Part 5: US Federal Tax

The Non-US Founder's Complete Guide to Running a US Business - Part 5 explains how U.S. tax applies to non-U.S. founders, including ECI, dual-status residency, Form 1040-NR filing, Form 5472 reporting, partnership withholding under Section 1446, and how profit extraction is taxed across borders.

THE NON-US FOUNDER'S COMPLETE GUIDE TO RUNNING A US BUSINESS

3/4/202628 min read

US federal tax is the subject that causes the most anxiety among non-US founders, and the most expensive problems when it is mishandled. It is also the area where generalist advice is most likely to fail you. The rules that apply to a non-US founder operating a US business are materially different from the rules that apply to US residents, and they interact with your home country tax obligations in ways that require both sides to be understood at once.

This part covers the US federal tax framework in full: how residency is determined, how different entity types are taxed, the specific forms you are required to file and when, withholding obligations, tax treaties, transfer pricing, and several provisions that trip up international founders who encounter them without warning. The goal is not to replace your tax advisor. It is to give you enough understanding of the framework that you can work with your advisor effectively, ask the right questions, and avoid the most common and costly mistakes.

1. How the US Tax System Works: An Overview for Non-US Founders

The United States operates a multi-layer tax system: federal taxes imposed by the Internal Revenue Service (IRS), state taxes imposed by each individual state, and in some jurisdictions local taxes imposed by cities or counties. These layers operate independently. Complying with federal tax does not mean you have complied with state tax. Part 6 covers state tax in detail. This part covers the federal layer.

The federal tax system is administered by the IRS under the authority of the Internal Revenue Code (the IRC, also referred to as Title 26 of the United States Code). The IRC is a detailed and extensive body of law, but for most non-US founders the relevant provisions cluster around a manageable set of concepts: residency, entity classification, ECI and FDAP income, withholding, and information reporting.

The federal tax calendar

The US federal tax year for individuals is the calendar year, running from January 1 through December 31. For corporations, the default is also the calendar year, though a corporation can elect a fiscal year ending on the last day of any month. Most early-stage entities default to the calendar year. The key federal tax deadlines for non-US founders are covered in the forms section later in this part and in the Annual Compliance Calendar in Part 9.

2. The Foundational Question: Are you a US Tax Resident?

Before anything else in US federal tax can be analyzed, you need to answer one question: are you a US tax resident or a non-resident alien? The answer determines which tax rules apply to you personally, which forms you file, and how your income is characterized and taxed.

This is a question about you as an individual, not about your entity. Your LLC or C-Corp has its own tax status independent of whether you personally are a US resident. But your personal residency status affects how the income from that entity is taxed in your hands.

The two tests for US tax residency

There are two ways an individual can become a US tax resident. The first is holding a green card (lawful permanent resident status). If you hold a green card, you are a US tax resident and taxed on your worldwide income, regardless of where you actually live. The second is meeting the Substantial Presence Test.

The Substantial Presence Test

The Substantial Presence Test is a mathematical formula based on the number of days you are physically present in the United States during a three-year rolling period. You meet the test, and are therefore treated as a US tax resident for that year, if you are present in the US for at least 31 days during the current calendar year AND the sum of the following is 183 days or more:

• All days present in the current year, plus

• One-third of the days present in the prior year, plus

• One-sixth of the days present in the year before that

As a practical illustration: if you were in the US for 120 days in the current year, 120 days in the prior year, and 120 days in the year before that, the calculation is 120 + (120/3) + (120/6) = 120 + 40 + 20 = 180 days. That falls below 183, so you would not meet the test in the current year. If you were in the US for 130 days in each of those three years, the calculation would be 130 + 43 + 21 = 194 days. That exceeds 183, so you would be treated as a US tax resident for the current year.

Days do not count toward the test if you are in the US as a student (F, J, M, or Q visa), as a teacher or trainee (J or Q visa), as a diplomat, or if you are unable to leave the US due to a medical condition that arose while you were there. If you are in the US under a treaty-exempt status, those days may also be excluded.

What it means to be a non-resident alien

If you do not hold a green card and do not meet the Substantial Presence Test, you are a non-resident alien (NRA) for US tax purposes. This is the status of most non-US founders at the start of their US business journey. As an NRA, you are taxed in the US only on income that has a sufficient nexus to the United States: ECI and certain categories of US-source FDAP income. You are not taxed on income from foreign sources.

The difference between being a US resident and an NRA for tax purposes is significant. A US resident is taxed on worldwide income. An NRA is taxed only on US-connected income. For most non-US founders who remain in their home countries, NRA status is appropriate and results in a more limited US tax obligation than residency status would.

Becoming a US tax resident unintentionally

One of the risks that non-US founders face is inadvertently becoming a US tax resident by spending too many days in the US. If you are traveling frequently to the US for business, attending conferences, meeting investors, and managing operations, your day count can accumulate faster than you expect. Crossing the Substantial Presence threshold converts you from an NRA to a US tax resident, with worldwide income tax consequences, for that entire calendar year.

