Part 10: Hiring in the United States

The Non-US Founder's Complete Guide to Running a US Business - Part 10 explains how to hire in the United States, covering employee vs contractor classification, payroll and compliance requirements, multi-state employment rules, EOR structures, benefits expectations, and immigration considerations for foreign-owned U.S. businesses.

THE NON-US FOUNDER'S COMPLETE GUIDE TO RUNNING A US BUSINESS

5/3/202626 min read

Hiring your first US-based worker is one of the most significant operational steps a non-US founder takes. It changes your compliance obligations immediately and in multiple states simultaneously. It introduces federal and state employment law requirements that did not exist before. It creates ongoing payroll, benefits, and HR obligations. And it forces the employee versus contractor question, which if answered incorrectly carries consequences that can be expensive to resolve.

This part covers everything a non-US founder needs to know about bringing people into a US business: the employee versus independent contractor distinction and why it matters so much, the step-by-step hiring process for each category, employer obligations under federal and state law, the Employer of Record model as an alternative to direct employment, benefits and compensation considerations, multi-state hiring complexity, and how to manage the ongoing HR compliance obligations that come with a US workforce.

1. Employee vs. Independent Contractor: The most Consequential Classification Decision

The distinction between an employee and an independent contractor is one of the most heavily enforced areas of US employment and tax law. Getting it wrong, specifically treating someone as an independent contractor when they should legally be classified as an employee, is called misclassification. The consequences include back payroll taxes, interest, penalties, unpaid benefits, state labor law violations, and potential personal liability for the owners of the misclassifying entity.

The reason misclassification is so common is that the correct answer is not always obvious. The classification depends on the facts and circumstances of the working relationship, not on what the contract says or what either party prefers. A contract that calls someone an independent contractor does not make them one. What matters is how the relationship actually works in practice.

Why the distinction matters

When you hire an employee, you take on a set of obligations that do not exist with a contractor: you must withhold and remit federal and state income tax, pay the employer half of FICA taxes, pay federal and state unemployment insurance, provide workers compensation insurance, comply with federal and state wage and hour laws (minimum wage, overtime, rest breaks), provide required notices and disclosures, and in some cases offer benefits such as health insurance and retirement plan access.

When you engage an independent contractor, none of these obligations apply. The contractor pays their own self-employment taxes, carries their own insurance, sets their own hours, and receives a Form 1099-NEC at year end rather than a W-2. The contractor relationship is simpler to administer and lower-cost from a compliance perspective. This is why misclassification almost always runs in one direction: employers classifying workers as contractors when those workers should legally be employees.

How the IRS and states determine classification

The IRS uses a common law control test based on three categories of factors: behavioral control, financial control, and the type of relationship. No single factor is determinative. The analysis requires weighing all relevant factors together and assessing which category the overall relationship most closely resembles.

Many states apply their own classification tests, and some are significantly stricter than the IRS standard. California uses the ABC test, which presumes all workers are employees unless the hiring entity can demonstrate all three of the following: the worker is free from the company's control in performing the work, the work is outside the company's usual course of business, and the worker is customarily engaged in an independently established trade or occupation. The California ABC test is very difficult to satisfy for workers who perform core business functions. A software company that hires a software developer as a contractor in California is likely to face classification challenges under the ABC test regardless of what the contract says.

Massachusetts, New Jersey, Illinois, and several other states also use ABC-style tests that are more worker-protective than the IRS standard. If you are hiring workers in these states, apply the state test, not just the federal one.

XXXXXXXXXXXXXXXX

Behavioral control

If the company directs how, when, and where the work is done, this points toward employee status.

If the worker controls how and when the work is done, this points toward contractor status.

Tools and equipment

If the company provides the tools, equipment, and workspace, this points toward employee status.

If the worker uses their own tools and equipment, this points toward contractor status.

Training

If the company trains the worker in specific methods, this points toward employee status.

If the worker brings their own skills and methods, this points toward contractor status.

Integration into the business

If the worker’s services are integral to the business, this points toward employee status.

If the worker provides services to multiple clients, this points toward contractor status.

Working hours

If the company sets specific hours of work, this points toward employee status.

If the worker sets their own schedule, this points toward contractor status.

Full-time commitment

If the worker is available full-time to the company, this points toward employee status.

If the worker works for multiple clients at the same time, this points toward contractor status.

Location

If the work must be performed at company premises, this points toward employee status.

If the worker can work from any location, this points toward contractor status.

Sequence of work

If the company dictates the order and sequence of tasks, this points toward employee status.

If the worker decides their own approach, this points toward contractor status.

