Part 8: Accounting and Bookkeeping

The Non-US Founder's Complete Guide to Running a US Business - Part 8, explains accounting and bookkeeping for foreign-owned U.S. entities, including GAAP vs cash and accrual methods, software selection, intercompany tracking, foreign currency accounting, Form 5472 readiness, and recordkeeping requirements.

THE NON-US FOUNDER'S COMPLETE GUIDE TO RUNNING A US BUSINESS

3/22/202623 min read

Accounting and bookkeeping are the infrastructure on which everything else in this guide depends. Your tax filings rely on your books. Your transfer pricing documentation relies on your books. Your Form 5472 reporting relies on your books. Your ability to pay yourself correctly, file payroll tax accurately, and demonstrate arm's length intercompany pricing all trace back to whether your financial records are complete, current, and structured correctly.

For a non-US founder, bookkeeping has additional complexity that domestic guides do not address: transactions occur in multiple currencies, intercompany movements between the US entity and a foreign entity need to be tracked separately and reported to the IRS, and the chart of accounts needs to be structured to support both US tax filing requirements and any home country reporting the founder's foreign entity needs. Getting this infrastructure right at the start is significantly less expensive than rebuilding it retroactively when a tax filing or an audit forces the issue.

This part covers the accounting standards applicable to your US entity, how to choose and configure bookkeeping software, chart of accounts design for foreign-owned entities, intercompany transaction recording, foreign currency accounting, what records you must retain and for how long, and how to manage the relationship between your US bookkeeping and your home country reporting.

1. Accounting Standards: What your US Entity is required to follow

The United States uses Generally Accepted Accounting Principles (GAAP) as its primary accounting standard framework, administered by the Financial Accounting Standards Board (FASB). International Financial Reporting Standards (IFRS), used in the UK, EU, Australia, and many other countries, are not generally accepted for US domestic financial reporting purposes.

For most early-stage foreign-owned US entities, the practical question is not which standard to adopt for statutory purposes but rather which basis of accounting to use for internal records and tax compliance. The two choices are cash basis accounting and accrual basis accounting.

Cash basis accounting

Under the cash basis, revenue is recorded when cash is received and expenses are recorded when cash is paid. It is simple, intuitive, and easy to reconcile to bank statements. For very small businesses with uncomplicated transaction patterns, it provides a clear picture of actual cash flow.

However, cash basis accounting has limitations. It can distort the picture of business performance when there are significant timing differences between when work is performed and when payment is received, or between when an expense is incurred and when it is paid. It also does not comply with GAAP, which means it is not suitable for entities that need audited or reviewed financial statements for investors, lenders, or regulatory purposes.

Accrual basis accounting

Under the accrual basis, revenue is recorded when it is earned (when the obligation to the customer is satisfied) and expenses are recorded when they are incurred (when the obligation to the vendor arises), regardless of when cash actually changes hands. Accrual accounting provides a more accurate picture of the entity's financial position and performance over time and is required for GAAP compliance.

For US tax purposes, most C-Corporations (Many corporations (including C-Corps) can use cash basis if average gross receipts are below ~$30 million (indexed)) and larger businesses are required to use the accrual method. Small businesses below a gross receipts threshold may be permitted to use the cash method for tax purposes. For many early-stage single-member LLCs, the cash method is acceptable for tax filing. However, starting on the accrual basis from the beginning is generally advisable for any entity that expects to grow, seek investment, or have complex intercompany transactions, because converting from cash to accrual later requires restating prior period records and can be time-consuming and costly.

Recommendation: Use accrual basis accounting from day one if your entity has intercompany transactions with a related foreign entity, expects to seek investor funding, will be subject to transfer pricing requirements, or anticipates significant timing differences between billing and payment. For a simple consulting LLC with straightforward revenue and minimal expenses, cash basis is manageable in the early stage, but plan for the eventual conversion.