If you are spending significant time in the US, track your days. An app or a simple spreadsheet will do. Knowing your year-to-date count gives you the information to make intentional decisions about travel rather than discovering a residency problem at tax time.

Critical: If you become a US tax resident for any part of a year, you are generally required to file a US resident tax return (Form 1040) for that year and report your worldwide income. If you are unsure whether you have met the Substantial Presence Test, consult a US tax advisor before filing.

3. Disregarded Entity Taxation: The Single-Member LLC

As covered in Part 2, a single-member LLC owned by a non-US person is treated as a disregarded entity for US federal tax purposes. The entity is invisible to the IRS for income tax purposes; its income and expenses flow directly to the owner.

For a non-resident alien owner, this means the following. If the LLC generates ECI, that income is reported on the owner's Form 1040-NR and taxed at graduated individual income tax rates, net of allowable deductions. The LLC pays no entity-level income tax. The owner is the taxpayer.

What the disregarded entity does file

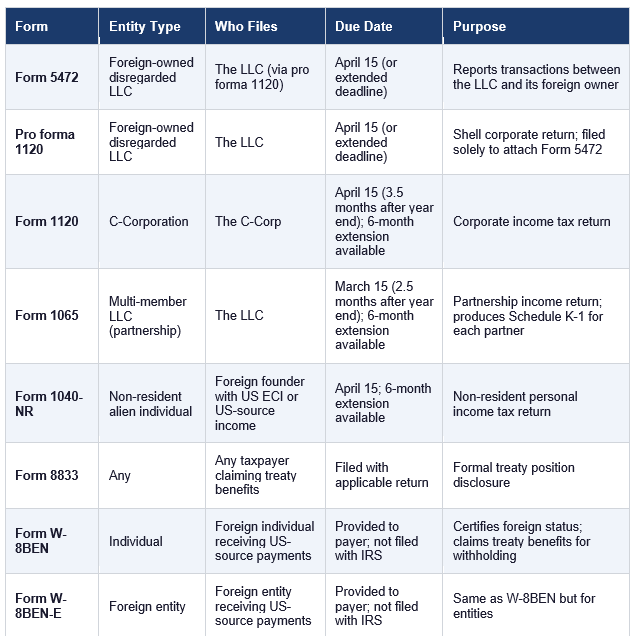

Although a disregarded LLC pays no income tax at the entity level, it does have filing obligations. A foreign-owned single-member LLC is required to file Form 5472 and a pro forma Form 1120. These are information returns, not tax returns. They report the existence of the entity and the transactions between the entity and its foreign owner.

A reportable transaction for Form 5472 purposes includes any exchange of money, property, or services between the LLC and its foreign owner. This includes capital contributions from the owner to the LLC, distributions from the LLC to the owner, loans in either direction, payments for services, and the payment of expenses by one party on behalf of the other. The threshold for reporting is broad: there is no minimum dollar amount. Any transaction between the LLC and the foreign owner is reportable.

$25,000 penalty: The penalty for failing to file Form 5472 is $25,000 per form per year. This penalty applies regardless of whether the entity earned any income or owed any tax. It is one of the most commonly triggered penalties for foreign-owned US entities and one of the most expensive for the same reason: many founders are simply unaware of the requirement. If your LLC has been operating for one or more years without filing Form 5472, the cure is to file the missing returns and consider engaging a professional to manage the penalty abatement process.

When the disregarded LLC has no ECI

A disregarded LLC that generates no ECI and receives only FDAP income does not require a Form 1040-NR filing from the foreign owner. The FDAP income is subject to withholding at the payer level; the owner receives the net amount and has no further US income tax filing obligation on that income. However, the Form 5472 and pro forma 1120 filing obligations remain regardless of whether the entity has ECI. The filing obligation exists because the entity exists, not because it has taxable income.

4. Partnership Taxation: The Multi-Member LLC

A multi-member LLC is treated as a partnership for US federal tax purposes. Partnerships do not pay federal income tax at the entity level. Instead, the partnership's income, deductions, credits, and other tax items flow through to the partners in proportion to their ownership interests, and each partner is taxed on their allocated share.

Form 1065 and Schedule K-1

The partnership files Form 1065, the US Return of Partnership Income, each year. This return reports the partnership's total income, deductions, and other tax items, and allocates them among the partners on Schedule K-1. Each partner receives a Schedule K-1 showing their share of the partnership's items, which they then report on their own tax return. For a non-resident alien partner, the K-1 income flows to Form 1040-NR.

Section 1446 withholding on foreign partners

Partnerships with foreign partners have a specific and important withholding obligation under Section 1446 of the IRC. The partnership is required to withhold US tax on each foreign partner's allocable share of ECI, even if no cash is actually distributed to that partner. The withholding rate is the highest applicable rate for the type of income: 37% for ordinary income allocated to a non-corporate foreign partner, 21% for income allocated to a foreign corporate partner.