Financial control

If the company controls how the worker is paid and the worker has no real risk of profit or loss, this points toward employee status.

If the worker sets their own rates, bears business risk, and can profit or lose, this points toward contractor status.

Payment method

If the worker is paid hourly, weekly, or by salary, this points toward employee status.

If the worker is paid per project or by invoice, this points toward contractor status.

Expenses

If the company reimburses business expenses, this points toward employee status.

If the worker pays their own business expenses, this points toward contractor status.

Relationship type

If the relationship is ongoing with no defined end, this points toward employee status.

If the work is project-based or fixed-term, this points toward contractor status.

Written contract

If there is no independent contractor agreement, this points toward employee status.

If there is a written contractor agreement with a clear project scope and terms, this points toward contractor status.

The contract helps, but it does not decide the classification by itself.

Benefits

If the company provides health insurance, vacation, or retirement benefits, this points toward employee status.

If no benefits are provided and the worker is responsible for their own benefits, this points toward contractor status.

The contract does not determine the classification: The most common misunderstanding about independent contractor status is that having a signed independent contractor agreement makes the classification correct. It does not. The IRS and state agencies look at the actual working relationship, not the label. If your contractor works set hours, uses your equipment, takes direction from you on how to do their work, and dedicates substantially all of their working time to your company, they are likely an employee regardless of what the agreement says.

Consequences of misclassification

If the IRS or a state agency determines that you have misclassified employees as independent contractors, the consequences include: liability for the employer's share of FICA taxes for all misclassified workers for all open tax years, liability for the employee's share of FICA taxes that should have been withheld (which the employer typically cannot recover from the workers after the fact), federal and state income tax withholding that should have been remitted, unemployment insurance contributions that were not made, interest on all of the above from the date they were due, and civil penalties.

State consequences can be more severe. California, for example, imposes penalties of $5,000 to $15,000 per violation for willful misclassification, with amounts increasing for patterns of violations. State labor departments can also require payment of back wages for overtime that was not paid because the worker was treated as a contractor not subject to overtime rules.

The practical lesson is to make the employee versus contractor determination carefully and conservatively. When in doubt, classify as an employee. The cost of correctly classifying a borderline worker as an employee from the start is significantly lower than the cost of defending a misclassification finding and paying back taxes, interest, and penalties for multiple years.

2. Hiring an Independent Contractor: The Correct Process

When a worker genuinely qualifies as an independent contractor under the applicable federal and state tests, the engagement process is simpler than employee hiring but still requires specific documentation and compliance steps.

The independent contractor agreement

Every contractor engagement should be documented with a written independent contractor agreement signed before work begins. The agreement should specify: the scope of work and deliverables, the start and end dates or conditions for termination, the rate and payment terms, confirmation that the contractor is responsible for their own taxes and insurance, a statement that the contractor is free to work for other clients, intellectual property assignment provisions (ensuring that any work product created belongs to your company), confidentiality obligations, and the dispute resolution mechanism.

The IP assignment clause deserves particular attention. In the absence of a written agreement that assigns intellectual property to the company, work created by an independent contractor may belong to the contractor rather than to the company, regardless of who paid for it. This is different from the employee situation, where work created within the scope of employment is generally considered work made for hire and owned by the employer automatically. For a contractor, the ownership transfer must be in writing.

Form W-9 for domestic contractors

Before making the first payment to a US-based independent contractor, collect a completed Form W-9 from them. The W-9 provides their legal name, business name if different, taxpayer identification number (SSN or EIN), and tax classification. You need this information to issue a Form 1099-NEC at year end for any contractor paid $600 or more during the year. Collecting the W-9 before the first payment is simpler than chasing contractors for it in January when you are preparing information returns.

Form W-8BEN or W-8BEN-E for foreign contractors

If you are paying a foreign independent contractor for services performed outside the United States, different rules apply. Services performed entirely outside the US by a non-US person are generally not US-source income and are not subject to US withholding or 1099 reporting. However, if the foreign contractor performs services inside the United States, the payment may be considered ECI (Effectively Connected Income).

To establish a foreign contractor's status, collect a completed Form W-8BEN (for individuals) or W-8BEN-E (for entities) before making the first payment. The W-8 certifies the contractor's foreign status and, if applicable, the treaty country of residence. Keep the W-8 on file and renew it every three years. If the contractor cannot provide a W-8 and the payment may be US-source, withhold at 30% and remit to the IRS on Form 1042.