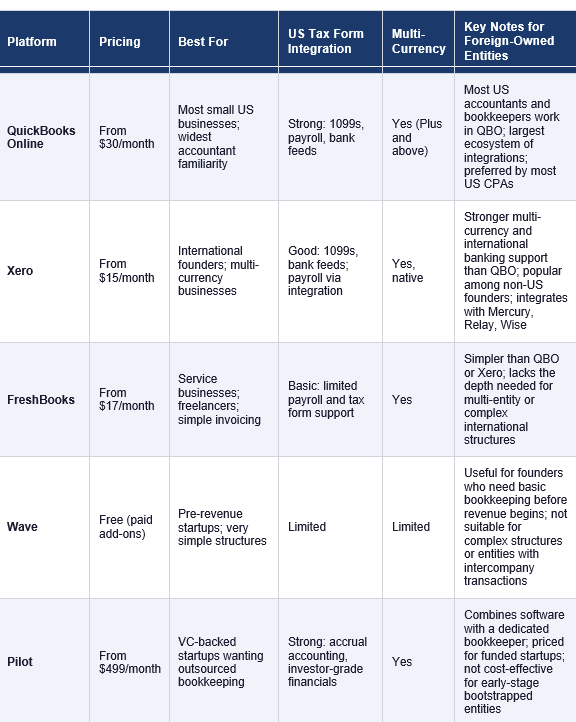

2. Choosing Your Bookkeeping Software

The bookkeeping software you choose determines how easy or difficult every downstream task becomes: tax preparation, Form 5472 reporting, payroll reconciliation, intercompany transaction tracking, and financial statement production. For a foreign-owned US entity, the decision involves considerations that do not apply to a domestically owned business.

The two most important questions are: does the software handle multi-currency transactions properly, and does it integrate with the banking platforms that foreign-owned entities typically use, specifically Mercury, Relay, and Wise. Secondary considerations are the software's familiarity to US accountants and tax preparers, its 1099 contractor payment tracking capability, and its payroll integration options.

QuickBooks Online vs. Xero: the core decision

For most non-US founders, the real choice is between QuickBooks Online and Xero. Both are capable platforms that can handle the accounting requirements of a foreign-owned US entity. The decision between them typically comes down to two factors: who your US accountant uses, and how important native multi-currency capability is to your operations.

QuickBooks Online is the dominant platform in the US market. The overwhelming majority of US-based bookkeepers, accountants, and tax preparers are fluent in QBO. If you are engaging a US CPA or enrolled agent to prepare your tax returns, the probability that they prefer QBO is high. Working in the same platform as your tax preparer simplifies the year-end handoff and reduces the time spent on data transfer and reconciliation.

Xero has stronger multi-currency capabilities built into its standard plans and has historically been more popular among international businesses and founders based outside the US. Its integration with Mercury, Relay, and Wise is clean and well-maintained. If you are managing a business with significant foreign currency transactions, regular intercompany settlements between a US entity and a foreign entity, or a home country accounting team that already uses Xero, it may be the better operational fit.

The decision is not irreversible, but migrating between platforms mid-stream is disruptive. Make a deliberate choice based on your specific circumstances and stick with it through at least your first full tax year.

Connecting your banking to your bookkeeping

Every bookkeeping platform offers bank feed integration: a direct connection to your bank account that imports transactions automatically, reducing manual data entry and the errors that come with it. For foreign-owned entities using Mercury or Relay, both platforms have native integrations with QBO and Xero that import transactions in real time. Wise also integrates with both platforms, which is important if you are using Wise for international payments and want those transactions captured in your bookkeeping without manual entry.

Setting up bank feeds on day one, before your first transaction, is the cleanest approach. Importing historical transactions retroactively is possible but requires more time to categorize and reconcile correctly. Treat the bank feed setup as part of your initial entity setup, not as something to address later.