The withheld amount is paid to the IRS on behalf of the foreign partner, and the partner receives credit for the withholding on their personal return. But the practical consequence is significant: a profitable partnership may need to remit withholding tax to the IRS on behalf of its foreign partners even in a year when it makes no cash distributions. If the partnership does not have sufficient cash to fund the withholding, it faces a compliance problem. This needs to be planned for from the outset.

Planning note: The Section 1446 withholding obligation falls on the partnership itself, not the individual partner. If you are forming a multi-member LLC with foreign partners, the operating agreement should address how withholding obligations are funded and whether the amounts withheld are treated as advances against future distributions.

Effectively Connected Income vs. non-ECI for partnerships

A partnership's ECI and its non-ECI items are handled differently. ECI is subject to Section 1446 withholding at the partnership level as described above. Non-ECI items, such as FDAP income received by the partnership, are subject to withholding under Section 1441 or 1442, again at the partnership level. The partnership acts as a withholding agent for both categories. Getting this right requires coordination between the partnership and its tax advisors from the moment the entity begins operating.

5. C-Corporation Taxation

A C-Corporation is taxed as a separate entity. It files its own tax return, pays its own taxes, and is entirely distinct from its shareholders for federal income tax purposes. This separation is both the source of the C-Corp's investor appeal and the source of its double taxation problem.

The 21% flat corporate rate

US C-Corporations pay federal income tax at a flat rate of 21% on their taxable income. Taxable income is gross income minus allowable deductions: ordinary and necessary business expenses, depreciation, employee compensation, interest, and other deductible items. The 21% rate applies to all taxable income regardless of amount; there is no graduated rate structure at the federal corporate level.

Deductible expenses and taxable income

The C-Corp's federal taxable income is the foundation of its tax liability, and managing it through legitimate deductions is the primary lever available to reduce the corporate tax bill. Commonly deductible items include employee salaries and benefits, contractor payments, rent for office space, software subscriptions, marketing and advertising expenses, professional fees (legal, accounting, consulting), travel and entertainment subject to the 50% meal deduction limitation, and depreciation on equipment and software.

A C-Corp that pays its founder a reasonable salary for services rendered reduces its taxable income by the amount of that salary. This is one of the primary mechanisms for extracting value from a C-Corp in a tax-efficient way: paying a deductible salary rather than taking non-deductible dividends. The salary must be reasonable for the services performed. Unreasonably high salaries paid to founder-shareholders can be recharacterized by the IRS as disguised dividends, which are not deductible.

Double taxation and when it actually matters

The double taxation of C-Corp earnings is real: the corporation pays 21% corporate tax on its profits, and when it distributes those profits as dividends, the dividends are taxed again in the shareholder's hands at applicable rates. For a non-resident alien shareholder, dividends are subject to US withholding tax at 30% (or a lower treaty rate) on the gross amount.

However, double taxation only materializes when the corporation actually distributes profits. A C-Corp that reinvests all of its profits into growth, product development, and hiring does not trigger the second layer of tax until a distribution event occurs. For VC-backed growth companies, the intended exit event is typically a sale of the company or an IPO, at which point shareholders receive capital gains treatment on the appreciation in their shares, not dividend treatment on accumulated earnings.

The double taxation concern is most relevant for profitable, mature companies that generate consistent cash flow and where the founder wants to extract those profits regularly. For early-stage companies focused on growth, it is typically a secondary consideration.

6. ECI vs. FDAP: Tax Rates, Withholding, and Treaty Interactions

The distinction between ECI and FDAP income is one of the most practically important concepts in US international tax. It determines your tax rate, your filing obligations, your withholding exposure, and whether tax treaties can reduce your liability.

ECI: taxed like a domestic business

ECI is taxed at the same rates that apply to US residents: graduated individual rates for non-corporate taxpayers (currently up to 37% for income above approximately $640,600 for single filers in 2026), or the flat 21% corporate rate for C-Corporations. Critically, ECI is taxed on net income after deductions. If your US business has $500,000 in revenue and $350,000 in deductible expenses, your ECI is $150,000, and you pay tax on $150,000.

A non-resident alien with ECI is required to file Form 1040-NR and report that income. Estimated quarterly tax payments are required if the expected annual tax liability exceeds $1,000 and withholding does not cover it.

FDAP: taxed on the gross amount

FDAP income is taxed at a flat 30% rate on the gross amount received, with no deduction for expenses. If you receive a $100,000 royalty payment from a US company for the use of your intellectual property in the United States, the payer is required to withhold $30,000 and remit it to the IRS. You receive $70,000. No expenses can be deducted against the $100,000.

The 30% rate is the statutory default. It can be reduced or eliminated by a tax treaty between the US and your country of residence. Treaty rates for dividends are commonly 5% or 15% depending on ownership percentage. Treaty rates for interest and royalties are often 0% for residents of countries with strong US treaties. The table in Section 12 of this part shows treaty rates for the most common founder home countries.