Form 1099-NEC at year end

For each US-based independent contractor paid $600 or more during the calendar year, you must issue a Form 1099-NEC by January 31 of the following year and file a copy with the IRS by the same date (for electronic filers) or February 28 (for paper filers). The 1099-NEC reports the total payments made to the contractor during the year and allows the IRS to cross-reference the contractor's income tax return.

You do not issue 1099-NECs to corporations (C-Corps or S-Corps), to foreign contractors whose services were performed outside the US, or sometimes to contractors paid via credit card or payment platforms like PayPal and Stripe (those platforms issue their own Form 1099-K to the contractor but this depends on payment settlement entity rules and thresholds). For sole proprietors, LLCs taxed as sole proprietors, and partnerships (other than law firms), the 1099-NEC is required if the $600 threshold is met.

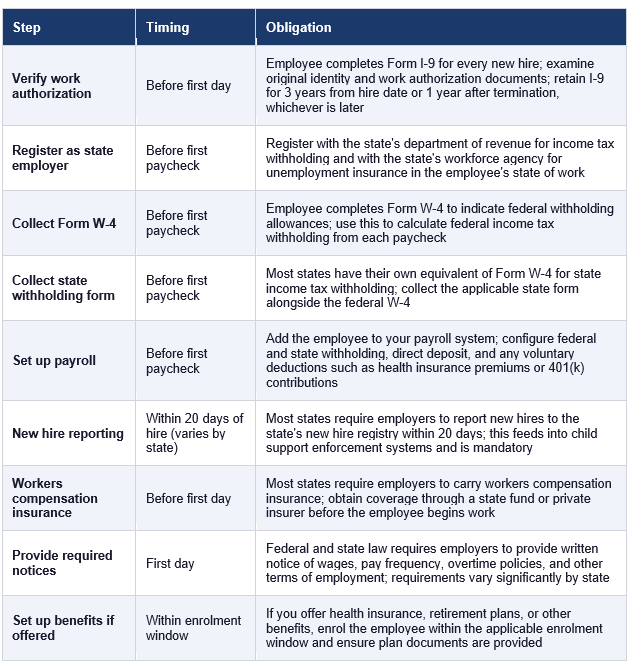

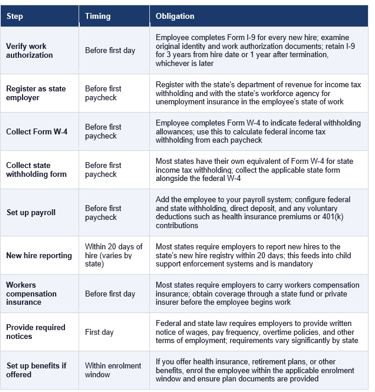

3. Hiring a US Employee: The Step-by-Step Process

Hiring a US employee involves a specific sequence of steps that must be completed in a particular order. Many of these steps must be done before the employee's first day or first paycheck. Missing steps or completing them out of sequence creates compliance gaps that can be difficult and costly to correct retroactively.

Form I-9: Verifying work authorization

Every US employer must verify that each newly hired employee is legally authorized to work in the United States. This verification is performed using Form I-9, which requires the employee to present original identity and work authorization documents from a prescribed list. Acceptable documents are organized into List A (documents that establish both identity and work authorization, such as a US passport or Permanent Resident Card) and List B plus List C (separate documents establishing identity and work authorization respectively, such as a driver's license plus a Social Security card).

The employee normally must present original documents, not copies. You must physically examine the originals (or use the authorized remote examination procedure if no original documents) and record the document information on the Form I-9 within three business days of the employee's first day. The I-9 must be retained for three years from the hire date or one year after the employee's last day of employment, whichever is later. I-9s are subject to inspection by the Department of Homeland Security and US Immigration and Customs Enforcement.

Note that Form I-9 only verifies that the employee is authorized to work. It does not verify immigration status for any other purpose and does not create any right to employment. Non-discrimination rules prohibit employers from requesting more or different documents than the law requires or from treating employees differently based on their citizenship status or national origin in the I-9 process.

At-will employment and offer letters

Most US states operate under the at-will employment doctrine, which means either party can end the employment relationship at any time, for any reason that is not illegal, without advance notice and without severance. This is very different from employment law in most of Europe, where terminating an employee typically requires notice, a legitimate reason, and often a severance payment.

At-will employment is the default in the US unless it is modified by a contract. A well-drafted offer letter preserves at-will status while setting clear expectations about compensation, benefits, start date, and reporting structure. Avoid language in offer letters that implies a guaranteed duration of employment, promises of continued employment, or conditions on termination that go beyond those required by law. Phrases like 'permanent position' or 'as long as you perform well' have been used to argue against at-will status in disputes.