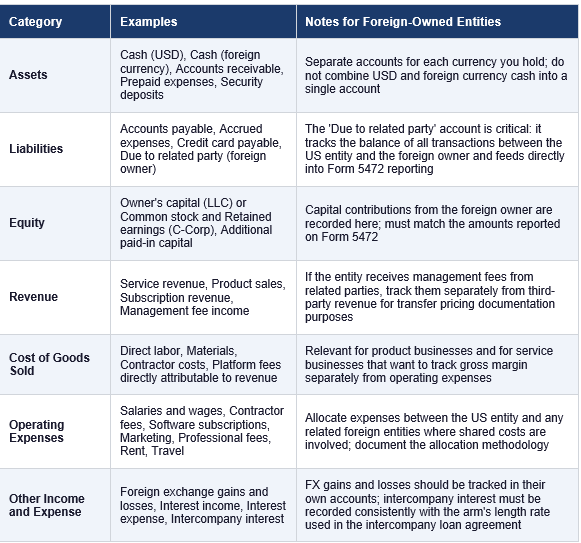

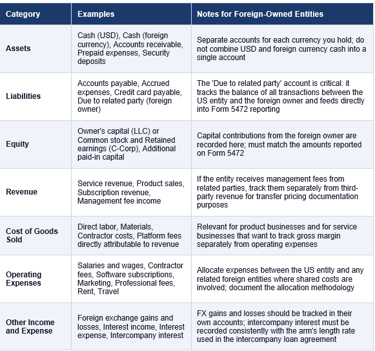

3. Chart of Accounts Design for Foreign-Owned US Entities

The chart of accounts is the organizational structure of your bookkeeping system: the list of categories into which every transaction is classified. A well-designed chart of accounts makes tax preparation faster, transfer pricing documentation easier, and financial reporting more useful. A poorly designed one creates confusion, misclassification, and downstream problems that are expensive to untangle.

For a foreign-owned US entity, the chart of accounts needs to do several things that a standard domestic template does not address: it needs to track intercompany transactions separately, handle multiple currencies, and produce information that directly supports Form 5472 reporting.

The intercompany accounts: the most important design decision

The most important chart of accounts decision for a foreign-owned entity is how to structure the intercompany accounts. These are the accounts that track all transactions between the US entity and its foreign owner or related foreign entities. They need to be set up correctly from the start because they feed directly into Form 5472 reporting and, for entities with management fee arrangements, into transfer pricing documentation.

The recommended approach is to create a separate account for each type of intercompany transaction. At minimum, you need accounts for: capital contributions received from the foreign owner, distributions paid to the foreign owner, management fees paid to or received from related foreign entities, intercompany loans (both the principal balance and the accrued interest), and any intercompany expense allocations. Having these in separate accounts rather than combined into a single intercompany account makes the Form 5472 categorization straightforward and provides a clean audit trail.

Common mistake: Many founders set up a single intercompany account and record all transactions between the US entity and the foreign owner into that account. When Form 5472 preparation time comes, every transaction in that account needs to be reviewed and categorized by type. This is workable for a small number of transactions but becomes time-consuming as the volume grows. Separate accounts from day one eliminate this problem entirely.

4. Recording Intercompany Transactions Correctly

Intercompany transactions are the transactions most likely to create compliance problems for foreign-owned US entities, and they are the transactions most likely to be recorded incorrectly in standard bookkeeping systems that were not designed with foreign ownership in mind. This section covers the specific recording requirements for each common intercompany transaction type.

Capital contributions

When the foreign owner contributes cash to the US LLC, the transaction is recorded as a debit to Cash and a credit to Owner's Capital (for an LLC) or Additional Paid-In Capital (for a C-Corp). The amount must be recorded in US dollars. If the contribution is made in a foreign currency, it must be converted to USD at the spot exchange rate on the date of the transfer. The foreign currency amount, the exchange rate used, and the source of the rate should all be documented.

The same transaction must be reported on Form 5472 as a reportable transaction in the category of contributions by the foreign owner to the reporting corporation. The amount reported on Form 5472 must match the amount recorded in the books.

Distributions to the foreign owner

When the US LLC transfers cash to the foreign owner, the transaction is recorded as a debit to Owner's Capital or a designated distributions account, and a credit to Cash. If the distribution is made in a foreign currency (for example, a wire to the owner's foreign bank account), it is recorded in USD at the spot rate on the date of transfer, and the difference between the USD amount sent and any FX conversion gain or loss is recorded in the FX gain or loss account.

Distributions are also reportable on Form 5472. Maintaining a running record of all distributions during the year, with dates and USD amounts, makes the annual Form 5472 preparation straightforward.

Management fees

If the US entity pays a management fee to a related foreign entity, the transaction is recorded as a debit to Management Fee Expense and a credit to Cash or Accounts Payable (if the invoice has been received but not yet paid). If the foreign entity invoices in a foreign currency, the invoice is recorded at the spot rate on the invoice date, and any difference between the invoice rate and the payment rate is recorded as an FX gain or loss.

Management fees paid to related foreign entities are reportable on Form 5472 and should be included in the intercompany services agreement and transfer pricing documentation described in Part 7. The amount recorded in the books must match the amounts reported on both Form 5472 and in the transfer pricing documentation. Inconsistencies between these sources are a red flag in an IRS examination.