Choosing your income category

The ECI versus FDAP characterization is generally determined by the facts and circumstances of your business activities, not by election. But the design of your business structure and operating arrangements can influence which category your income falls into. A US service company with a US office and US employees generates ECI. A foreign company that licenses intellectual property to a US company and has no US operations generates FDAP royalty income. The tax efficiency of each depends on your specific situation: your margin, your applicable treaty rates, and the interaction with your home country tax.

7. Form 5472: The Most Important Form you have never heard of

Form 5472 is an information return that must be filed by any US corporation that is 25% or more foreign owned, or any foreign corporation that is engaged in a US trade or business. Since 2017, the filing requirement was extended to include foreign-owned single-member LLCs, which are required to file Form 5472 attached to a pro forma Form 1120.

The purpose of Form 5472 is to give the IRS visibility into transactions between US entities and their foreign owners or related parties. Without this disclosure, the IRS has limited ability to assess whether income is being shifted offshore through related-party transactions to avoid US tax. Form 5472 is the primary mechanism through which the IRS monitors the transfer pricing behavior of foreign-owned US entities.

What Form 5472 requires you to report

Form 5472 requires the reporting of all transactions between the US entity and any related party that is a foreign person. Reportable transactions include:

• Sales of inventory, goods, or property between the US entity and the foreign owner

• Purchases of inventory, goods, or property from the foreign owner

• Rents and royalties paid or received between the entities

• Loans between the US entity and the foreign owner, including interest paid or received

• Services performed by the US entity for the foreign owner, or by the foreign owner for the US entity

• Amounts paid or received in connection with a cost-sharing arrangement

• Capital contributions from the foreign owner to the US entity

• Distributions from the US entity to the foreign owner

For a typical early-stage single-member LLC, the most common reportable transactions are the initial capital contribution when the foreign founder puts money into the LLC, any distributions from the LLC to the founder, and any management fees or service payments between the LLC and a related foreign entity owned by the founder.

The penalty structure

The penalty for failing to file Form 5472, or for filing a Form 5472 that is incomplete or inaccurate, is $25,000 per form per year. This is not a tax penalty calculated as a percentage of income. It is a flat penalty that applies regardless of whether the entity has any income or owes any tax. It applies per form: if you have two reportable entities and file neither, the penalty is $50,000. If the failure continues after the IRS notifies you, an additional $25,000 penalty applies for each 30-day period of continued failure.

The IRS has broad authority to assess this penalty, and while penalty abatement is available for reasonable cause, demonstrating reasonable cause for failure to file a required information return requires a substantive showing. 'I did not know about the requirement' is not, by itself, reasonable cause. However, first-time penalty abatement is available to taxpayers with a clean compliance history, and engaging a qualified professional to file delinquent returns and request abatement is often effective.

First priority: If you own a foreign-owned US LLC and have never filed Form 5472, this is the single most urgent compliance issue to address. The penalty compounds annually. Addressing it proactively, before the IRS contacts you, gives you the best opportunity for penalty abatement.

8. Pro Forma Form 1120: The Shell Return

A foreign-owned single-member LLC is a disregarded entity and does not file a regular corporate tax return. However, because the LLC is required to file Form 5472, and Form 5472 must be attached to a corporate return, the IRS requires the LLC to file a pro forma Form 1120.

A pro forma Form 1120 is a Form 1120 that is completed only to the extent necessary to support the attached Form 5472. The LLC enters its name, address, and EIN on the form, indicates that it is a foreign-owned disregarded entity, and attaches Form 5472. It does not complete the income, deductions, or tax liability sections in the way a regular C-Corp would, because the LLC has no entity-level tax liability. The form exists solely as a vehicle for submitting Form 5472 to the IRS.

The pro forma 1120 and attached Form 5472 are filed by the extended due date for Form 1120, which is generally October 15 for calendar-year entities (April 15 original deadline, plus six-month extension). The filing must be sent to the IRS Service Center in Ogden, Utah, not to the standard Form 1120 filing address - Also note the latest requirements - https://www.irs.gov/pub/irs-pdf/i5472.pdf

9. Form 1040-NR: The Non-Resident Personal Return

Form 1040-NR is the US federal income tax return for non-resident aliens. If you are a non-resident alien who has US-source ECI during the tax year, you are required to file Form 1040-NR and report that income. You are also required to file Form 1040-NR if you have any US tax liability, or if you want to claim a refund of any US tax that was withheld from your income during the year.