California, Montana, and a small number of other states or jurisdictions have limitations on at-will employment or require cause for termination in certain circumstances. Montana is the only state that is not fully at-will, but only after a probationary period. California is mostly at-will but with some exceptions.

If you are hiring in these jurisdictions, confirm the applicable rules before drafting your offer letter.

Federal wage and hour law: FLSA basics

The Fair Labor Standards Act (FLSA) establishes the federal minimum wage, overtime requirements, and child labor restrictions. The current federal minimum wage is $7.25 per hour, though many states and cities have significantly higher minimums. The applicable minimum wage is the higher of the federal minimum and the state or local minimum for the employee's work location.

The FLSA requires that non-exempt employees be paid at least 1.5 times their regular rate of pay for all hours worked over 40 in a workweek. Employees classified as exempt from overtime must meet both a salary threshold (currently $684 per week, or $35,568 annually) and a duties test based on the nature of their work. The most common exemptions are for executive, administrative, and professional employees. Misclassifying a non-exempt employee as exempt from overtime is a common and expensive compliance error.

States frequently have their own wage and hour laws that are more protective than the FLSA. California's overtime rules, for example, require daily overtime (1.5x for hours over 8 per day) and double time (2x for hours over 12 per day), which is more generous to employees than the federal weekly overtime standard. When federal and state rules conflict, the rule most protective of the employee applies.

4. Federal Employer Obligations Beyond Payroll

Payroll tax compliance, covered in Part 9, is the most visible federal employer obligation but not the only one. Federal employment law imposes a range of additional requirements on employers that apply regardless of the employee's state of residence.

Anti-discrimination law

Federal law prohibits employers from discriminating against employees or applicants on the basis of race, color, religion, sex, national origin, age (for workers 40 and older), disability, genetic information, and pregnancy. These protections are administered by the Equal Employment Opportunity Commission (EEOC) and enforced through administrative charges and federal litigation.

The federal anti-discrimination laws apply to employers with a minimum number of employees: Title VII (race, color, religion, sex, national origin) applies to employers with 15 or more employees; the Age Discrimination in Employment Act applies to employers with 20 or more employees; the Americans with Disabilities Act applies to employers with 15 or more employees. For very small employers in early stages, these thresholds mean some federal protections do not yet apply, though most states have their own anti-discrimination laws that cover smaller employers.

Family and Medical Leave Act

The Family and Medical Leave Act (FMLA) requires employers with 50 or more employees to provide up to 12 weeks of unpaid, job-protected leave per year for qualifying family and medical reasons, including the birth or adoption of a child, serious health conditions of the employee or immediate family members, and military deployment situations. Employees must have worked for the employer for at least 12 months and at least 1,250 hours during the prior year to be eligible.

For most early-stage foreign-owned US entities with fewer than 50 US employees, FMLA does not yet apply. However, many states have their own family and medical leave laws that apply to smaller employers and in some cases provide paid leave. California, New York, New Jersey, Washington, Oregon, Colorado, and several other states have state-run paid leave programs funded by employee payroll deductions.

Workers compensation insurance

Workers compensation insurance is required by law in most states for all employers with at least one employee. It provides benefits to employees who suffer work-related injuries or illnesses, covering medical expenses, lost wages during recovery, and permanent disability payments where applicable. In exchange, employees generally cannot sue their employer in tort for work-related injuries; workers compensation is the exclusive remedy.

Workers compensation insurance is obtained either from a state-run insurance fund or from a private insurer, depending on the state. The cost varies by the type of work performed: office workers have very low rates, while construction and manual labor workers have significantly higher rates. Coverage must be in place before the employee's first day of work. Operating without required workers compensation coverage exposes the employer to substantial fines, civil liability, and in some states criminal penalties.

OSHA: Workplace safety

The Occupational Safety and Health Act requires employers to provide a workplace free from recognized hazards that are causing or likely to cause death or serious physical harm. The Occupational Safety and Health Administration (OSHA) enforces these requirements through inspections and can issue citations and fines for violations. Most OSHA requirements are more relevant for physical workplaces and manufacturing environments than for remote-first technology companies, but all employers are subject to the general duty clause requiring a safe workplace.

5. State Employment Law: Why it varies so much

Federal employment law sets a floor. States can and frequently do impose more protective requirements on employers. The result is that the employment law obligations of a US employer vary significantly depending on which states their employees work in. A company with employees in California, New York, and Texas faces three materially different state employment law environments.