Intercompany loans

If the US entity borrows from or lends to the foreign owner, the loan principal is recorded as a liability (Due to Related Party) or asset (Note Receivable from Related Party) on the US entity's books. Interest accrues on the loan at the arm's length rate specified in the loan agreement and is recorded as interest expense or interest income in each accounting period, regardless of when cash is actually paid or received. The accrued but unpaid interest balance is tracked in an accrued interest account.

Both the principal and the interest are reportable on Form 5472: the principal as a loan from the foreign owner, and the interest payments as amounts paid to the foreign related party. Failing to record accrued interest correctly is one of the most common bookkeeping errors for entities with intercompany loans, and it creates discrepancies between the books and the Form 5472 that are difficult to explain in an audit.

5. Foreign Currency Accounting

Foreign currency accounting is one of the most technically complex areas of bookkeeping for international businesses and one of the least well-handled by founders who are managing their own books. The core principle is straightforward: your US entity's functional currency is the US dollar, and all transactions must ultimately be recorded in US dollars. But the mechanics of how non-USD transactions are converted, and what happens to the differences that arise from exchange rate movements, require specific treatment.

Functional currency vs. reporting currency

Your US entity's functional currency is the currency of the primary economic environment in which it operates. For a US entity that earns revenue primarily in USD and incurs most of its expenses in USD, the functional currency is USD. If your US entity earns revenue primarily in a foreign currency, the functional currency analysis becomes more complex, but for most early-stage foreign-owned US entities with US customers and USD revenue, functional currency is USD.

Your reporting currency is the currency in which you prepare your financial statements. For a US entity, the reporting currency is USD. Foreign currency transactions are translated into USD for recording and reporting purposes.

Transaction-date recording

Every transaction denominated in a foreign currency must be recorded in USD at the exchange rate on the date of the transaction. If you receive a GBP invoice from a related UK entity on March 15 and pay it on April 10, the liability is recorded at the March 15 exchange rate and the payment is recorded at the April 10 exchange rate. The difference between these two amounts is an unrealized exchange gain or loss from March 15 to March 31 (if your reporting period ends then), and a realized exchange gain or loss on the April 10 payment date.

Period-end remeasurement

At the end of each accounting period, monetary assets and liabilities denominated in foreign currencies (cash balances in foreign currency accounts, foreign currency receivables, and foreign currency payables) must be remeasured at the period-end exchange rate. The difference between the exchange rate at which the transaction was originally recorded and the period-end rate is recorded as an unrealized foreign exchange gain or loss. This gain or loss flows through the income statement and affects taxable income.

For an entity that regularly holds significant foreign currency balances, period-end remeasurement can produce meaningful income statement volatility. Exchange rate movements of even a few percent on a large balance create gains and losses that affect both the financial statements and the tax liability. Understanding this dynamic, and planning for it, is part of managing a business with multi-currency exposure.

Choosing and consistently applying exchange rates

The IRS requires that foreign currency amounts be translated using a consistent methodology. The two most common approaches are the spot rate on the transaction date and the average exchange rate for the period. The IRS generally accepts the use of published exchange rates, including the official exchange rates published by the Treasury's Bureau of the Fiscal Service and the rates published by the Federal Reserve. Using a consistent source and documenting the rate used for each transaction is important for audit defense.

Most bookkeeping platforms that support multi-currency transactions handle the exchange rate application automatically, pulling rates from a standard source and applying them to transactions as they are recorded. Verify that your platform is pulling rates from a recognized source and that you understand how it handles period-end remeasurement before relying on its output for tax purposes.

FX gains and losses and taxable income

Realized foreign exchange gains and losses, meaning those that arise when a foreign currency transaction is settled at a different rate from the rate at which it was originally recorded, are generally taxable as ordinary income or deductible as ordinary business expenses. Unrealized gains and losses from period-end remeasurement may be included in taxable income for accrual-basis taxpayers but excluded for cash-basis taxpayers. Specifically, FX treatment depends on: Section 988 rules, whether the item is monetary, whether gain/loss is realized vs unrealized

The tax treatment of FX gains and losses for non-US founders interacts with the home country treatment of the same items. Whether your home country recognizes the same FX gains and losses in the same period, and whether the foreign tax credit mechanism provides relief for tax paid on FX income in the US, depends on your home country's specific rules. This is an area where coordination between your US and home country advisors is important.