When a non-US founder must file Form 1040-NR

As a non-resident alien operating a US business through a disregarded LLC, the following situations require a Form 1040-NR filing:

• Your disregarded LLC generated ECI during the tax year, and you have US income tax liability on that income after applicable deductions and credits

• You are a partner in a US partnership (multi-member LLC) and received a Schedule K-1 showing ECI allocated to you

• You received US-source wages, salary, or other compensation for services performed in the United States

• You have US-source income on which the withholding was insufficient to cover the full tax due, or from which you want to claim a refund of excess withholding

What Form 1040-NR covers

Form 1040-NR reports your ECI from US sources: business income from the disregarded LLC, wages for services performed in the US, and other US-connected income. It also allows you to claim deductions against your ECI, including business expenses of the LLC, the deductible portion of self-employment tax (if applicable), and certain itemized deductions. The result is your US taxable income, to which graduated US income tax rates are applied.

Form 1040-NR also has a section for US-source income that is not ECI (FDAP income), though most FDAP income is fully withheld at the source and does not create a filing obligation in itself unless you are claiming a refund or a treaty benefit that reduces the withholding rate.

Dual-status returns

If you become a US tax resident partway through a year (because you met the Substantial Presence Test after arriving in the US) or cease to be a US resident partway through a year (because you left), you may need to file a dual-status return for that year. A dual-status return covers the period you were a resident (on Form 1040) and the period you were a non-resident (on Form 1040-NR). This is a more complex filing than either a pure resident or pure non-resident return, and it requires careful handling to avoid errors in how income from each period is reported.

10. Withholding Tax on Payments Leaving the US

The US operates a withholding tax system on certain payments made to non-residents and foreign entities. The withholding is collected at the source: the US person or entity making the payment is responsible for deducting the withholding amount and remitting it to the IRS. The recipient receives the net amount.

Understanding the withholding rules matters for non-US founders in two directions: as a recipient of US-source payments subject to withholding, and as a US entity making payments to foreign persons that may be subject to withholding obligations.

The 30% default rate

The default withholding rate on FDAP payments to non-resident aliens and foreign entities is 30% of the gross amount. This applies to dividends paid by a US C-Corp to its foreign founder, interest paid to a foreign person on a US obligation, royalties paid to a foreign person for the use of intellectual property in the United States, and certain other fixed or periodic payments from US sources.

The 30% rate is reduced by applicable tax treaties. For founders from treaty countries, the treaty rate for dividends is typically 5% or 15%, for interest is often 0%, and for royalties is typically 0% to 15% depending on the type of intellectual property and the specific treaty.

Claiming treaty benefits: Form W-8BEN and W-8BEN-E

To claim a reduced withholding rate under a tax treaty, the non-US recipient must provide the US payer with a valid Form W-8BEN (for individuals) or Form W-8BEN-E (for entities). These forms certify the recipient's foreign status and, where a treaty rate is being claimed, the specific treaty article under which the reduction is sought.

Without a valid Form W-8, the US payer is required to withhold at the 30% default rate. If you are a non-US founder receiving dividends, royalties, or other FDAP payments from your US entity or from US customers, providing a completed Form W-8BEN to the payer is how you ensure the correct withholding rate is applied. These forms are valid for three years from the date of signature and must be renewed.

The US entity as a withholding agent

Your US entity may itself have withholding obligations as a payer. If your C-Corp pays dividends to its foreign founder, it is required to withhold at the applicable rate (30% or treaty-reduced rate) and remit the withheld amount to the IRS. If your LLC or C-Corp makes royalty payments to a related foreign entity, those payments may be subject to withholding. If the US entity makes payments to foreign contractors for services performed in the United States, withholding may apply.

Failing to withhold and remit required amounts as a withholding agent creates liability for the US entity itself. The IRS can collect the unwithheld tax from the withholding agent, plus interest and penalties, even if the foreign recipient has already paid the tax in their own country. Getting the withholding mechanics right is a compliance obligation of the US entity, not just the foreign recipient.

11. Tax Treaties: What they Cover and how to use them

The United States has income tax treaties with many countries covering the majority of the developed world, though notable gaps exist. These treaties serve two primary purposes: eliminating or reducing double taxation, and providing clarity on which country has the right to tax specific categories of income.

What treaties typically cover

Most US income tax treaties contain provisions addressing the following:

• Reduced withholding rates: Treaties typically reduce the 30% default withholding rate on dividends, interest, and royalties to lower rates, often 0% to 15% depending on the income type and the specific treaty.

• Permanent Establishment: Treaties define the threshold at which a foreign company's US activities create a taxable presence. The treaty PE standard is generally higher than the domestic ETBUS standard, providing some protection for foreign companies with limited US activities.

• Residence and tiebreaker rules: Treaties include rules for resolving situations where an individual or entity is considered a resident of both treaty countries under their respective domestic laws.

• Exchange of information: Treaties authorize the tax authorities of both countries to share taxpayer information to assist in tax enforcement. This is not relevant to most compliant taxpayers but is worth understanding: if you have a US entity and a home country tax authority, those two authorities can and do share information.

• Non-discrimination: Most treaties include provisions preventing the host country from imposing more burdensome taxes on the other country's residents than it imposes on its own residents in comparable circumstances.