California employment law

California has the most employer-protective employment laws in the United States, and it enforces them aggressively. For non-US founders hiring their first US employees, California is the state most likely to create compliance surprises. Key California-specific requirements that go beyond federal law include:

Minimum wage significantly above the federal minimum, currently $16 per hour for most employers and $20 per hour for fast food workers, with further increases scheduled

Daily overtime requirements (1.5x for hours over 8 per day; 2x for hours over 12 per day) in addition to weekly overtime

Mandatory paid sick leave: employees accrue at least one hour of paid sick leave for every 30 hours worked, up to 40 hours per year

Required meal periods: employees working more than 5 hours must receive a 30-minute unpaid meal break; employees working more than 10 hours must receive a second break

Required rest periods: employees must receive a 10-minute paid rest break for every 4 hours worked

The ABC test for independent contractor classification, which is very difficult to satisfy for workers performing core business functions

WARN Act obligations for layoffs affecting 50 or more employees (and other triggering events) with 60 days notice required

Pay transparency: employers with 15 or more employees must include pay ranges in job postings

California also has strong anti-retaliation protections, whistleblower protections, and robust enforcement mechanisms including the Private Attorneys General Act (PAGA), which allows employees to sue on behalf of themselves and other employees for labor code violations and to recover a portion of the civil penalties. PAGA litigation has become one of the most significant employment law risks for California employers.

New York employment law

New York City and New York State both impose requirements that go beyond federal law. State-level requirements include a minimum wage above the federal minimum (currently $16 per hour in New York City and surrounding counties), a paid family leave program funded by employee payroll deductions, and requirements for written pay notices to employees at hire. New York City adds pay transparency requirements (salary ranges in job postings), a ban on consideration of prior salary history in hiring decisions, and additional protections against discrimination.

Texas employment law

Texas employment law is notably less restrictive than California or New York. Texas follows the federal minimum wage of $7.25 per hour, has no state paid leave requirements beyond what federal law mandates, applies at-will employment broadly, and has no state income tax. For non-US founders who have flexibility in where their US team is located, Texas is often an attractive option from a compliance burden perspective. The tradeoffs are that the talent pool in Texas, while large, may be less deep in certain specialized technology sectors than in California or New York.

The multi-state complication

A company with remote employees across multiple states must comply with the employment law of each state where its employees work. This means tracking which state each employee works in, applying the most protective wage and hour rules for that state, maintaining separate state payroll registrations, and keeping current with state law changes that may affect any of the states in your footprint. As the remote workforce has grown, this multi-state compliance burden has become one of the more significant operational challenges for early-stage companies that hire nationally.

The practical solution is to be intentional about which states you hire in, particularly in the early stage. Starting with employees in one or two states and expanding gradually allows you to manage the compliance infrastructure in each state before adding more. Hiring immediately across ten states creates a compliance matrix that is difficult to manage without dedicated HR resources.

6. The Employer of Record Model

An Employer of Record (EOR) is a third-party organization that serves as the legal employer of your workers on paper while you direct their day-to-day work. The EOR handles all employer compliance obligations: payroll, payroll tax withholding and remittance, benefits administration, workers compensation, employment contracts, and HR compliance. You pay the EOR a fee per employee and direct the employees' work; the EOR manages everything else.

The EOR model has become significantly more common among non-US founders who want to hire US talent without immediately setting up their own US payroll infrastructure. It is also widely used for hiring employees in foreign countries where establishing a local entity would be impractical.

When the EOR model makes sense

The EOR model is most useful in the following situations:

• You want to hire US employees before your US entity is fully set up with payroll infrastructure

• You want to hire in a state where the compliance burden is high (such as California) and prefer to outsource the compliance to a specialist

• You are hiring only one or two US employees and the cost of setting up full payroll infrastructure does not justify the compliance overhead

• You want to move quickly and cannot afford the several weeks that setting up state payroll registrations, workers compensation, and benefits takes

• You are hiring internationally across multiple countries simultaneously and want a single platform to manage employment compliance in all of them

EOR providers

Deel offers Employer of Record (EOR) and contractor management services across more than 150 countries. Pricing is approximately from $599 per employee per month. It is best suited for founders who want a single platform for both global EOR and contractor payments. Pricing and country availability should always be checked directly with the provider before engagement.

Rippling provides EOR services together with a broader HR, payroll, IT, and benefits platform across more than 50 countries. Pricing generally starts from approximately $500 per employee per month, plus a base platform fee. It is often used by founders who want HR and operational systems integrated into one platform. Pricing and feature availability should be confirmed directly with the provider.

Remote.com provides EOR services in more than 180 countries, with pricing generally starting from approximately $599 per employee per month. It is commonly used by founders hiring internationally who want strong local compliance support. Current pricing and country coverage should always be verified directly with the provider.