6. Bookkeeping Specifically Designed for Form 5472 Compliance

Form 5472 is the filing obligation that most foreign-owned US entities are least prepared for, and good bookkeeping practice is the most effective way to ensure that the form can be completed accurately and on time every year. This section covers the specific bookkeeping disciplines that make Form 5472 preparation straightforward rather than a scramble.

The reportable transactions log

The single most useful bookkeeping tool for Form 5472 compliance is a running log of all reportable transactions between the US entity and the foreign owner or any other related foreign parties. A reportable transaction is any exchange of money, property, or services between the reporting entity and any 25% foreign shareholder or any related party. The log should capture: the date of the transaction, the parties involved, the type of transaction, the amount in USD, and a brief description.

This log can be maintained in your bookkeeping software by filtering transactions tagged to the intercompany accounts described in Section 3. At year end, the accountant preparing Form 5472 should be able to pull the log directly from the bookkeeping system without needing to reconstruct it from bank statements. If your bookkeeping system does not produce this log cleanly, maintaining a separate spreadsheet as a supplement is acceptable, but the primary records must be in the books.

Matching book records to Form 5472 categories

Form 5472 requires reporting by transaction category: sales, purchases, rents, royalties, interest paid, interest received, services rendered, services received, commissions paid, commissions received, premiums paid, and other amounts. Your chart of accounts should map cleanly to these categories. If you have a management fee expense account, it corresponds to the services received category. If you have an intercompany interest expense account, it corresponds to the interest paid category.

Before your first Form 5472 filing, review your chart of accounts against the Form 5472 categories and confirm that every account type that will contain intercompany transactions maps to a specific Form 5472 line. Adjusting the chart of accounts before transactions begin is simple. Reclassifying transactions after year end to match Form 5472 categories is time-consuming and error-prone.

7. Working with a US Bookkeeper or Accountant

Most non-US founders at the early stage manage their own bookkeeping using one of the platforms described in Section 2. This is entirely feasible for a simple entity with limited transactions, but there are stages at which engaging a professional becomes both practical and cost-effective.

When to manage your own bookkeeping

Self-managed bookkeeping is appropriate when your entity has a limited number of transactions per month, your revenue streams are straightforward, you have no employees, intercompany transactions are minimal and easy to categorize, and you are comfortable with the bookkeeping software you have chosen. Many founders in the first year of operations, particularly those running a single-member LLC providing services to a small number of US clients, can maintain their books adequately without professional assistance.

When to engage a bookkeeper

The typical triggers for engaging a professional bookkeeper are: transaction volume growing beyond what you can manage in a reasonable amount of time each week, introduction of payroll, intercompany transactions that require careful categorization for Form 5472 purposes, the need to produce financial statements for investors or lenders, or preparation for an audit or due diligence process. A bookkeeper typically handles transaction categorization, bank reconciliation, accounts receivable and payable tracking, and month-end close processes, but does not prepare tax returns.

The accountant relationship

Your US accountant, whether a CPA or an enrolled agent, prepares your tax returns and provides tax planning advice. The accountant works from the financial records the bookkeeper maintains. The quality of the bookkeeping directly affects the quality and efficiency of the tax preparation: an accountant working from well-organized, correctly categorized books produces accurate returns faster and at lower cost than one who must first reconstruct the records.

For a foreign-owned US entity, the US accountant needs to understand international tax. Not every US CPA has meaningful experience with Form 5472, foreign-owned disregarded entities, transfer pricing documentation, or the interaction between US and foreign tax systems. When engaging a US accountant, confirm their experience with foreign-owned entities and specifically with the filing requirements that apply to your structure before committing to the relationship.

Briefing your US accountant: what they need to know

Before your first US tax filing, give your US accountant a complete picture of your structure and situation. This means explaining: the ownership structure of the US entity and who the foreign owner is, any related foreign entities and their relationship to the US entity, a description of intercompany transactions that occurred during the year, your home country tax position and whether you have a home country accountant who will also be filing, any tax treaties you believe apply to your situation, and your own tax residency status in both the US and your home country.

An accountant who understands the full picture from the start can provide more useful advice, identify issues before they become problems, and coordinate with your home country advisor where cross-border questions arise. An accountant who learns about the foreign ownership structure only at filing time is working with incomplete information and may miss issues that a full briefing would have surfaced.

8. Month-End and Year-End Close Process

A close process is the set of steps you complete at the end of each accounting period to ensure your books are complete, accurate, and reconciled before you move on. For small entities managed by a single founder, a monthly close is not always practical, but a quarterly close at minimum, and a thorough year-end close, are essential.