Limitation on Benefits clauses

Modern US tax treaties include a Limitation on Benefits (LOB) clause designed to prevent treaty shopping: the practice of routing income through a third country in order to access that country's favorable treaty with the US. The LOB clause restricts treaty benefits to persons who have a substantial connection to the treaty country, either through ownership, residency, or active business activity there.

For most genuine founders who are actually resident in the treaty country and running a real business there, the LOB clause is not a problem. It becomes relevant in structures where a holding company in a treaty-favorable jurisdiction is interposed specifically to reduce US withholding, without the holding company having genuine economic substance in that jurisdiction.

How to formally claim a treaty benefit: Form 8833

If you are taking a position on a US tax return that is based on a treaty, you are generally required to disclose that position on Form 8833 (Treaty-Based Return Position Disclosure). This form identifies the specific treaty, the specific treaty article you are relying on, and an explanation of how that article applies to your situation.

Form 8833 is filed as part of your tax return. Failure to file it when required does not invalidate your treaty position, but it can result in a penalty of $1,000 per failure ($10,000 for C-Corps). More importantly, filing Form 8833 creates a clear record of your treaty position that can be defended in an audit. Taking a treaty position without disclosing it creates the same tax benefit but with greater risk if the IRS examines the return.

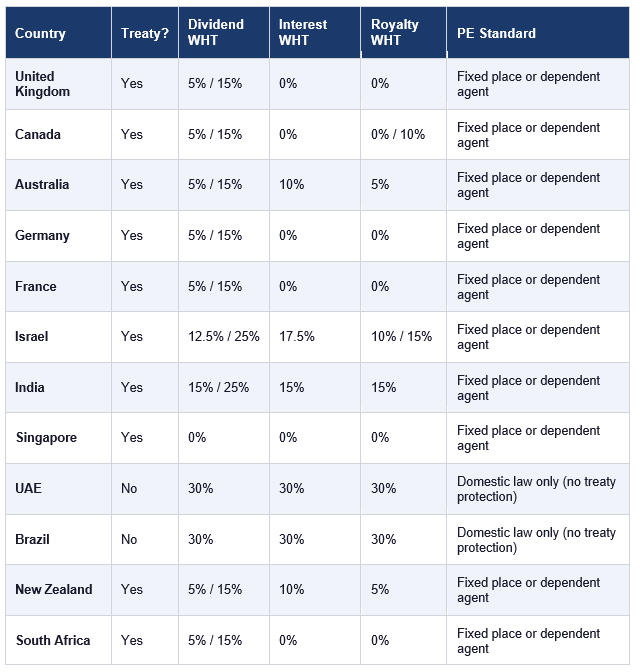

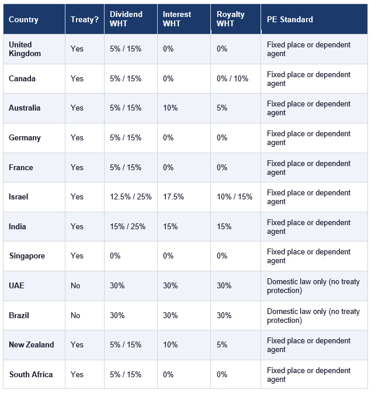

12. Treaty Rates by Country: Quick Reference

The following table shows key treaty provisions for the home countries most commonly represented among non-US founders. Withholding rates shown are the treaty-reduced rates; the default rate without a treaty is 30% on all categories. Dividend rates shown are for the most common ownership scenarios (qualifying / non-qualifying). Treaty provisions are subject to change and this table should be confirmed against current treaty text and IRS guidance before relying on it.

Important: Treaty rates for dividends often depend on the ownership percentage held by the recipient. A 5% rate commonly applies when the recipient owns 10% or more of the paying corporation; a 15% rate applies otherwise. The exact thresholds vary by treaty. Royalty rates may also vary depending on whether the royalty is for the use of industrial, commercial, or scientific equipment versus patents, trademarks, or literary works

13. The Branch Profits Tax

The Branch Profits Tax (BPT) is covered briefly in Part 2 in the context of entity selection. This section provides the full treatment for founders whose structures may be affected by it.

The BPT applies to foreign corporations that have ECI from a US trade or business conducted directly through a branch rather than through a separately incorporated US subsidiary. It is imposed at a rate of 30% (reducible by treaty) on the "dividend equivalent amount" for the year, which is broadly the portion of the branch's US earnings that are deemed to have been sent back to the foreign parent.

The BPT is designed to impose a second level of tax on branch profits equivalent to the withholding tax that would apply if a US subsidiary had distributed its earnings as dividends to its foreign parent. Without the BPT, operating in the US through a branch rather than a subsidiary would allow a foreign company to avoid the dividend withholding tax entirely.