Papaya Global offers EOR and international payroll services across more than 160 countries. Pricing generally starts from approximately $650 per employee per month. It is typically more suitable for larger teams with complex multi-country payroll requirements. Pricing and service scope should be checked directly with the provider.

Gusto is primarily a U.S. domestic payroll platform rather than a global EOR provider. Pricing generally starts from approximately $40 per month plus around $6 per employee. It is commonly used by founders hiring employees only within the United States who want a relatively cost-effective payroll solution. Current pricing and service availability should always be confirmed directly with the provider.

Limitations of the EOR model

The EOR model is not without trade-offs. Cost is the primary limitation: EOR fees of $500 to $700 per employee per month represent a meaningful additional cost on top of the employee's salary, particularly for high-salary technical roles. For a company with 20 or more US employees, the cumulative EOR cost typically exceeds the cost of building in-house payroll infrastructure, at which point the economics favor transitioning to direct employment.

There are also legal and practical complexities. The EOR is the employer of record, which means the employee has an employment relationship with the EOR, not with your company. This can create complications with equity grants, intellectual property assignment, non-compete agreements, and certain benefits. Some employees are uncomfortable with the EOR structure when they become aware of it, because their paystub and employment documents reflect the EOR's name rather than the company they work for day-to-day.

Most founders who start with an EOR for their first one to three US employees transition to direct employment once the headcount and the entity infrastructure justify it. The EOR serves as a bridge, not a permanent structure.

7. Compensation and Benefits: What US Employees Expect

Understanding US compensation norms is important for attracting and retaining US talent. The compensation package expected by a US employee differs significantly from what is standard in most other countries, and non-US founders who offer only a salary without considering the standard benefits package will find it difficult to compete for quality candidates.

Base salary benchmarking

US salaries vary enormously by role, industry, location, and experience level. The same software engineering role might command $120,000 in Austin, $180,000 in San Francisco, and $160,000 in New York. Location matters both because the cost of living varies and because local market rates vary.

Reliable salary benchmarking sources include the Bureau of Labor Statistics Occupational Employment and Wage Statistics, Levels.fyi for technology roles, LinkedIn Salary, Glassdoor, and Payscale. For specialized technical roles in major markets, compensation data from VC-backed startup compensation surveys such as Option Impact or Pave provide more relevant benchmarks than general market surveys.

Health insurance

Employer-sponsored health insurance is the most important component of the US employee benefits package. The United States does not have universal healthcare, and the cost of health insurance for an individual without employer coverage is substantial. Most full-time US employees expect their employer to provide health insurance, and the absence of health insurance is a significant competitive disadvantage in hiring.

Employers are not legally required to provide health insurance until they have 50 or more full-time equivalent employees, at which point the Affordable Care Act's employer mandate applies. However, competitive hiring typically requires offering health insurance well before reaching that threshold, particularly for professional and technical roles.

Health insurance is obtained through a broker or directly from an insurer. The employer typically pays a portion of the premium and the employee pays the remainder through pre-tax payroll deductions. Common plan types include HMOs, PPOs, and high-deductible health plans paired with Health Savings Accounts. Gusto and Rippling both offer health insurance brokerage services integrated with their payroll platforms, which simplifies administration for small employers.

Retirement plans

The most common employer-sponsored retirement plan in the US is the 401(k), a defined contribution plan that allows employees to defer a portion of their salary on a pre-tax or after-tax basis into an investment account. Employers frequently offer a matching contribution, typically 3% to 6% of salary, as a competitive benefit. The 401(k) matching contribution is a significant component of total compensation that candidates consider when comparing offers.

For early-stage companies with few employees, a SIMPLE IRA or SEP IRA may be more practical than a full 401(k) plan, which has higher administrative costs and more complex compliance requirements. Gusto and Guideline offer integrated 401(k) administration for small businesses at lower cost than traditional plan administrators.

Equity compensation

Equity compensation, specifically stock options or restricted stock units (RSUs), is a standard component of compensation at US technology startups and a key tool for aligning employee incentives with company growth. For a C-Corp, the standard equity vehicle is the Incentive Stock Option (ISO) under Section 422 of the IRC, which provides favorable tax treatment to US employees when specific holding period requirements are met.

Administering an equity compensation plan requires establishing a formal equity plan (typically an Incentive Stock Plan or Equity Incentive Plan), maintaining a cap table, issuing grant notices and option agreements, and tracking vesting, exercise, and termination events. Cap table management software such as Carta or Pulley automates much of this administration and produces the 409A valuations that are required annually to set the exercise price of ISO grants.