Month-end close checklist

• Reconcile all bank accounts: confirm that every transaction in your bank statement has been recorded in your bookkeeping software and that the ending balance matches

• Reconcile all credit card accounts: same process for any business credit cards

• Review and categorize any uncategorized transactions: do not carry uncategorized transactions forward to the next period

• Record any accrued expenses not yet reflected in the books: accrued interest on intercompany loans, accrued professional fees, subscription renewals

• Record intercompany transactions and confirm they are categorized correctly against the Form 5472 transaction log

• Remeasure any foreign currency balances at the period-end exchange rate and record the resulting FX gain or loss

• Review accounts receivable aging: follow up on any overdue invoices and assess whether any receivables need to be written off

• Review accounts payable: confirm all vendor invoices have been recorded and that nothing due has been missed

Year-end close checklist

The year-end close extends the month-end process with additional steps required for annual compliance:

• Complete all month-end steps for December

• Compile the full Form 5472 transaction log for the year and cross-reference against book records

• Prepare or confirm the fixed asset schedule: additions, disposals, and depreciation for the year

• Confirm payroll records are complete: all W-2s and 1099-NECs must be prepared and issued by January 31

• Review all intercompany accounts and confirm they reconcile with the corresponding records in the related foreign entity's books

• Confirm management fee invoices for the year match the intercompany services agreement and the amounts recorded in both entities' books

• Produce a trial balance and review for any unusual items, large year-over-year variances, or accounts with unexpected balances

• Confirm your estimated tax payments for the year and compare the total to the expected tax liability to assess whether a top-up payment is needed before the filing deadline

• Provide the completed year-end package to your US accountant: trial balance, transaction detail by account, bank statements, Form 5472 transaction log, payroll records, and intercompany documentation

Timing: The Form 5472 and pro forma Form 1120 are due by the extended deadline for Form 1120, which is generally September 15 for calendar-year entities. However, preparing the underlying records on which Form 5472 depends should not wait until August. Completing the year-end close in January or February gives your accountant adequate time to prepare the returns without rushing.

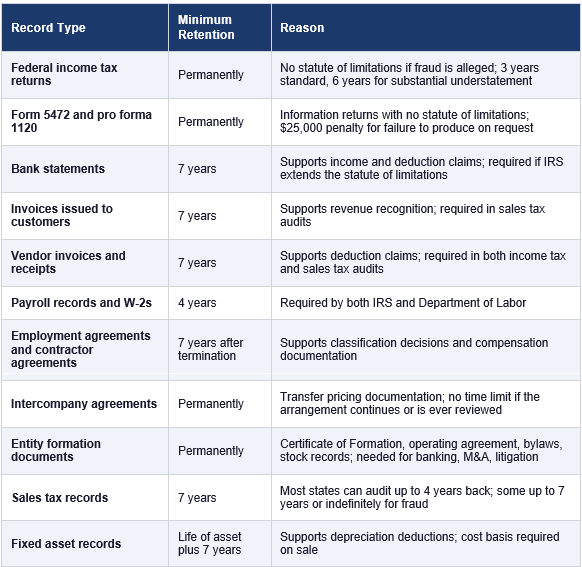

9. Records Retention: What to keep and for how long

Maintaining complete and organized records is a legal requirement, not just good practice. The IRS can examine returns for up to three years after filing in the standard case, six years if income was substantially understated, and indefinitely in cases involving fraud or when no return was filed. State tax authorities have their own statute of limitations, which in some states extends to seven years or more.

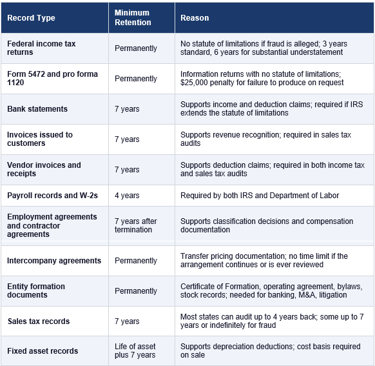

8. Month-End and Year-End Close Process

A close process is the set of steps you complete at the end of each accounting period to ensure your books are complete, accurate, and reconciled before you move on. For small entities managed by a single founder, a monthly close is not always practical, but a quarterly close at minimum, and a thorough year-end close, are essential.