When the BPT is relevant for non-US founders

For most non-US founders who have formed a US LLC or C-Corp as a standalone entity, the BPT is not directly applicable. It becomes relevant in the following situations:

• A foreign parent company has a US branch (not a separately incorporated subsidiary) that generates ECI

• A treaty between the US and the foreign parent's country of residence reduces the BPT rate below 30%

• A foreign-owned US entity is structured in a way that the IRS could characterize certain payments as equivalent to branch profit repatriation

If your structure involves a foreign operating company with US branch activities rather than a separately incorporated US entity, the BPT needs to be factored into your tax analysis. Incorporating a US subsidiary to receive the US business income eliminates the BPT at the branch level, though dividend withholding at the subsidiary-to-parent level then needs to be managed.

14. Transfer Pricing: The Arm's Length Standard

Transfer pricing refers to the prices charged in transactions between related entities: your US LLC and your UK operating company, for example, or your Delaware C-Corp and your Singapore holding entity. The IRS requires that these intercompany transactions be priced on an arm's length basis, meaning at the price that unrelated third parties would charge each other for the same transaction in similar circumstances.

Transfer pricing is one of the most complex areas of US international tax, and most early-stage non-US founders encounter it in a simplified form: management fees, intercompany loans, and IP licensing arrangements between their US entity and a related foreign entity. Getting the pricing wrong, even unintentionally, can result in IRS adjustments that increase the US entity's taxable income, penalties for underpayment, and the possibility of double taxation if the corresponding entity's home country does not make an offsetting adjustment.

The most common transfer pricing scenarios for non-US founders

Management fees are the most common transfer pricing issue for early-stage founders. If your US entity pays a management fee to your foreign entity for services (strategic oversight, shared staff, use of systems), the IRS expects that fee to reflect the fair market value of the services received. A management fee that is set at a round number without any economic analysis is likely to be scrutinized. A management fee that is supported by a brief transfer pricing analysis showing comparable market rates is defensible.

IP licensing is the second most common scenario. If your foreign entity owns intellectual property that the US entity uses, the royalty paid from the US entity to the foreign entity needs to reflect the arm's length rate for that type of IP in that type of transaction. Setting the royalty at zero (or at an inflated rate) creates transfer pricing exposure.

Intercompany loans require the use of an arm's length interest rate. The IRS publishes Applicable Federal Rates (AFRs) monthly, which are accepted as safe harbor rates for many intercompany loans. Loans between related entities with no interest, or with interest below the applicable AFR, can be recharacterized as equity or gifts.

Documentation requirements

US transfer pricing documentation requirements scale with the size of the intercompany transactions. For most early-stage founders, formal transfer pricing studies are not required, but maintaining a written record of how intercompany prices were determined, what comparable transactions were considered, and why the selected price reflects arm's length dealing is sound practice. If your US entity ever faces an IRS examination, this documentation is what stands between you and a transfer pricing adjustment.

15. GILTI and Subpart F: When these Rules Affect Non-US Founders

GILTI (Global Intangible Low-Taxed Income) and Subpart F are US anti-deferral rules that require US shareholders of certain foreign corporations to include a portion of the foreign corporation's income in their US taxable income currently, rather than deferring it until a distribution is made. These rules are primarily aimed at preventing US multinationals from parking profits in low-tax foreign subsidiaries.

For most non-US founders, GILTI and Subpart F are not directly relevant, because these rules apply to US shareholders of foreign corporations, not to foreign shareholders of US entities. However, there are two scenarios where non-US founders encounter them.

Scenario 1: The founder becomes a US tax resident

If a non-US founder who owns a foreign operating company becomes a US tax resident (by meeting the Substantial Presence Test or obtaining a green card), they become a US shareholder of their foreign company. If they own more than 50% of the foreign company's voting power or value, the foreign company becomes a Controlled Foreign Corporation (CFC) for US purposes. As a CFC, the foreign company's Subpart F income (passive income, certain related-party sales, and services income) is taxable to the US shareholder currently, regardless of distributions. GILTI brings most operating income of CFCs into current inclusion as well.

This is a critical planning point for founders who are considering moving to the United States. The moment you become a US tax resident, your foreign company's income may become currently taxable in the US, even if you never bring a dollar of it to the US. Pre-immigration tax planning with a US international tax advisor is essential for any founder who owns a foreign business and is moving to the US.

Scenario 2: The US entity has foreign corporate shareholders

GILTI and Subpart F can also become relevant if your US C-Corp is owned by a foreign holding corporation rather than by you personally, and that foreign corporation has US shareholders. If the foreign holding corporation is a CFC with respect to those US shareholders, the US C-Corp's income may feed into the CFC's income for Subpart F and GILTI purposes. This is a more complex multi-entity scenario that requires specialized advice to navigate correctly.

16. Section 83(b) Elections: A Reminder

Section 83(b) elections are covered in full in Part 3. This section is a reminder of their relevance in the context of federal tax, because the consequences of missing the election are tax consequences, not just administrative ones.