For LLCs, the equivalent of equity compensation is a profits interest grant, which is more complex to administer and less familiar to most employees than stock options. This is one of the practical reasons that C-Corps are preferred for companies planning to recruit from the US tech talent market.

Paid time off

Unlike most countries, the United States has no federal requirement for employers to provide paid vacation or paid time off. Paid time off is entirely at the employer's discretion, subject to any state requirements (California, for example, treats accrued vacation as wages that must be paid out on termination). Competitive employers in professional roles typically offer two to four weeks of paid vacation, paid federal holidays, and paid sick leave where required by state or local law. Unlimited PTO policies have become common at startups, though research suggests employees with unlimited PTO often take less time off than those with a defined allocation.

8. Hiring Foreign Nationals for US Roles

A non-US founder hiring for US-based roles will frequently encounter candidates who are themselves not US citizens or permanent residents. Whether and how your US entity can employ a foreign national in the United States depends entirely on that person's immigration status and work authorization.

Who is authorized to work in the US

The following categories of individuals are generally authorized to work in the United States without employer sponsorship: US citizens, US nationals, lawful permanent residents (green card holders), individuals with refugee or asylee status, individuals with certain temporary protected status designations, individuals with Employment Authorization Documents (EADs) issued under certain visa categories, and individuals authorized to work incident to their visa status (such as certain J-1 exchange visitors and L-2 spouses of L-1 visa holders).

The Form I-9 process described in Section 3 is how you verify each employee's work authorization. You are not required to sponsor foreign nationals for work visas, but you cannot employ anyone who is not authorized to work in the US, regardless of their qualifications.

Visa sponsorship: the H-1B and other options

If you want to hire a foreign national who is not otherwise authorized to work in the US, your company must sponsor them for a work visa. The most common work visa for professional roles is the H-1B, which requires the employee to have at least a bachelor's degree or equivalent in a specialty field related to the position. The H-1B is subject to an annual cap of 65,000 new visas (plus 20,000 for US master's degree holders, there are other exceptions), and demand significantly exceeds supply each year. The selection process is by random lottery, meaning sponsoring an H-1B does not guarantee a visa.

Other work visa categories that may be relevant include the O-1 for workers with extraordinary ability in their field, the L-1 for intracompany transferees (moving an employee from a related foreign entity to the US entity), the TN for Canadian and Mexican nationals under the USMCA, and the E-3 for Australian nationals in specialty occupations. Each category has specific eligibility requirements, processing timelines, and costs.

Visa sponsorship usually requires working with an immigration attorney. The costs include attorney fees, USCIS filing fees (which vary by visa category and can range from several hundred to several thousand dollars), and in some cases premium processing fees for faster adjudication. The employer bears most of these costs by law for H-1B visas. The process is time-consuming and uncertain, and founders should plan for timelines of several months from initiation to approval.

Do not give immigration advice: As an employer, your role is to verify work authorization through the I-9 process and, if you choose to sponsor visas, to work with an immigration attorney. You should not advise employees on their immigration status or options, tell employees whether they qualify for a particular visa category, or make hiring decisions based on citizenship or national origin. Refer any employee immigration questions to a qualified immigration attorney.

9. Managing HR Compliance on an Ongoing Basis

Hiring is the beginning of an ongoing HR compliance obligation that continues for as long as you have employees. The obligations evolve as your headcount grows, as employment laws change, and as your employee mix changes. Managing these obligations without a dedicated HR function requires systems and discipline.

Employee handbook

An employee handbook documents your company's policies, procedures, and expectations. It covers topics such as the code of conduct, anti-harassment and anti-discrimination policies, time off policies, expense reimbursement, confidentiality, use of company equipment and systems, disciplinary procedures, and the dispute resolution process. A well-drafted handbook serves multiple purposes: it informs employees of their rights and obligations, it protects the company in employment disputes by demonstrating that policies were communicated, and it satisfies some state law requirements for written policy notices.

Employee handbooks should be reviewed annually and updated whenever relevant laws change or company policies evolve. Outdated handbooks that no longer reflect current law can actually create liability by promising employees rights they do not have under the current policy or by imposing restrictions that are no longer enforceable. Most employment attorneys offer handbook review services, and several HR software platforms include handbook builders with state-specific legal compliance.

Performance management and termination

At-will employment means you can terminate an employee at any time for any legal reason, but managing terminations poorly creates legal risk even in an at-will state. Documenting performance issues, providing clear feedback, following a consistent process, and treating similarly situated employees consistently are practices that both help the employee understand what is expected and protect the company if a termination is later challenged.