Month-end close checklist

• Reconcile all bank accounts: confirm that every transaction in your bank statement has been recorded in your bookkeeping software and that the ending balance matches

• Reconcile all credit card accounts: same process for any business credit cards

• Review and categorize any uncategorized transactions: do not carry uncategorized transactions forward to the next period

• Record any accrued expenses not yet reflected in the books: accrued interest on intercompany loans, accrued professional fees, subscription renewals

• Record intercompany transactions and confirm they are categorized correctly against the Form 5472 transaction log

• Remeasure any foreign currency balances at the period-end exchange rate and record the resulting FX gain or loss

• Review accounts receivable aging: follow up on any overdue invoices and assess whether any receivables need to be written off

• Review accounts payable: confirm all vendor invoices have been recorded and that nothing due has been missed

Year-end close checklist

The year-end close extends the month-end process with additional steps required for annual compliance:

• Complete all month-end steps for December

• Compile the full Form 5472 transaction log for the year and cross-reference against book records

• Prepare or confirm the fixed asset schedule: additions, disposals, and depreciation for the year

• Confirm payroll records are complete: all W-2s and 1099-NECs must be prepared and issued by January 31

• Review all intercompany accounts and confirm they reconcile with the corresponding records in the related foreign entity's books

• Confirm management fee invoices for the year match the intercompany services agreement and the amounts recorded in both entities' books

• Produce a trial balance and review for any unusual items, large year-over-year variances, or accounts with unexpected balances

• Confirm your estimated tax payments for the year and compare the total to the expected tax liability to assess whether a top-up payment is needed before the filing deadline

• Provide the completed year-end package to your US accountant: trial balance, transaction detail by account, bank statements, Form 5472 transaction log, payroll records, and intercompany documentation

Timing: The Form 5472 and pro forma Form 1120 are due by the extended deadline for Form 1120, which is generally September 15 for calendar-year entities. However, preparing the underlying records on which Form 5472 depends should not wait until August. Completing the year-end close in January or February gives your accountant adequate time to prepare the returns without rushing.

9. Records Retention: What to keep and for how long

Maintaining complete and organized records is a legal requirement, not just good practice. The IRS can examine returns for up to three years after filing in the standard case, six years if income was substantially understated, and indefinitely in cases involving fraud or when no return was filed. State tax authorities have their own statute of limitations, which in some states extends to seven years or more.

How to organize and store records

The organizational system matters less than the consistency with which it is applied. A simple folder structure with a folder for each year, subfolders for each entity, and within those subfolders organized by record type, maintained in a cloud storage system with regular backups, is entirely adequate. More important than the system is the discipline of filing documents when they are created rather than accumulating a backlog that becomes difficult to organize retroactively.

For original signed documents, such as executed operating agreements, stock purchase agreements, and intercompany loan agreements, maintain both a digital copy and a secure physical copy. If the original is ever challenged, having a physical original is stronger than a scan, though a well-maintained scan is far better than no record at all.

Document requests during an audit

If the IRS examines your return or a state revenue agency conducts a sales tax audit, they will issue document requests specifying what they want to see and the time frame in which you must respond. The ability to respond promptly with organized, complete records significantly reduces the time and cost of an audit. An audit that requires weeks of record reconstruction from bank statements, email threads, and fragmented files takes far longer and costs far more in professional fees than one where the records are ready to produce.

When the IRS requests records related to Form 5472 specifically, the penalty for failure to produce records is an additional $25,000 per failure, separate from the filing penalty. This makes the Form 5472 transaction log and the underlying intercompany records the single most important records to maintain and to be able to produce quickly.

10. Coordinating US Bookkeeping with Home Country Reporting

Running a US entity as a non-US founder almost always creates a need to coordinate between your US bookkeeping and your home country reporting. The nature of that coordination depends on your home country, your entity structure, and how your home country treats the US entity's income.

Information your home country accountant needs from US books

At minimum, your home country accountant will need the following information from your US entity's books to prepare your home country returns:

• Total revenue earned by the US entity during the year

• Total distributions received from the US entity during the year, in both USD and home currency amounts

• Any management fees paid from the US entity to your home country entity

• Any intercompany loans between the US entity and home country entities, including interest paid or received

• The ending balance of the US entity's equity attributable to you

• US tax paid or withheld during the year, including any withholding on dividends or FDAP income

The form in which this information is needed depends on your home country accountant's requirements and your home country's tax system. Some home country accountants will ask for a full set of US financial statements. Others will work from a summary of the key figures. Establishing this expectation in the first year of operations, rather than discovering it at home country filing time, avoids delays.