If you received equity in your US C-Corp subject to a vesting schedule and did not file a Section 83(b) election within 30 days of the grant date, you will recognize ordinary income equal to the fair market value of the equity at each vesting date. For a founder whose equity was worth very little at grant but is worth significantly more at vesting, this can create a large ordinary income tax liability with no corresponding cash to pay it. The election cannot be filed retroactively.

If you are in this situation, consult a US tax advisor about what options may be available to manage the tax liability at vesting dates going forward.

17. Estimated Tax Payments

US tax is a pay-as-you-go system. Tax is not simply paid in a lump sum at filing time. For individuals (including non-resident alien founders who file Form 1040-NR), estimated tax payments are required if you expect to owe at least $1,000 in federal tax for the year after subtracting any withholding, and if withholding will cover less than the smaller of 90% of your current year tax liability or 100% of your prior year tax liability.

Quarterly payment schedule

Estimated tax payments are due four times per year on the following dates:

• April 15: payment for income received January 1 through March 31

• June 15: payment for income received April 1 through May 31

• September 15: payment for income received June 1 through August 31

• January 15 of the following year: payment for income received September 1 through December 31

Each payment is an estimate of the tax owed on income received in that period. The total of the four payments should cover at least 90% of the year's actual tax liability, or 100% of the prior year's tax liability (110% if your prior year adjusted gross income exceeded $150,000), to avoid underpayment penalties.

C-Corp estimated payments

C-Corporations are also required to make estimated tax payments, due on the 15th day of the fourth, sixth, ninth, and twelfth months of the corporation's tax year. For a calendar-year C-Corp, this means April 15, June 15, September 15, and December 15. The corporation must pay at least 25% of its estimated annual tax liability in each installment, with the total covering 100% of the current year liability or 100% of the prior year liability to avoid penalties.

18. Federal Tax Forms: Quick Reference

The following table summarizes the key federal tax forms relevant to non-US founders operating US entities. Filing deadlines shown assume a calendar tax year. Extensions are available for most returns but do not extend the time to pay tax due.

Before you move to Part 6

Part 6 covers US state tax: the separate layer of tax obligations that exist in every state where your business operates, employs people, or has economic nexus. It covers state income tax, sales tax and the Wayfair economic nexus rules, franchise taxes, and the state-by-state compliance differences that catch many founders off guard.

Before you move on, confirm that you have clarity on the following from this part:

• Whether you are a US tax resident or non-resident alien, and whether your day count creates any risk of inadvertent residency

• Which forms your US entity is required to file, and whether you are current on those filings

• Whether Form 5472 has been filed for every year your foreign-owned LLC has been in existence

• Whether your home country has a tax treaty with the US, and whether you are claiming the treaty benefits you are entitled to

• Whether your intercompany transactions with related foreign entities are documented and priced at arm's length

• Whether you have a system for making estimated quarterly tax payments

Antravia Advisory: US federal tax for non-US founders is an area where professional guidance pays for itself many times over. The penalties for missed filings are steep, the treaty benefits for those who claim them correctly are valuable, and the interaction with your home country tax position requires both sides to be coordinated. We work with non-US founders to get this right from the start and keep it right as the business grows.

Continue to Part 6: US State Tax

About Antravia Advisory

Antravia Advisory is a US-based tax and accounting advisory firm headquartered in Winter Park, Florida, operating nationally and internationally.

We advise international businesses entering the United States and complex US companies operating across multiple states, entities, and revenue structures. Our work spans advanced tax strategy, multi-state sales tax oversight, cross-border structuring, and high-level accounting architecture for e-commerce brands, subscription and SaaS businesses, platform-based models, and multi-entity groups.

We work with founders and leadership teams who require technical precision, structural clarity, and financial frameworks built for scale, capital events, and long-term resilience.

The Non-US Founder’s Complete Guide to Running a US Business

Part 1 — Before You Start

Part 2 — Choosing Your US Entity

Part 3 — Formation

Part 4 — US Banking

Part 5 — US Federal Tax

Part 6 — US State Tax

Part 7 — Paying Yourself

Part 8 — Accounting and Bookkeeping

Part 9 — Annual Compliance Calendar

Part 10 — Hiring in the US

Part 11 — Intellectual Property and Contracts

Part 12 — Your Home Country Obligations

Part 13 — Applied Business Types

Part 14 — Exiting, Winding Down, or Restructuring

Disclaimer:

Content published by Antravia is provided for informational purposes only and reflects research, industry analysis, and our professional perspective. It does not constitute legal, tax, or accounting advice. Regulations vary by jurisdiction, and individual circumstances differ. Readers should seek advice from a qualified professional before making decisions that could affect their business.

See also our Disclaimer page

Antravia Advisory

Accounting built for complexity

Not legal advice, always verify with your Accountant

Email:

Contact us:

© 2025. All rights reserved. | Disclaimer | Privacy Policy | Terms of Use |

contact@antravia.com

Antravia LLC

941 W Morse Blvd suite 100

Winter Park

Florida

32789