN or foreign EIN for each foreign partner. Do not wait until March.

4. Calculate the partnership's effectively connected taxable income for the year and determine each foreign partner's allocable share.

5. Confirm that quarterly Section 1446 instalment payments were made on Form 8813 on April 15, June 15, September 15, and December 15 of the tax year.

6. Prepare Form 1065 and Schedule K-1 for each partner. File by March 15, or September 15 with a valid extension.

7. Prepare Form 8804 and a Form 8805 for each foreign partner. File with Form 1065.

8. Issue K-1s to all partners promptly so that foreign partners can prepare their own US returns.

9. Ensure foreign partners are aware of their own US filing obligations, Form 1040-NR or Form 1120-F, and their deadlines.

10. If any transfer of a partnership interest occurred during the year, confirm whether Section 1446(f) withholding applied.

11. If the LLC holds US real property interests, confirm whether FIRPTA withholding applied to any distributions or dispositions.

12. If a new member joined during the year, determine whether this created a split-year transition from disregarded entity to partnership and address any overlapping filing obligations.

Part Twelve: How This Connects to Form 5472

Readers who have also reviewed our Form 5472 guide here will notice that the two compliance frameworks are mutually exclusive in most cases. A single-member foreign-owned LLC uses the Form 5472 pro forma 1120 route. A multi-member LLC uses the Form 1065 partnership route. A multi-member LLC with a Form 8832 corporate election re-enters the Form 5472 world if foreign ownership reaches 25% or more.

The overlap zone, where both could theoretically seem relevant, is the transition year when a second member joins. In that year, the LLC may have both a disregarded entity period and a partnership period within the same calendar year. The Form 5472 obligation covers the disregarded entity period. The Form 1065 obligation covers the partnership period. Both forms may be required for the same LLC for the same tax year.

This is the scenario where getting professional advice early in the year of transition makes the most material difference. The filing requirements for a transition year are complex enough that trying to reconstruct them after the fact creates unnecessary risk and cost.

How Antravia Advisory Can Help

Foreign-owned multi-member LLCs sit at one of the most complex intersections in US international tax. The partnership rules, the Section 1446 withholding regime, FIRPTA, treaty analysis, and the individual filing obligations of foreign partners all interact, and a gap in any one of them creates compounding exposure.

Antravia Advisory works with foreign-owned US businesses on Form 1065 preparation and filing, Section 1446 withholding calculations and compliance, Forms 8804 and 8805 preparation, K-1 preparation for foreign partners, ITIN applications, coordination with foreign partners' own US filing obligations, remediation of prior-year non-compliance, and penalty abatement requests.

If your LLC recently added a foreign member, or if you have been filing under the wrong framework for prior years, contact us for an initial consultation. Early identification of a compliance gap is always less expensive than discovering it after the IRS does.

Disclaimer

This article is published by Antravia Advisory for general informational purposes only. It does not constitute tax advice and does not create a client relationship. US tax law is complex and fact-specific. The information in this article reflects the law as understood at the time of publication and may not reflect subsequent changes. Every taxpayer's situation is different. You should consult a qualified US tax professional before making any decisions based on the content of this article.

The Non-US Founder’s Complete Guide to Running a US Business

The Non-US Founder's Complete Guide to Running a US Business - Everything a non-US founder needs to know about setting up, operating, and scaling a US business, from choosing the right entity and opening a bank account, to tax compliance, paying yourself, hiring staff, and managing your home country obligations. Built for international entrepreneurs who want to get it right. Link

Disclaimer:

Content published by Antravia is provided for informational purposes only and reflects research, industry analysis, and our professional perspective. It does not constitute legal, tax, or accounting advice. Regulations vary by jurisdiction, and individual circumstances differ. Readers should seek advice from a qualified professional before making decisions that could affect their business.

See also our Disclaimer page

Antravia Advisory

Accounting built for complexity

Not legal advice, always verify with your Accountant

Email:

Contact us:

© 2025. All rights reserved. | Disclaimer | Privacy Policy | Terms of Use |

contact@antravia.com

Antravia LLC

941 W Morse Blvd suite 100

Winter Park

Florida

32789