Wrongful termination claims can be brought even in at-will states when the termination violates anti-discrimination law, retaliates against protected activity such as filing a workers compensation claim or reporting a workplace safety violation, or breaches a specific contractual commitment. Having documentation of the performance issues that led to a termination, and having treated the terminated employee consistently with how you have treated others in similar situations, is the best protection against these claims.

California, in particular, has a robust private right of action for employees through PAGA, which allows a single terminated employee to bring a representative action on behalf of all current and former employees for labor code violations, with significant potential damages. Taking California terminations particularly seriously, and consulting an employment attorney before terminating a California employee who may have a grievance, is a sound practice.

Regular payroll and HR audits

Scheduling an annual review of your payroll and HR compliance is a practical way to catch issues before they become enforcement actions. The review should include: confirming that all employees have current, valid Form I-9s on file, verifying that employee classifications as exempt or non-exempt are still accurate given any changes in duties or compensation, confirming that contractor classifications are still defensible for any workers classified as contractors, reviewing state registrations to confirm they are current in all states where employees work, and confirming that workers compensation coverage is in place and covers all employees.

Many employment attorneys offer compliance audits as a service, typically reviewing I-9 records, classification decisions, and policy documents for a flat fee. For a company at the stage where HR compliance is becoming complex, an annual external audit is a cost-effective way to identify and address gaps before a regulator does.

Before you move to Part 11

Part 11 covers intellectual property and contracts: protecting your IP through the US entity, the most important contract types for a US business, how US contract law differs from what you may be familiar with from other jurisdictions, and the specific considerations for foreign-owned entities in commercial contracting.

Before you move on, confirm that the following from this part are addressed:

• Every person working for your US business has been correctly classified as an employee or independent contractor under both the IRS standard and the applicable state test

• Independent contractor agreements are in place with all contractors, including IP assignment and confidentiality provisions

• Form W-9 has been collected from all US-based contractors before payment was made

• Form W-8BEN or W-8BEN-E has been collected from all foreign contractors before payment was made

• All employees have completed Form I-9 with original documents examined and recorded within three business days of their start date

• Payroll is set up and compliant in every state where employees work

• Workers compensation insurance is in place in every state where you have employees

• New hire reporting has been filed in each applicable state

• Your compensation and benefits package is competitive for the roles and markets you are hiring in

• If you are using an EOR, you understand the transition plan to direct employment as headcount grows

Antravia Advisory: The hiring decision is where the cost of getting the classification wrong and the complexity of state-by-state compliance converge. If you are about to make your first US hire and are not certain whether the person should be classified as an employee or contractor, or which state compliance obligations will apply, getting that assessment done before the first paycheck is issued is significantly less expensive than correcting it after the fact.

Continue to Part 11: Intellectual Property and Contracts

About Antravia Advisory

Antravia Advisory is a US-based tax and accounting advisory firm headquartered in Winter Park, Florida, operating nationally and internationally.

We advise international businesses entering the United States and complex US companies operating across multiple states, entities, and revenue structures. Our work spans advanced tax strategy, multi-state sales tax oversight, cross-border structuring, and high-level accounting architecture for e-commerce brands, subscription and SaaS businesses, platform-based models, and multi-entity groups.

We work with founders and leadership teams who require technical precision, structural clarity, and financial frameworks built for scale, capital events, and long-term resilience.

The Non-US Founder’s Complete Guide to Running a US Business

Part 1 — Before You Start

Part 2 — Choosing Your US Entity

Part 3 — Formation

Part 4 — US Banking

Part 5 — US Federal Tax

Part 6 — US State Tax

Part 7 — Paying Yourself

Part 8 — Accounting and Bookkeeping

Part 9 — Annual Compliance Calendar

Part 10 — Hiring in the US

Part 11 — Intellectual Property and Contracts

Part 12 — Your Home Country Obligations

Part 13 — Applied Business Types

Part 14 — Exiting, Winding Down, or Restructuring

Disclaimer:

Content published by Antravia is provided for informational purposes only and reflects research, industry analysis, and our professional perspective. It does not constitute legal, tax, or accounting advice. Regulations vary by jurisdiction, and individual circumstances differ. Readers should seek advice from a qualified professional before making decisions that could affect their business.

See also our Disclaimer page

Antravia Advisory

Accounting built for complexity

Not legal advice, always verify with your Accountant

Email:

Contact us:

© 2025. All rights reserved. | Disclaimer | Privacy Policy | Terms of Use |

contact@antravia.com

Antravia LLC

941 W Morse Blvd suite 100

Winter Park

Florida

32789