Currency translation for home country reporting

Your home country financial reporting will be in your home country's currency. US entity figures reported to your home country accountant need to be translated from USD. The translation rate used depends on your home country's rules: average rate for the year for income items, year-end rate for balance sheet items is the most common approach, but confirm with your home country accountant what their specific requirements are.

Keeping a record of the exchange rates you used for each reporting period, with a reference to the source of those rates, provides a clear audit trail if either the IRS or your home country tax authority asks about the translation methodology used.

Avoiding double reporting or missed reporting

One of the practical risks in managing books across two jurisdictions is that a transaction gets reported in one jurisdiction but not the other, or gets reported twice in both. The most common version of this problem is a distribution from the US LLC that is correctly recorded in the US books but not communicated to the home country accountant, resulting in the distribution being missed from the home country return.

The solution is a year-end reconciliation step specifically for intercompany items: a confirmation that every transaction recorded in the US entity's intercompany accounts has a corresponding entry in the home country entity's books, and that the amounts in both sets of books are consistent after translation. This step, added to the year-end close checklist, prevents most cross-border reporting discrepancies before they become issues.

Before you move to Part 9

Part 9 covers annual compliance: a consolidated calendar of every federal and state filing obligation your US entity has across the full calendar year, with practical guidance on how to manage the compliance process without letting deadlines slip.

Before you move on, confirm that the following from this part are in place:

• You have selected your bookkeeping software and connected your US bank account via bank feed

• Your chart of accounts has separate accounts for each type of intercompany transaction and maps to Form 5472 reporting categories

• You have chosen accrual or cash basis accounting and documented the decision

• You have a system for recording foreign currency transactions at the correct exchange rate and for tracking FX gains and losses

• Your year-end close process includes preparation of the Form 5472 transaction log

• Your records retention system is set up and you have confirmed which records need to be kept permanently

• Your US accountant has been briefed on the full ownership structure, intercompany arrangements, and home country tax position

• Your home country accountant knows what information to expect from the US entity each year

Antravia Advisory: Bookkeeping for a foreign-owned US entity is more complex than standard domestic bookkeeping, and the consequences of getting it wrong, specifically the Form 5472 penalties and the transfer pricing documentation gaps, are disproportionately expensive relative to the cost of getting it right from the start. If you are setting up your US entity's accounting infrastructure and want to make sure it is built to support your compliance obligations, we can help.

Continue to Part 9: Annual Compliance

About Antravia Advisory

Antravia Advisory is a US-based tax and accounting advisory firm headquartered in Winter Park, Florida, operating nationally and internationally.

We advise international businesses entering the United States and complex US companies operating across multiple states, entities, and revenue structures. Our work spans advanced tax strategy, multi-state sales tax oversight, cross-border structuring, and high-level accounting architecture for e-commerce brands, subscription and SaaS businesses, platform-based models, and multi-entity groups.

We work with founders and leadership teams who require technical precision, structural clarity, and financial frameworks built for scale, capital events, and long-term resilience.

The Non-US Founder’s Complete Guide to Running a US Business

Part 1 — Before You Start

Part 2 — Choosing Your US Entity

Part 3 — Formation

Part 4 — US Banking

Part 5 — US Federal Tax

Part 6 — US State Tax

Part 7 — Paying Yourself

Part 8 — Accounting and Bookkeeping

Part 9 — Annual Compliance Calendar

Part 10 — Hiring in the US

Part 11 — Intellectual Property and Contracts

Part 12 — Your Home Country Obligations

Part 13 — Applied Business Types

Part 14 — Exiting, Winding Down, or Restructuring

Disclaimer:

Content published by Antravia is provided for informational purposes only and reflects research, industry analysis, and our professional perspective. It does not constitute legal, tax, or accounting advice. Regulations vary by jurisdiction, and individual circumstances differ. Readers should seek advice from a qualified professional before making decisions that could affect their business.

See also our Disclaimer page

Antravia Advisory

Accounting built for complexity

Not legal advice, always verify with your Accountant

Email:

Contact us:

© 2025. All rights reserved. | Disclaimer | Privacy Policy | Terms of Use |

contact@antravia.com

Antravia LLC

941 W Morse Blvd suite 100

Winter Park

Florida

32789